The ‘Double Death Tax’: How Pensions Will Be Taxed from 2027

The New Rules and What To Do About Them

In just twelve months, new pension legislation is set to come into effect that will fundamentally change how pensions are treated on death. From 6 April 2027, most unused pension savings will form part of your estate for inheritance tax purposes. This is one of the most significant changes to pension taxation in a generation.

For years, pensions have sat outside your estate. That made them a powerful estate planning tool – many people deliberately preserved their pension, spending other assets first, knowing the pension could pass to loved ones free of IHT. From next April, that strategy is effectively redundant.

In this week’s blog, we take a detailed look at what’s changing and what it means in practice. We cover the new rules, work through a clear example, explore the concept of the “double death tax”, and explain how inheritance tax will actually be applied to pensions. We also consider how these changes affect financial planning more broadly, and how our approach may need to evolve as a result.

It’s a longer read than usual, but given the scale of the changes, it’s an important one.

A pension is a long-term investment and funds are not normally accessible until 55 (rising to 57 from April 2028). When investing via a pension, your capital is at risk. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

No Signs of a U-Turn

The proposed changes have been making their way through Parliament.

The measures were first announced in the 2024 Autumn Statement.

Draft legislation was published on 21 July 2025.

It passed through the Public Bill Committee in January and February 2026.

Royal Assent followed swiftly on 18 March.

Compare this with the Government’s experience on business and agricultural property relief. There, sustained pressure from farmers and business owners led to two major concessions: first, making the allowance transferable between spouses at the 2025 Autumn Budget, and then more than doubling it from £1 million to £2.5 million in December 2025. On pensions, however, the Government has held firm throughout. No concessions of any substance have been made (so far).

What’s Changing

Currently, most unused pension funds sit outside your estate for IHT because pension schemes operate under discretionary trusts. From 6 April 2027, that exemption disappears. Your unused pension will be added to the rest of your estate and, if the total exceeds the available nil-rate bands, it will be taxed at 40%.

The key details:

Pension death benefits passing to a surviving spouse or civil partner remain exempt from IHT, as do benefits paid to a registered charity.

Death-in-service benefits payable from registered pension schemes will be excluded entirely.

The existing income tax rules around age 75 remain unchanged. If you die before 75, beneficiaries can draw on the inherited pension free of income tax. If you die after 75, they pay income tax at their marginal rate on withdrawals.

That last point is crucial. It creates the spectre of a Double Death Tax which we explore below.

Worked Example

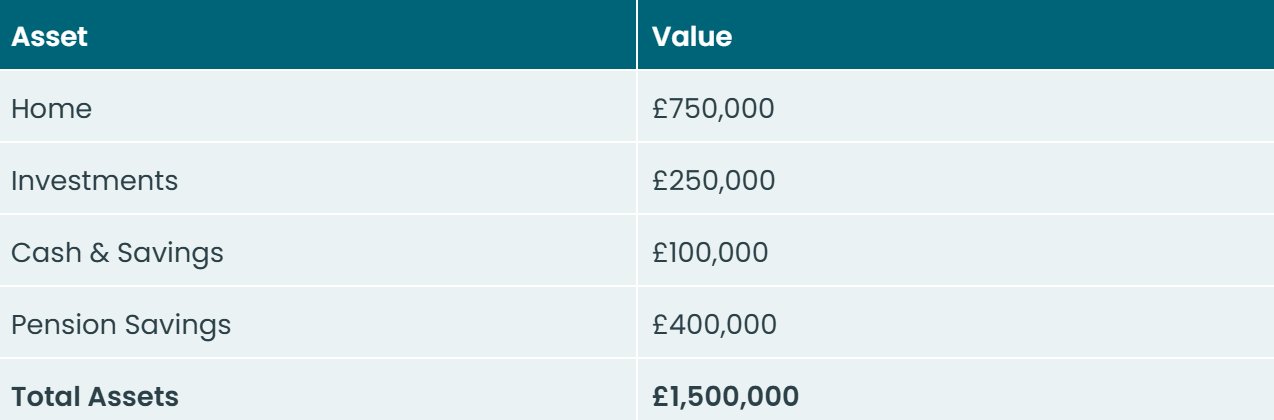

Jin and Sun are married with three children. Their current financial position is summarised below:

From an inheritance tax (IHT) perspective, they benefit from combined nil-rate bands of £650,000 (£325,000 each), plus combined residence nil-rate bands of £350,000 (£175,000 each), assuming their home (or the proceeds thereof) passes to direct descendants. In total, this means up to £1 million of their estate can currently be passed on free of IHT.

