How Delaying Retirement by 2.5 Years Can Add a Decade to Your Financial Security

(image created by AI; article written by me)

How a small shift in your retirement date can make a vast difference

Retirement timing is one of the most powerful levers in financial planning. Working just two and a half years longer can extend the life of a retirement portfolio by over a decade, while working to 65 instead of 60 can increase sustainable annual spending by as much as £20,000 — for the rest of your life.

One of the key roles of a financial planner is to determine whether you're on track to have sufficient income and accessible capital to support the lifestyle you want in retirement.

While there are many factors that influence this, one of the most powerful is often the retirement date itself.

That may sound like an obvious point, but the impact can be far greater than many people realise. In this week's blog, we explore how even a relatively modest delay to retirement can significantly improve your long-term financial position and projected future wealth.

As a result, where retirement timing is flexible, the conversation often shifts from "When do I want to retire?" to "What sort of retirement do I want?" — particularly in terms of the level of spending, flexibility and financial security you wish to enjoy in later life.

The Triple Whammy

The impact of deferring retirement is extremely powerful in terms of wealth creation due to a ‘triple-whammy’ effect:

1. Earnings and contributions continue

Your salary continues, pension contributions continue, and any surplus income can continue to be directed towards savings and investments. In other words, more money is flowing into your retirement pot.

2. Withdrawals are delayed

At the same time, you're postponing the point at which you start drawing on your pensions, investments and savings. The money therefore remains invested for longer, benefiting from an additional year of compounding rather than being spent.

3. You begin retirement from a stronger position

Perhaps most importantly, a larger pot at retirement is inherently more sustainable. The same level of spending represents a smaller percentage withdrawal, leaving more of the portfolio's growth available to replenish what has been taken out.

For example, someone withdrawing £50,000 a year from a £500,000 portfolio is drawing 10% annually. Someone withdrawing the same amount from a £700,000 portfolio is drawing just 7.1%. Assuming growth of 6% a year after costs, the first portfolio would be depleted after around 15½ years, whereas the second would last more than 31 years. A portfolio that is 40% larger can ultimately support withdrawals for more than twice as long.

These figures are for illustrative purposes only and do not reflect actual investment returns, which can fluctuate and are not guaranteed.

The combined effect of these three factors is extremely powerful. Additional contributions increase the size of the pot. Delayed withdrawals keep more money invested. And a larger starting portfolio makes future withdrawals more sustainable. Played out over several years, these effects compound on one another, meaning that even a relatively modest delay to retirement can have a transformative impact on long-term financial security.

A Potential Fourth Factor

There is also a potential fourth factor that can make the above even more powerful.

Many people target retirement at 60 or 65. But that window often coincides with one of the most financially unencumbered periods of adult life.

By this point, children may have finished university and become financially independent. The mortgage may also have been reduced substantially, or repaid entirely.

The result is that additional years of work do not just add income to the pot. They often do so at a point when personal expenditure is lower than it has been for decades.

The years immediately before retirement can therefore be among the highest-earning and lowest-obligation years of a person’s financial life. That means the ability to save and ‘increase the pot’ can be supercharged.

As ever, this is best illustrated by way of an example.

Worked Example

Consider Jack, aged 50.

He currently earns £175,000 a year

He is an active member of his workplace pension scheme. His pension is currently worth £400,000, and total annual contributions amount to 15% of salary, split equally between his own salary sacrifice contributions and employer funding.

Outside of his pension, Jack has accumulated £50,000 in cash savings and a further £250,000 in investments. Of the latter, £150,000 is held within a Stocks & Shares ISA, with the remaining £100,000 invested via a General Investment Account (GIA).

His home is worth approximately £600,000 and is subject to an outstanding repayment mortgage of £100,000. The mortgage has ten years remaining and carries an interest rate of 4%.

Looking ahead, Jack is on track to receive the full State Pension from age 67.

His target spending level in retirement is £6,000 per month after tax. For now, any surplus income is directed towards his ISA and investment portfolio, allowing both to continue growing alongside his pension savings.

When discussing retirement, Jack explains that he would like to retire "sometime between age 60 and 65", but he has not yet settled on a specific date.

