How to Reduce the ‘Double Death Tax’ on Pensions

A Tax-Efficient Loop to Counter the New Pension IHT Rules

The proposed inheritance tax changes to pensions from April 2027 are creating new planning opportunities for retirees willing to rethink the traditional “preserve the pension” approach. One of the most effective may be the “pension-to-pension” strategy - using pension withdrawals, tax-efficient gifting, and onward pension contributions to move wealth to the next generation with significantly less tax leakage.

With pensions set to be included in your estate for inheritance tax purposes from April 2027, the old logic of preserving your pension and spending other assets first is effectively redundant.

We covered the full detail of the new rules - including the spectre of the ‘double death tax’ - in our recent blog, The ‘Double Death Tax’: How Pensions Will Be Taxed from 2027.

One of the strategies we flagged in that piece was accelerating pension drawdown to create surplus income, and gifting that surplus out of the estate. This week, we expand on this concept and explore the ‘pension to pension’ strategy, to provide a tax efficient loop that can simultaneously reduce your IHT exposure and deliver significant tax relief to the next generation.

Please note, a pension is a long-term investment not normally accessible until age 55 (rising to 57 from April 2028). The value of investments can fall as well as rise. The Financial Conduct Authority does not regulate tax advice.

The Concept

The idea is straightforward:

Draw additional pension income — even if this takes you into the higher-rate band (but ideally not above £100,000 so as not to trigger marginal 60% income tax)

Gift the surplus income to your adult children or grandchildren, qualifying for the Normal Expenditure out of Income IHT exemption

The recipient uses the gift to make a pension contribution, attracting income tax relief at their marginal rate

The result is a transfer of wealth from your pension to theirs — with significantly less tax along the way than leaving it in your estate.

We expand on this below.

Step by Step

Step 1: Draw Additional Pension Income

If you’re already in retirement, the first step is to consider whether you can draw more pension income than you need — creating a genuine income surplus that exceeds your normal living costs.

Assuming you have no further tax-free cash entitlement available, you’ll pay income tax at your marginal rate on this additional income: 20% for basic-rate, 40% for higher-rate. Ideally, you’ll want to keep your total taxable income below £100,000 to avoid the personal allowance taper and the effective 60% tax trap.

Under the new rules, any pension you don’t draw will form part of your estate for IHT. If your estate exceeds the nil-rate bands, that pension will be taxed at 40% on death — and potentially again through income tax when your beneficiaries withdraw it (aka. The ‘Double Death Tax’). Drawing it now, paying income tax at a known rate, and moving the wealth out of your estate is potentially a better outcome.

Step 2: Gift the Surplus

Once you’ve drawn the income and paid tax, the net amount is yours to gift. Provided it meets three conditions, it qualifies for the Normal Expenditure out of Income IHT exemption:

The gift forms part of a regular pattern of giving

It is made from income, not capital

You retain sufficient income to maintain your normal standard of living (i.e. the gift is made out of surplus income)

Unlike a standard ‘Potentially Exempt Transfer’ (PET), which requires a seven-year survival period, gifts qualifying under this exemption are immediately exempt from IHT. Day one. No seven-year clock.

Step 3: Pay Into a Child’s or Grandchild’s Pension

Rather than simply handing over the cash, the recipient could use the gift to make a pension contribution in their own name. A few rules to note:

Anyone can contribute to anyone else’s pension, but the contribution is treated as if the member made it — the recipient gets the tax relief, not the donor

In terms of contribution limits, pension contributions are capped at the lower of 100% of the recipient’s ‘relevant earnings’ (generally, work-related income); and the available annual allowance (£60,000 per tax year, plus any unused allowance carried forward from the previous three tax years, subject to tapering for higher earners). Importantly, these limits are assessed based on the recipient of the gift, not the donor. Consideration must also be given to any existing personal and/or employer pension contributions already made on the recipient’s behalf during the tax year.

For a non-earning child or grandchild, the maximum is £3,600 gross (£2,880 net, topped up with 20% basic-rate relief)

If the recipient is a higher or additional-rate taxpayer, they claim the extra relief via self-assessment — even though the money came from a third party

Why the Maths Are Compelling

Here’s a worked example:

Rose, aged 75, has a defined contribution pension valued at £800,000 and an estate that already exceeds the available inheritance tax nil-rate bands.

Her day-to-day spending needs are comfortably met through a combination of State Pension (£12,500 per annum) and existing pension drawdown income (£3,000 per month / £36,000 per annum). She is therefore already fully utilising her basic-rate income tax band, meaning any additional pension withdrawals would largely be taxed at 40% (higher rate).