Under current legislation

Pension savings typically fall outside of the estate for IHT purposes. This means Jin and Sun’s taxable estate is £1.1 million. After applying their available nil-rate bands (£1 million), the remaining £100,000 would be subject to IHT at 40%, resulting in a potential liability of £40,000.

Under the proposed rules

From next April, pension savings are expected to be included within the estate for IHT purposes. This increases the total estate value to £1.5 million. After deducting the £1 million nil-rate bands, the remaining £500,000 would be subject to IHT at 40%, resulting in a potential liability of £200,000.

In simple terms, this represents an increase in their potential IHT liability of £160,000. Overnight.

Wider implications

For clients with larger pension pots, the impact inevitably becomes even more significant. Furthermore, where an estate jumps above £2 million due to the inclusion of pension savings, the residence nil-rate band begins to taper away (reduced by £1 for every £2 over the threshold), which can further increase the overall tax exposure.

The ‘Double Death Tax’

One of the most widely criticised aspects of the proposed changes is the potential for what has been termed a “double death tax”.

Under current rules, if you die after age 75, any pension inherited by your beneficiaries is subject to income tax at their marginal rate when withdrawals are made. These rules are not changing.

However, under the proposed changes, pension savings would also be included within your estate for inheritance tax (IHT) purposes. This means the same funds could be taxed twice — first via IHT, and then again through income tax when accessed by beneficiaries.

In practical terms, this creates a significantly higher overall tax burden.

From a planning perspective, this feels unduly punitive. A more balanced approach - in my view - would be either:

pensions being subject to IHT, with no further income tax on withdrawal; or

pensions remaining outside the estate for IHT, with withdrawals taxed as income regardless of age at death (i.e. remove the age 75 rule).

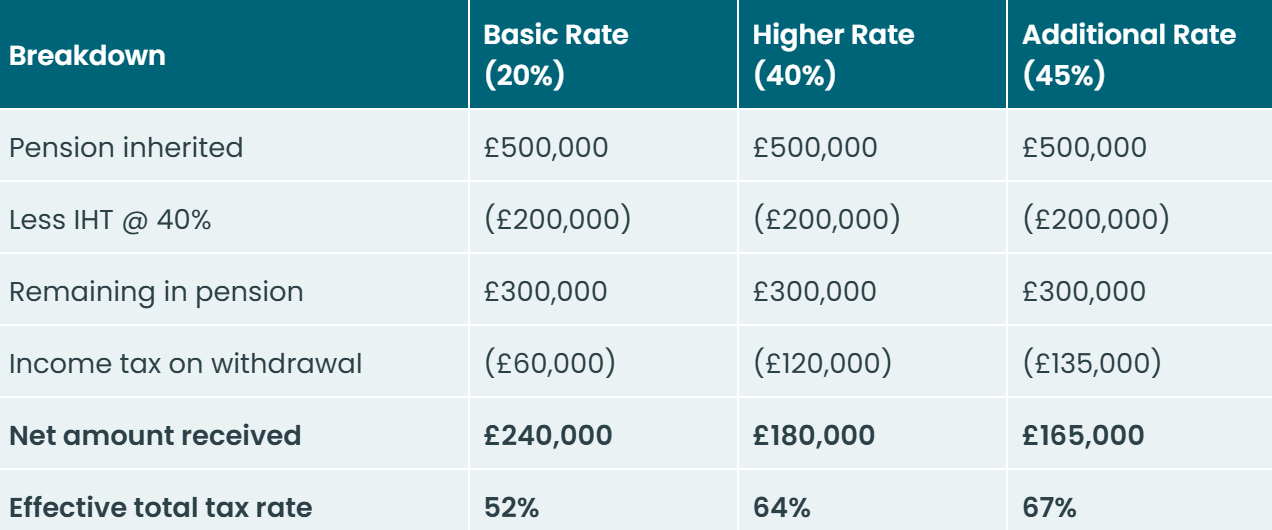

Illustrative example

To demonstrate the potential impact, we revisit Jin and Sun’s position. Assume they leave combined pension savings of £500,000 to their children.

The table below shows the net amount received depending on the beneficiary’s tax band:

At the higher rate, nearly two-thirds of the pension is lost to tax. At the additional rate, this rises to close to 70%.

It’s worth noting this is a simplified, ‘worst-case’ illustration. In practice:

part of the pension may fall within available nil-rate bands (apportioned between pension and non-pension assets), reducing the IHT charge; and

beneficiaries may have flexibility to draw funds gradually, potentially utilising lower tax bands over time (for example, during periods of lower income or in retirement).