Modelling assumptions

We can now combine Jack's current financial position with a number of assumptions to project his finances into the future:

Earnings and expenditure are assumed to increase in line with inflation.

No future property downsizing is assumed, as this is not currently part of Jack's plans.

Pension and investment assets are assumed to grow at 6% per annum, net of all underlying costs and charges.

State Pension benefits increase with inflation.

As with any financial projection, the results should be viewed as illustrative rather than predictive. Actual investment returns, inflation, tax rates and future legislation may differ from those assumed, and future outcomes cannot be guaranteed.

A pension is a long-term investment and funds are not normally accessible until 55 (rising to 57 from April 2028). When investing, your capital is at risk. The fund value may fluctuate and can go down as well as up.

The Retirement Delta in Numbers

We now model three scenarios across Jack’s retirement range. In each case, cashflow modelling software is used to project his total liquid capital — cash, investments, and pension — as a gauge of whether he is on track to sustain his desired retirement lifestyle.

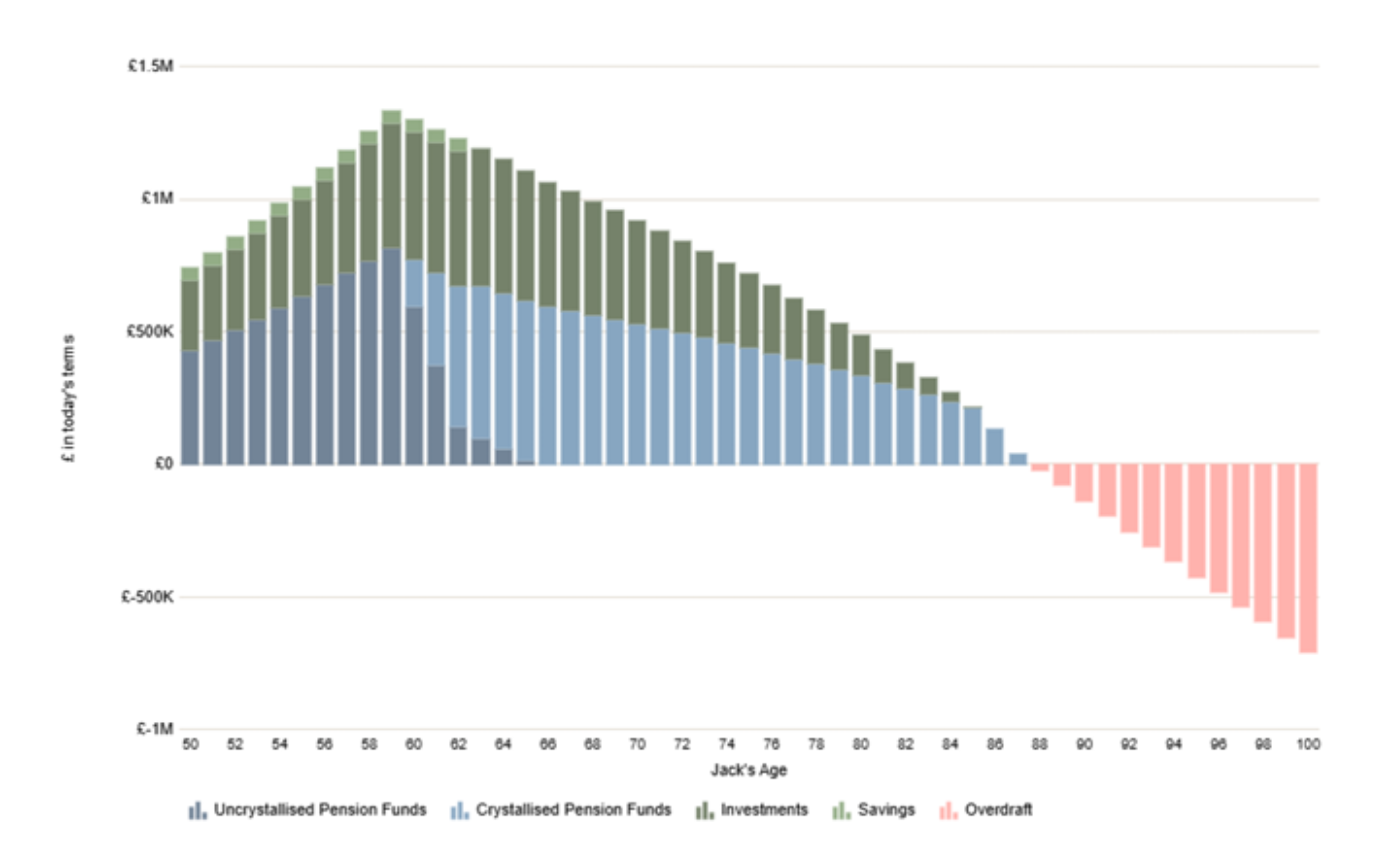

1. Retire at 60

Retiring at 60 — a decade from now — Jack’s liquid capital is projected to be depleted around age 87. On the face of it, that might sound acceptable. But life expectancy at 60 for a man in good health is comfortably into his nineties

Jack owns his home, so there is equity outside the projection. But releasing it is not straightforward, and it is not what he wants to do. The more pertinent observation is that this scenario carries real sequencing risk: if investment returns are poor in the early years of retirement — when the pot is largest and most vulnerable — the picture could deteriorate significantly.