Outside of her pension, Rose also holds additional savings and investments, which are currently being left untouched and free to grow for the future.

She decides to draw an additional £40,000 per annum from her pension via flexi-access drawdown, to generate an income surplus, that she can then gift to her daughter. Whilst she could alternatively purchase an annuity to generate further guaranteed income, we assume drawdown remains her preferred option for flexibility purposes.

Rose’s daughter, Ana, earns £100,000 per annum and is currently contributing £10,000 a year into her workplace pension scheme. She chooses to contribute the entire gift amount to her pension.

Comparing the Outcomes

1. Do Nothing

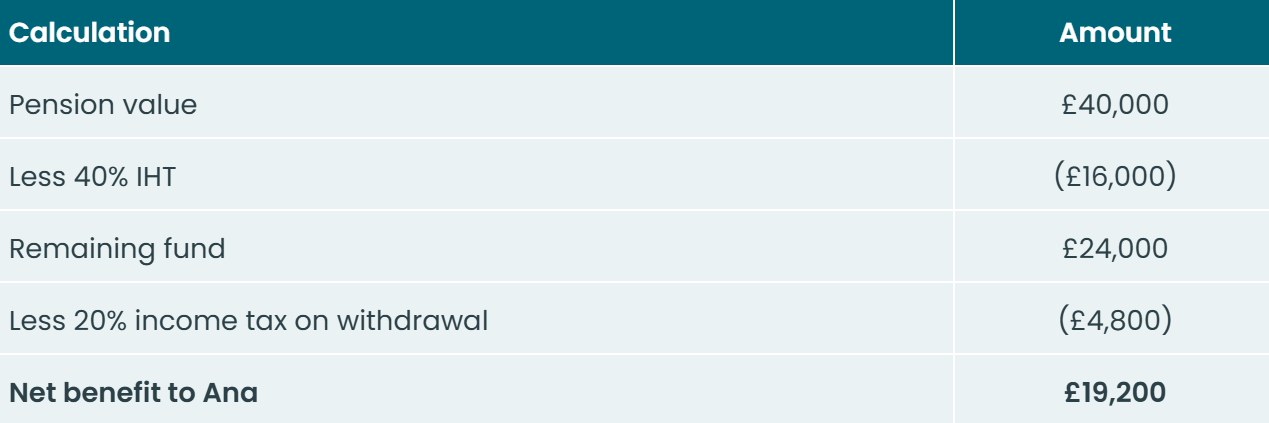

Under a ‘do nothing’ scenario, Rose leaves the additional £40,000 inside her pension.

Assuming the proposed rule changes proceed as expected, the pension could eventually become subject to inheritance tax on death. If Ana subsequently draws the inherited pension whilst a basic-rate taxpayer (in retirement, say), the combined effect of inheritance tax and income tax could reduce the £40,000 to approximately £19,200 net:

