The Pension Tax Arbitrage: Why Pensions Still Make Sense

(image created by AI; article written by me)

Pension Tax Arbitrage

Pensions remain one of the most tax-efficient ways for UK taxpayers to build long-term wealth, thanks to upfront tax relief, tax-free investment growth, and partial tax-free withdrawals in retirement. In many cases, the “pension tax arbitrage” means the government effectively subsidises your retirement savings - particularly for higher earners and those caught in the 60% tax trap.

Pensions have had a rough few years in the court of public opinion. Various rule changes, tax tweaks, and a constant drumbeat of doom-laden headlines have unsettled savers — particularly younger ones. But strip away the noise, and the arithmetic remains compelling.

In this week’s blog, we’re going back to basics, looking at why pension saving is, mathematically speaking, one of the most powerful wealth-building tools available to UK taxpayers — and how the numbers shift depending on your circumstances (your tax status).

The Triple Whammy: Three Tax Advantages in One

Pension saving benefits from a ‘triple whammy’ tax benefit:

Tax relief on contributions. Contributions benefit from tax relief at your marginal rate of income tax, which significantly reduces the effective cost of investing. For example, a £1,000 gross pension contribution would cost £800 for a basic-rate taxpayer, £600 for a higher-rate taxpayer, and £550 for an additional-rate taxpayer. This means the government effectively contributes the balance via tax relief, boosting the value of your pension investment from day one.

Tax-free growth. Once inside a pension, your money grows completely free of income tax and capital gains tax.

Partial tax-free withdrawal. When you come to draw your pension, 25% of your fund (up to £268,275 — more on this shortly) can be taken tax-free. The remainder is taxed as income, but at your marginal rate in retirement — which, for many people, is lower than during their working years.

Taken together, these three advantages create what we call the ‘pension tax arbitrage’: the difference between what a contribution costs you and what it’s worth when you take it back out. Even ignoring investment growth entirely, that arbitrage can be substantial.

A pension is a long-term investment and funds are not normally accessible until 55 (rising to 57 from April 2028). When investing via a pension, your capital is at risk. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

The Base Case: 40-45% Tax Relief In; 20% Tax Out

Let’s start with a worked example.

Assume you’re an additional rate taxpayer, i.e. earning say £150,000 a year, and you make a £10,000 gross pension contribution.

Ignoring any investment growth — which can compound tax-free over many years — the numbers look like this:

Net cost to you: £10,000 less 45% tax relief = £5,500

Tax-free cash at retirement: 25% of £10,000 = £2,500 (withdrawn completely free of tax, assuming you have sufficient allowance)

Taxable portion: The remaining £7,500 is ideally drawn at the basic rate of tax in retirement (20%) = tax bill of £1,500 = net proceeds of £6,000

Total net proceeds: £2,500 + £6,000 = £8,500

In summary, a £5,500 outlay ultimately delivers £8,500 back in your hands. That’s a 54.5% return on cost, before a single penny of investment growth.

This is pension arbitrage in its simplest form. It works because you received tax relief at 45% on the way in, but the money comes back out taxed at only 20% (on 75% of it). In effect, the government is subsidising your long-term retirement savings.

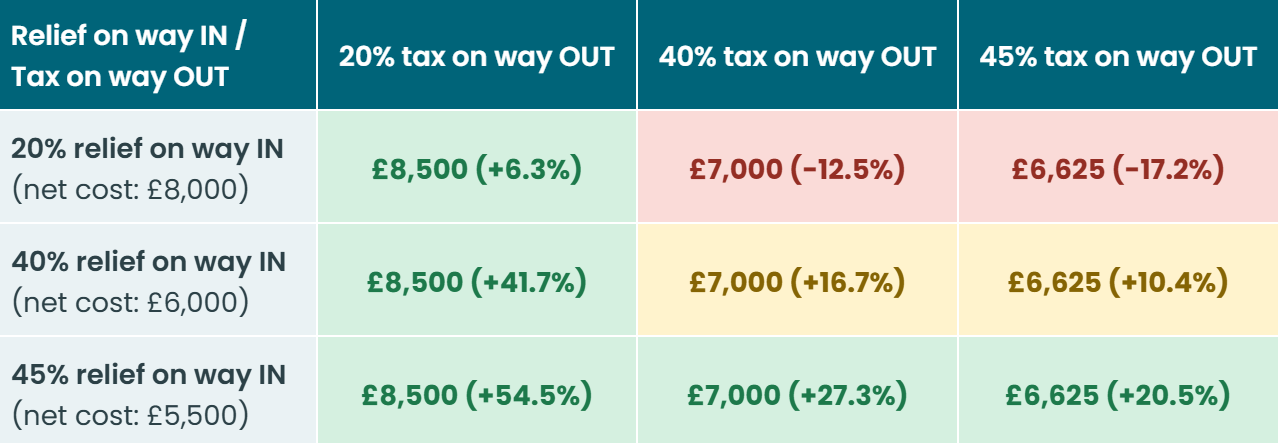

The Arbitrage Mix: Different Rates In, Different Rates Out

Of course, the power of the pension tax arbitrage depends on two variables: the rate of tax relief you receive on the way in, and the rate at which you pay tax on the way out.