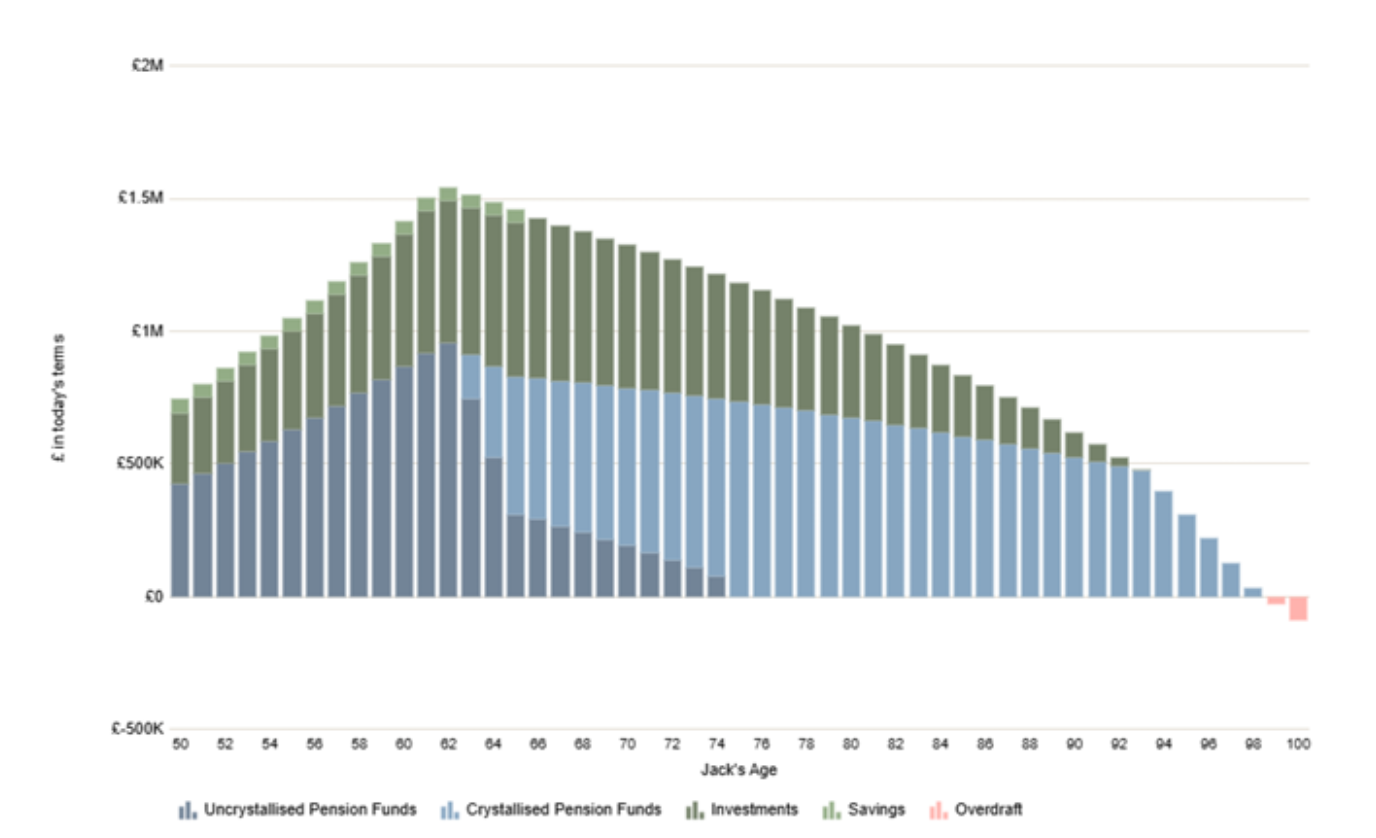

2. Retire at 62 ½

Deferring by just two and a half years transforms the picture. Jack’s liquid capital is now projected to last until around age 98 — comfortably beyond any reasonable life expectancy assumption. The risk of running out has effectively been removed from the conversation.

That is striking - a 2½-year delay to retirement has pushed the depletion point out by around eleven years. This is the ‘triple whammy’ effect at work: more contributions, less drawdown, and a meaningfully higher starting balance that compounds more efficiently throughout retirement.

