Why Are Stock Markets Hitting Record Highs Despite Everything Going On?

(image created by AI; article written by me)

Markets at New Highs — and a War Still Raging

Global stock markets continue to reach record highs despite geopolitical tensions, rising oil prices and higher bond yields — largely driven by exceptionally strong US corporate earnings and growing optimism around AI-led productivity gains. While inflation and borrowing costs remain key risks, history suggests that staying invested through uncertainty is usually more effective than trying to time short-term market movements.

I try not to comment on financial markets too often.

The reason is that there's already plenty of that commentary out there, and it would also be contradictory to keep ‘banging the drum’ that investing is a long game, only to react to every short-term market move.

That said, our recent conversations with clients have been dominated by one question: how are global stock markets making new highs given everything going on in the world?

The confusion is understandable. Despite ongoing geopolitical tensions, sharply higher oil prices and rising government bond yields, markets have continued to climb. The S&P 500 and Nasdaq — the two main US equity indices — have both hit fresh record highs this week, with many other regions either joining them or not far behind.

On the face of it, this seems disconnected from reality. So, what on earth is going on?

As ever, there are two sides to the story.

Please note: when investing, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invested. Past performance is not a reliable indicator of future returns. This blog is for general information only and does not constitute personal financial advice.

The Bear Case: Inflation & Borrowing Costs

The bear case — the pessimistic view — centres on borrowing costs, or more specifically, interest rates. These remain one of the key drivers of stock market performance and risk assets in general.

In turn, interest rates are largely dictated by inflation. When inflation rises, central banks typically raise rates to cool demand — and that’s generally bad news for equities in two distinct ways.

First, higher borrowing costs squeeze company profits. Businesses pay more to service debt, consumers face higher mortgage and lending costs, and spending slows as a result. That slowdown is precisely the intention of the central bankers: weaker demand should, eventually, bring inflation back under control.

Second, higher interest rates reduce valuations. Future profits become less valuable in today’s money when cash can earn a higher return elsewhere. In simple terms, investors become less willing to pay high multiples for earnings that may not arrive for many years.

And this is where the bear case becomes more compelling.

The oil shock linked to the Iran conflict has pushed commodity prices broadly higher, reigniting fears that inflation could remain elevated for longer than markets had hoped. Bond markets have responded accordingly. Yields on 10-year US Treasuries (bonds issued by the US government) recently hit their highest level since last July, while 30-year yields briefly moved above 5%.

At the start of the year, markets were confidently pricing in interest rate cuts. Now, expectations have shifted sharply, with investors increasingly worried that the next move could be another rate rise.

Echoes of 2022

There are uncomfortable echoes of 2022 here:

Towards the end of 2021 and into early 2022, inflation was already creeping higher following the enormous wave of Covid-era stimulus.

Then came a supply shock, with Russia’s invasion of Ukraine, which sent energy and commodity prices soaring.

Initially, inflation was dismissed as “transitory”. It turned out not to be. Inflation surged into double digits in the UK, central banks responded with aggressive interest rate hikes, and both equities and bonds sold off heavily. For traditional balanced portfolios, it was one of the worst years in recent history.

We’re clearly nowhere near those inflation levels today. But the warning signs coming from the bond market feel uncomfortably familiar — even if equity investors, for now at least, appear happy to look the other way.

The Bull Case: Earnings, AI, and a Booming US Economy

If the bond market is flashing warning signs, the corporate earnings picture is telling a very different story, especially in the US.

Q1 2026 was, by almost any measure, a blowout quarter. According to FactSet data, 84% of S&P 500 companies reporting to date beat earnings estimates — the highest proportion since Q2 2021. In aggregate, companies reported earnings around 20% above forecasts — more than double the long-run average. The tech sector led the charge, with earnings growing around 24% year-on-year.

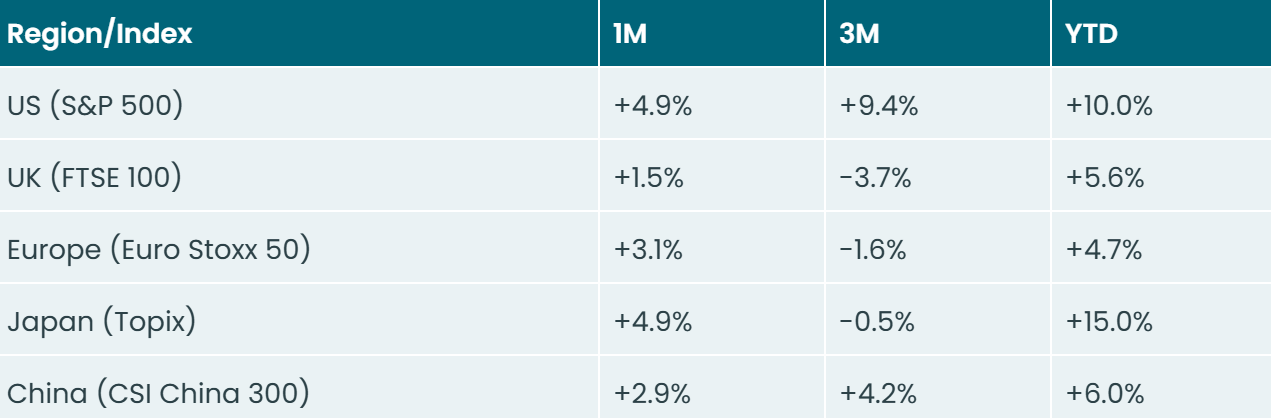

And it is the US that continues to drive the recovery in global equities. The table below compares the performance of the main equity regions and indices, over the last month, three months, and year-to-date (YTD):