The table below illustrates the outcome of a £10,000 gross pension contribution under a range of common scenarios. For simplicity, we’ve assumed contributions are made to a personal pension using the standard “relief at source” method — meaning the individual makes a net contribution, basic-rate tax relief is added automatically by the provider, and any higher or additional-rate relief is reclaimed via self-assessment.

These examples do not include any potential National Insurance savings available through salary sacrifice arrangements, which can further enhance the overall benefit. We revisit this later.

Also note, all figures assume that 25% of the pension can be taken tax-free at retirement. Accordingly, the net proceeds are calculated as 25% tax-free cash plus 75% taxed at the relevant income tax rate shown.

Reading the matrix: green cells represent a 20%+ return on cost (the pension arbitrage works heavily in your favour). Amber cells are more marginal, with a <20% return. Red cells are where the arithmetic actually turns negative, where you receive basic rate tax relief on contribution, then draw your pension as a higher or additional rate taxpayer.

The key takeaway is that good retirement planning is as much about how you draw your pension as it is about how you build it. The goal, where possible, is to extract funds as a basic rate taxpayer — keeping the bulk of your retirement income below the higher rate threshold of £50,270.

The 60% Tax Trap: Where Pension Tax Arbitrage Becomes Even More Powerful

For some earners, the case for pension saving is even more compelling than the 45% scenario above.

If your income falls between £100,000 and £125,140, you are caught in one of the UK’s most punishing tax traps. For every £2 earned above £100,000, you lose £1 of your Personal Allowance. The result is an effective marginal tax rate of 60% on that band of income.

Pension contributions are one of the most effective ways to escape this trap. By reducing your ‘adjusted net income’ below £100,000, you can restore your Personal Allowance and receive effective tax relief of 60% on those contributions.

On a £10,000 gross contribution at 60% effective relief, your net cost could be as little as £4,000. Combined with £8,500 in net proceeds (assuming the 20% draw-down rate), that’s a return on cost of over 112% — again, before investment growth.

What About Basic Rate Taxpayers?

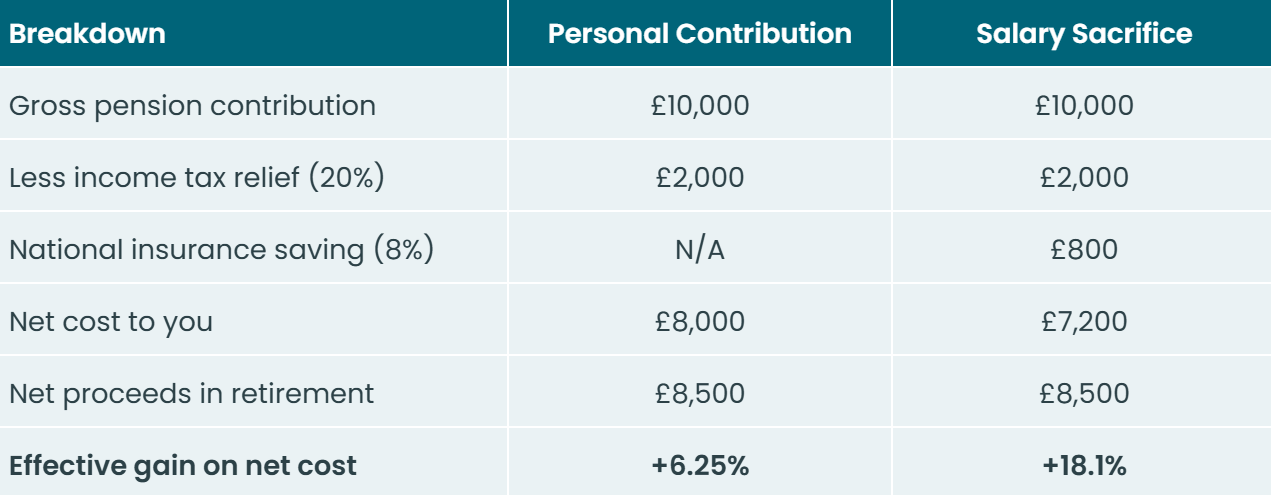

It’s easy to assume pension saving is primarily a tool for higher earners. However, even at the basic rate of income tax, the upfront relief is meaningful — and can be enhanced further through salary sacrifice.