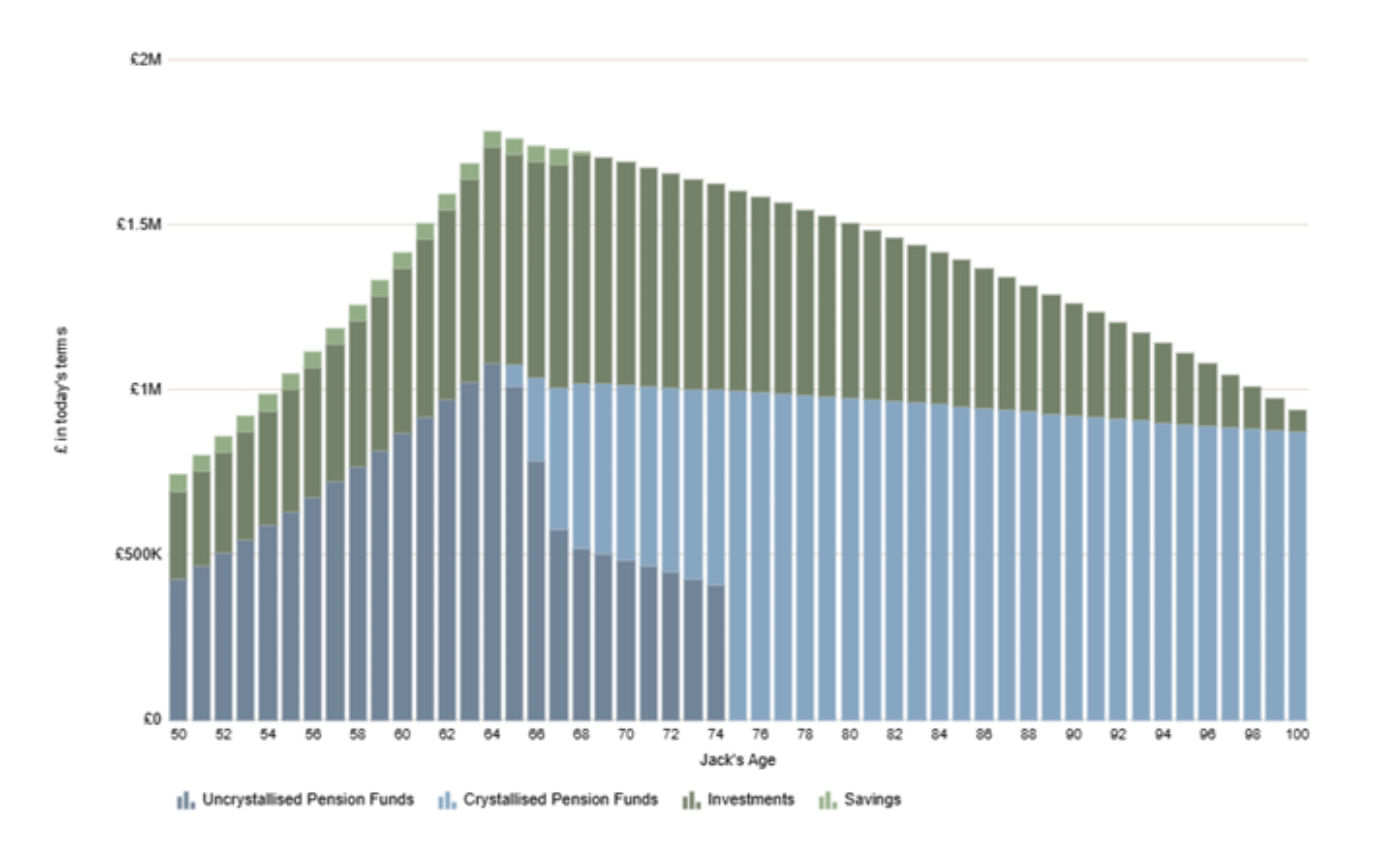

3. Retire at 65

Working to 65 produces a result that might initially seem hard to believe. Jack is now projected to hold liquid assets in excess of £1 million at age 100 — in today’s money, and in addition to his main residence.

This reflects the compounding power of a substantially higher starting point. Comparing the retire-at-65 scenario with retire-at-60, Jack enters retirement with roughly £1.75 million in liquid capital versus approximately £0.75 million — the product of five more years of contributions, employer matching, and uninterrupted investment growth. That larger pot has a lower withdrawal rate relative to its size, which means a greater proportion of returns compound rather than being spent. The effect builds on itself, year after year.

Spending tolerance

Rather than asking whether Jack's money will last, a more useful question might be: how much can he afford to spend?

To answer this, we reverse the calculation. Instead of fixing spending and modelling the outcome, we assume Jack's liquid assets are fully depleted at age 100 and calculate the maximum sustainable level of annual expenditure under each retirement scenario.

The answer, across the three scenarios, looks like this:

Retire at 60: spending tolerance of approximately £61,000 per annum

Retire at 62½: spending tolerance of approximately £71,000 per annum

Retire at 65: spending tolerance of approximately £81,000 per annum

In other words, every additional year worked increases Jack’s sustainable spending by approximately £4,000 per annum — for the rest of his life. Over five years, that is a £20,000 annual difference in what retirement can look like: more travel, more generosity, more flexibility, a larger buffer.

That is the retirement delta at work.

Knowing When Enough is Enough

There is, however, a flip side to this.