As you can see, most major regions have been broadly flat — or slightly negative — over the last three months. US equities, by contrast, have surged ahead, with the S&P 500 gaining almost 10% over that period alone.

In fact, the index closed April at a fresh all-time high of 7,209, marking its strongest monthly gain since 2020. As of this week, the S&P now sits more than 14% above its March low and roughly 10% higher year-to-date.

AI Is Now Showing Up in the Numbers

A major part of this earnings story is artificial intelligence (AI).

But importantly, the narrative is beginning to shift. For the last two to three years, AI has largely been a “big tech” story — companies spending extraordinary sums on chips, data centres and infrastructure. That remains true today, benefiting a relatively small group of firms operating at the centre of the AI boom.

However, the strong performance of US small and mid-cap companies this year suggests something broader may now be happening. The Russell 2000 — a benchmark for smaller US listed companies — is up around 17% year-to-date, hinting that the benefits of AI may be starting to spread beyond big tech and into the wider economy.

In other words, it’s no longer just about the companies building AI — it’s increasingly about the companies using it. Businesses across a wide range of industries are beginning to improve efficiency, reduce costs and boost productivity through automation and AI-driven tools.

The bulls argue this trend is only just beginning, not just in America but globally. If AI genuinely drives a sustained improvement in productivity and profit margins, then today’s elevated market valuations may prove far more justified than they currently appear.

The Tug of War — and What to Do About It

So that’s how we currently see the world.

On one side: sticky inflation, rising bond yields, record levels of government borrowing, and uncomfortable echoes of 2022.

On the other: exceptionally strong corporate earnings, AI-driven productivity gains, and a remarkably resilient US economy that continues to power global growth.

For now, markets are clearly siding with the bulls. The question is whether that reflects rational optimism — or wishful thinking.

The honest answer is we don’t know (and we’d be wary of anyone who claims they do).

What we can say with greater confidence is this:

Trying to Time the Market Is a Losing Game

Cast your mind back a few months. The Strait of Hormuz had effectively closed. Oil prices were surging. Inflation expectations were rising. Bond yields were climbing. The consensus view was that equity markets faced significant headwinds through the remainder of 2026.

Since then, the S&P 500 has rallied more than 14% from its March lows. Anyone who sold to “wait and see” is now faced with the uncomfortable decision of when to buy back in — and at materially higher prices.

And as we’ve written before, the best days in markets tend to cluster around periods of maximum uncertainty and volatility. Miss those days, and long-term returns suffer significantly.

Equities Have Historically Been a Good Inflation Hedge

High inflation is a clear and direct negative for bonds because it erodes the real value of fixed interest payments. But the picture is more nuanced for equities — at least unless inflation becomes extreme and destabilising.

Strong companies typically have pricing power, which means they can pass rising costs onto customers, protect profit margins, and continue growing earnings over time. In periods of moderate inflation, that can allow equities to keep pace with — or even outgrow — rising prices.

That doesn’t mean equities are immune to inflation, but the relationship is far more complex than the recent warning signals from bond markets alone might suggest.

Markets Correct — That's Normal

Even if the bull case proves right, corrections along the way are inevitable.

Markets typically suffer a 10% pullback most years, with larger falls of 20%-plus every four or five years. That volatility is not a flaw of investing — it is the price of admission. There has to be some risk to earn a long-term return above cash.

The challenge is not to avoid those periods, but to stay invested through them, rather than trying to jump out and back in at precisely the right time — a game very few people win.

Our View

Short-term market moves are inherently unpredictable.

Longer term, however, the picture is much clearer. Over the last century, equities have endured wars, recessions, inflation shocks, political crises, pandemics and financial crashes — and yet global markets have continued to rise, at roughly 9-10% a year in nominal terms, or 4-5% real (inflation-adjusted).

Why? Because behind the stock market sit real businesses, driven by innovation, productivity, inflation and, ultimately, the human desire to create wealth and generate profits. Capitalism has proven remarkably resilient.

As long as those forces remain in play, we see no reason to believe equities will not continue to deliver returns comfortably ahead of inflation over the long run.

As ever, the boring answer is usually the right one: stay invested, stay diversified, and let the long-term story play out.

Happy Thursday!

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.