1. Personal Contribution (Income Tax Relief Only)

Say a basic-rate taxpayer contributes £8,000 net into their pension. HMRC then adds £2,000 in basic-rate tax relief, resulting in a total gross contribution of £10,000. The effective net cost is therefore £8,000.

Using the matrix above (20% tax relief in, 20% tax out), the pension ultimately generates net proceeds of £8,500 — an effective return on cost of 6.25%.

That may appear modest, but it is still a positive uplift before taking account of any investment growth, which compounds free of income tax and capital gains tax over the accumulation period.

2. Salary Sacrifice (Extra 8% NI Saving)

The arithmetic becomes even more compelling when pension contributions are made via salary sacrifice — a structure commonly available through workplace pension schemes.

Rather than making a pension contribution from take-home pay, you agree to reduce your salary, with your employer paying the equivalent amount directly into your pension. Because the contribution never passes through payroll as taxable income, you avoid both income tax and employee National Insurance on that portion of salary.

For a basic-rate taxpayer, this creates an additional 8% National Insurance saving on top of the standard 20% income tax relief, materially improving the overall efficiency of the contribution.

Note, higher and additional-rate taxpayers can also benefit from salary sacrifice, although the National Insurance saving is smaller — currently 2% — reflecting the marginal NI rate above the Upper Earnings Limit.

It is worth noting that the rules on salary sacrifice are due to change from April 2029. Under current proposals, only the first £2,000 of annual pension contributions made via salary sacrifice will remain exempt from National Insurance. Contributions above this level would become subject to both employee and employer NICs, significantly reducing the additional benefit currently available through salary sacrifice arrangements for basic-rate taxpayers.

The table below compares the effective “pension tax arbitrage” achieved by a basic-rate taxpayer when making a £10,000 gross pension contribution via a standard personal contribution (income tax relief only) versus salary sacrifice (income tax relief + NI saving).

As you can see, the additional National Insurance saving available through salary sacrifice materially enhances the effective tax arbitrage of pension contributions for a basic-rate taxpayer.

The ‘Magic Number’

The examples above assume you can take 25% of your pension tax-free in retirement. But it’s important to note that this benefit is capped.

The Lump Sum Allowance limits your total tax-free cash entitlement to £268,275 across all pension pots. This represents 25% of £1,073,100 (the previous Lifetime Allowance before this was abolished) — which means once your pension exceeds this value, you’ve used up your tax-free entitlement and every further pound withdrawn is subject to income tax.

This is why, in our view, the sweet spot for pension accumulation sits around £1.1–1.2m for most clients — enough to maximise the tax-free cash entitlement, without building a pot so large that the withdrawal strategy becomes significantly less tax-efficient.

Note, some individuals may be entitled to a higher Lump Sum Allowance where they successfully applied for Lifetime Allowance protections, such as Fixed Protection or Individual Protection.

Why £1.1-1.2m is Our Target Zone

The arithmetic of pension contribution is most compelling when the following are satisfied:

Contributions made as a higher or additional rate taxpayer: 40–45% relief on the way in.

Full tax-free cash taken: £268,275 withdrawn completely free of tax.

Residual drawn as a basic rate taxpayer: Ideally keeping total income (State Pension + pension drawdown) below the higher rate threshold of £50,270.

This translates to the 40-50% ‘pension tax arbitrage’ detailed in the earlier matrix.