The financial benefit of working for a few more years can become its own trap. In Jack’s case, retiring at 65 rather than 62½ could mean materially higher spending power, or a much larger legacy for any beneficiaries - an extra £1 million in the example above.

That is tempting, but it also risks creating a never-ending loop of “one more year”.

This is where good planning matters. The aim is not simply to maximise wealth, it is to understand what “enough” looks like, what retirement is really for, and when the probability of achieving that life is high enough to confidently step away.

Summary

One of the most powerful levers in retirement planning is also one of the simplest: the retirement date itself.

For many people, the difference between retiring at 60, 62½ or 65 is not merely a few extra years of work. It can mean the difference between a retirement that is comfortable and one that is exceptionally secure and flexible. Additional years of earnings, ongoing pension contributions, delayed withdrawals and continued investment growth combine to create a powerful compounding effect that can dramatically improve long-term outcomes.

In our worked example, a delay of just 2½ years pushed the projected depletion date of liquid assets out by more than a decade. Working to 65 increased sustainable retirement spending by around £20,000 per year compared to retiring at 60.

Of course, retirement planning is not about accumulating the largest possible pot. It is about understanding what "enough" looks like and making informed decisions that align with the life you want to live.

The key takeaway? Don't just ask whether you can afford to retire. Ask what each additional year of work is worth — and whether the benefits justify the trade-off.

Happy Thursday!

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.