2. Pension to Pension Strategy

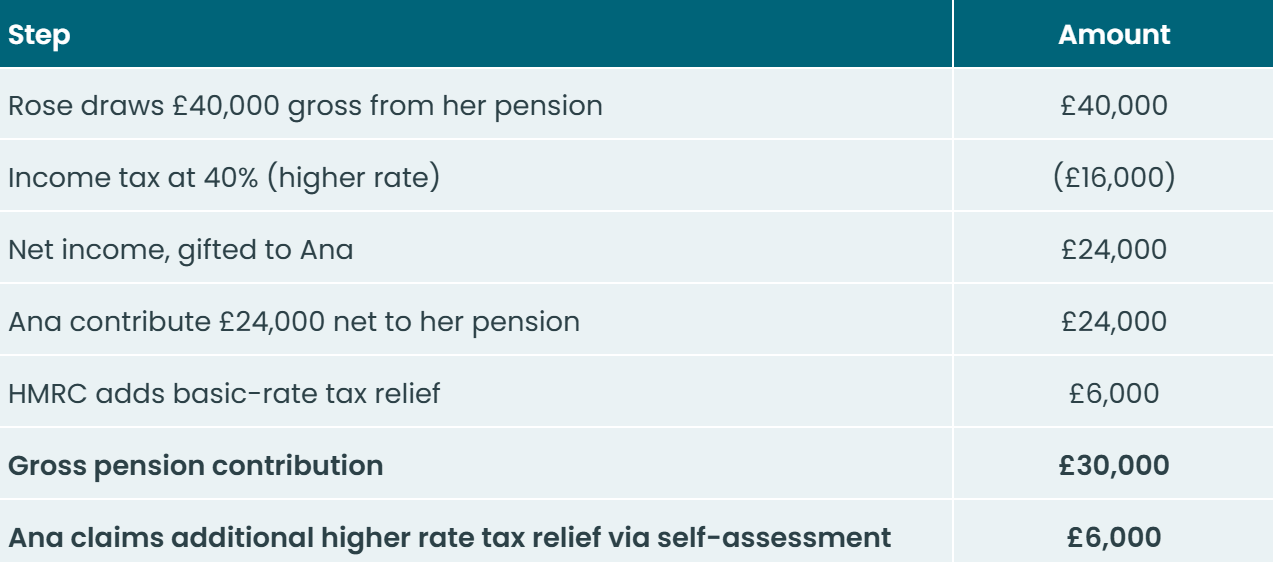

Under the alternative strategy, Rose instead draws the £40,000 during her lifetime.

She pays £16,000 income tax on the withdrawal, leaving £24,000 net. This surplus income is then gifted to Ana. Assuming the gift qualifies under the ‘Normal Expenditure out of Income’ exemption, it falls immediately outside Rose’s estate for inheritance tax purposes.

Ana then contributes the £24,000 into her pension:

HMRC automatically adds £6,000 basic-rate tax relief, increasing the gross contribution to £30,000.

Ana subsequently reclaims a further £6,000 through self-assessment, reflecting her higher-rate taxpayer status.

At this point, £24,000 gifted by Rose has effectively created:

a £30,000 pension contribution, plus

£6,000 reclaimed personally by Ana.

When Ana eventually accesses the pension, she should be able to take up to 25% tax-free (up to a lifetime limit of £268,275), with the balance taxed as income. Assuming she withdraws the funds as a basic-rate taxpayer in retirement, the after-tax proceeds would be approximately:

The Result

Comparing the two approaches:

That represents an uplift of approximately £12,300, or around 64% more value passing to the next generation.

This is an annual amount - the intention would be to repeat this strategy every year, potentially delivering a substantial uplift over time.

Importantly, this example ignores any future investment growth within Ana’s pension, which would further enhance the long-term benefit of the strategy.

It’s also worth noting that the exact maths — and therefore the ultimate net benefit — will vary depending on the tax position of both the original pension holder and the recipient.

For example, the planning can become particularly powerful where pension income is drawn at only 20% tax, whilst the recipient subsequently receives pension tax relief at 40% or even 45%. In some cases, the effective relief may be higher still where pension contributions help restore lost Personal Allowance within the £100,000–£125,140 ‘tax trap’, creating an effective marginal relief rate of up to 60%.

Conversely, the benefit may be less pronounced where the original pension withdrawal suffers 40% income tax, whilst the recipient receives only basic-rate (20%) pension tax relief on the onward contribution.

Nevertheless, even in these less favourable scenarios, the strategy can still compare favourably against the alternative of leaving excess pension monies exposed to a potential double layer of taxation — namely 40% inheritance tax on death, followed by a further layer of income tax when the beneficiary ultimately draws the inherited pension (assuming the previous policyholder passed after the age of 75).

Please note, the Financial Conduct Authority does not regulate tax advice. Tax treatment depends on individual circumstances and may be subject to change in the future.

A Few Things to Keep in Mind

Record-keeping is essential. The Normal Expenditure out of Income exemption is claimed on death, and HMRC will want evidence of a regular pattern funded from surplus income. We typically advise clients to use HMRC form IHT403 as a template.

Don’t overdo the drawdown. Pushing income above £100,000 triggers the 60% trap. The ‘sweet spot’ is typically drawing up to £100,000 of total income without tipping over.

Model your cashflow first. Accelerating drawdown reduces the pot available for your later years. A thorough cashflow plan is essential to ensure you’re not over-committing, i.e. that you retain sufficient liquid capital for your own needs.

The gift is still a gift for IHT. It should qualify under Normal Expenditure out of Income if the conditions are met, or otherwise as a PET with the usual seven-year rule.

The Bottom Line

The pension-to-pension strategy represents a compelling estate planning opportunity ahead of the proposed pension inheritance tax changes due next April.

In simple terms, you pay income tax on the pension withdrawal (typically 20–40%), but potentially avoid 40% inheritance tax via the Normal Expenditure out of Income exemption, whilst also generating fresh pension tax relief in your child’s name through a subsequent pension contribution.

The end result? More wealth stays within the family and less is lost to HMRC — in our example, the strategy improved the net outcome by around 64%, with scope for even greater benefit where pension income can be drawn at lower tax rates.

As always, the detail matters. The appropriate withdrawal level, gifting structure and wider retirement strategy should all be considered carefully alongside your own long-term spending needs and cashflow plan.

Happy Thursday!

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.