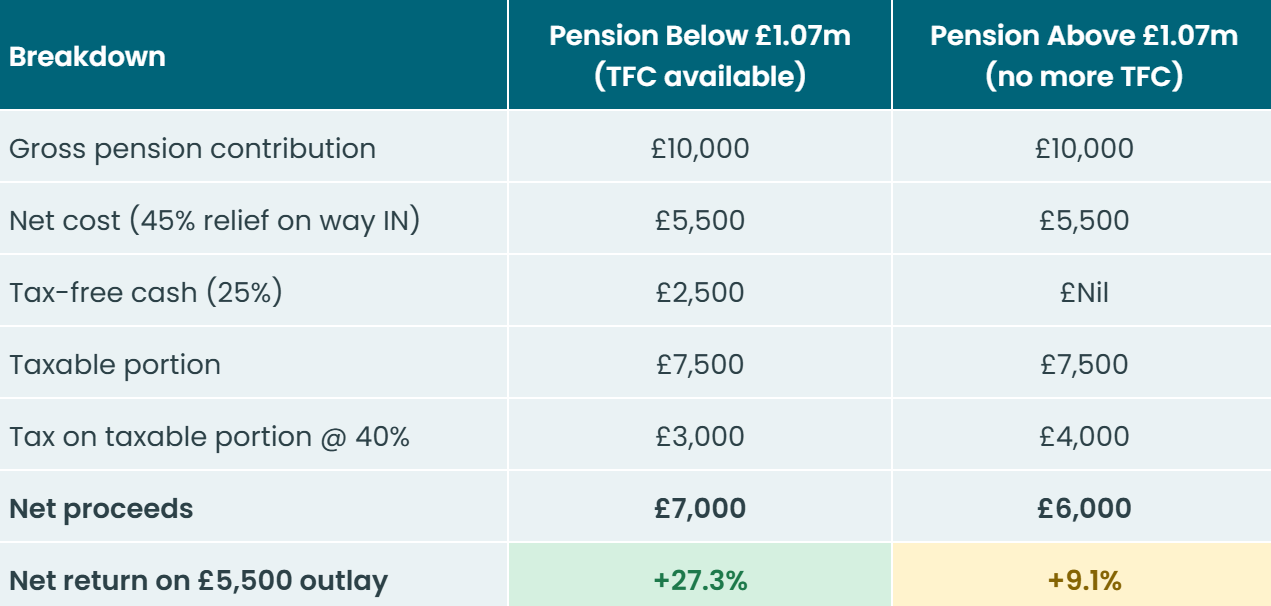

Beyond the Magic Number: Diminishing Returns, But Still Attractive

What happens if you continue contributing once your pension exceeds the level at which the full tax-free lump sum is available?

The short answer is that the ‘pension tax arbitrage’ becomes less powerful — but can still remain attractive.

Once your tax-free cash entitlement has been fully utilised, all further withdrawals are taxable as income. And where pension income in retirement pushes you into the higher-rate tax band, the gap between the tax relief received on the way in and the tax paid on the way out narrows materially.

For example, assume you make pension contributions as an additional-rate taxpayer, receiving 45% tax relief upfront, but ultimately pay 40% income tax on withdrawals in retirement. The economics then look as follows:

As the table shows, once tax-free cash has been exhausted and withdrawals are taxed at 40%, the effective benefit reduces materially. A contribution costing £5,500 after tax relief ultimately produces £6,000 net — still positive, but far less compelling than the earlier examples.

Importantly, however, this analysis still ignores any investment growth achieved within the pension wrapper, which continues to compound free of income tax and capital gains tax. Over long time horizons, that tax shelter can remain highly valuable, even where the upfront arbitrage is reduced.

A Word on Accessibility

Hopefully, this blog reinforces the point that pensions are, generally speaking, the most tax-efficient form of long-term saving and investment, thanks to their powerful combination of upfront tax relief, tax-free investment growth, and tax-free cash in retirement.

The trade-off, however, is accessibility.

Money contributed to a pension is effectively locked away until the Minimum Pension Age — currently 55, rising to 57 from 2028. For many people, that loss of liquidity is the principal drawback of pension saving.

The key question, therefore, is whether the tax advantages outweigh the restriction on access. In most cases we advocate a blended approach: maximising pension contributions where appropriate, whilst also building accessible capital through other wrappers, most commonly ISAs first, followed by General Investment Accounts (GIAs) and other structures where suitable.

A Word on Inheritance Tax

There is another important caveat to the “let the pension grow as large as possible” strategy.

From 6 April 2027, unused pension funds are due to fall within the scope of Inheritance Tax for the first time, potentially exposing pension assets to a 40% IHT charge on death. For individuals who had planned to preserve pensions primarily as intergenerational wealth vehicles, this represents a significant shift in the planning landscape.

We have explored this in more detail in previous blogs, most recently this one: The Pension Double Death Tax.

In Summary

The ‘pension tax arbitrage’ is real, and in most scenarios it is substantial. To recap the key scenarios:

45% tax relief IN, 20% tax OUT: Cost £5,500 for £8,500 net proceeds. Return on cost: +54.5%.

60% effective relief IN (£100k–£125,140 band): Cost as low as £4,000 for £8,500 net proceeds. Return on cost: 112%+.

Basic rate via salary sacrifice: Net cost £7,200 for £10,000 in pension. 28% effective relief.

20% taxpayer IN, 40-45% tax OUT: The two scenarios where the arithmetic turns negative.

Magic number (~£1.07m): The point at which tax-free cash is exhausted. Build beyond this with care, particularly with IHT changes arriving in April 2027.

None of the analysis above incorporates investment growth which, over multiple decades within a tax-advantaged pension wrapper, is often the most powerful driver of long-term wealth accumulation. The tax arbitrage provides the foundation; time and compounding provide the acceleration.

Pensions therefore remain the most tax-efficient long-term savings vehicle available to UK investors. While the rules and allowances may evolve over time, the underlying arithmetic has remained remarkably resilient through successive rounds of pension reform. Short-term headlines should not obscure that broader reality.

Happy Thursday!

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.