Byzantine complexity

As a side note, to illustrate just how complex these new rules are, a major national newspaper recently published an article explaining how the rules would work, including a claim that beneficiaries inheriting a pension would be able to claim income tax relief against IHT already paid from the pension. This was incorrect – a misinterpretation of the legislation – and a correction and apology soon followed. If the broadsheet tax journalists are struggling to get this right, it tells you something about the complexity ordinary families and their advisers are being asked to navigate.

The Mechanics – How IHT Will Actually Be Paid

Getting into the weeds a little, but at a high level, when someone dies on or after 6 April 2027 with unused pension benefits, the process will work broadly as follows:

Step 1 – Information. The legal personal representatives (normally the executors of the estate) must identify the deceased’s pension benefits and notify each pension scheme of the death. The pension scheme administrator must then provide the value of the benefits within four weeks, along with details of how benefits are split between exempt beneficiaries (spouse or charity) and non-exempt beneficiaries - typically following the pension ‘expression of wishes’.

Step 2 – Valuation and withholding. The personal representatives gather information on all pension schemes and the wider estate, determine whether IHT is payable, and if so can issue a “withholding notice” to each pension scheme, instructing them to hold back up to 50% of the benefits for up to 15 months to cover potential IHT liabilities.

Step 3 – Report and pay. The personal representatives calculate the IHT attributable to pension benefits, submit the IHT account to HMRC, and notify the pension scheme and beneficiaries of the amount due.

Step 4 – Pay benefits. There are then three options for actually settling the IHT bill: pay it from the free estate (before probate is granted); instruct the pension scheme to pay it directly to HMRC; or have the beneficiaries pay the IHT themselves, coordinated by the personal representative.

For someone with a single pension, this adds a layer of complexity. For someone with multiple pensions accumulated over a working life – perhaps an old workplace scheme here, a SIPP there, a small preserved benefit elsewhere – it could become an administrative nightmare. We return to this point later.

Planning implications – nine things to consider

1. Pensions Are Still Great

We see some younger clients dismissing pension saving for fear that “the Government will just tax it all anyway.” This is understandable but wrong (in our view).

The combination of upfront income tax relief on contributions, tax-free investment growth, and 25% tax-free cash on withdrawal (up to the current lump sum allowance of £268,275) means pensions are, generally speaking, still the best vehicle for building long-term wealth.

That’s notwithstanding the valid trade-off between tax efficiency and accessibility – you are locking funds away until the minimum pension age (currently 55 but set to rise to 57 over the next two years). But the tax advantages remain compelling.

2. But They Should be Spent

However, the days of using pensions as an estate planning tool are clearly numbered.

The presence of the double death tax means pension savings should ideally be spent in retirement. Build a pension. Spend a pension.

We’ve talked before about £1.1–1.2 million being the ‘magic number’ for pension savings – roughly equivalent to the maximum tax-free cash entitlement combined with scope to draw the balance over an average life expectancy at the basic rate of income tax only. This kind of planning becomes even more important from April 2027.

3. Annuities Are a Relative Winner

The reduced death benefits of drawdown pensions (with up to 40% potentially lost to IHT) weaken one of the traditional arguments against annuity purchase.

In simple terms, why retain a large drawdown pot—exposed to IHT and potentially income tax on withdrawal—when an annuity can convert this into a guaranteed income for life?

This shift is reinforced by a significant improvement in annuity rates. A healthy 65-year-old can now secure around 7.5% income on a level, single-life basis with a 10-year guarantee [source: AMS, as at 01/04/2026] —around 50% higher than in 2021. For many, this combination of income certainty and improved tax efficiency makes annuities increasingly attractive.

As noted in previous commentary, a blended approach often works well: using annuity income to cover essential spending (plus a margin of comfort), while retaining drawdown for more flexible, discretionary expenditure such as holidays and hobbies.

4. Don’t Act Hastily

For most people our advice is to wait until the new rules actually come into effect. Who knows whether there will be a late U-turn? We’ve seen it elsewhere.

And critically, if you were to die between now and 6 April 2027, your pension still sits outside your estate for IHT. Making drastic changes now could mean giving up a tax advantage you currently have.

5. But Don’t Wait for a New Government Either

We’d be reticent about the school of thought that says “wait for the next election – a new government might reduce or abolish IHT entirely.” We think it’s right to play the cards in front of you in terms of current tax rules. Historically, removing a potentially major revenue earner has been politically challenging regardless of which party is in power. Plan for the rules as they are, not as you hope they might become.

6. Consider Generation Skipping

Death benefit nominations will become much more important, particularly around the age-75 rule which determines whether income tax is payable on an inherited pension.

For example, those who have reached 75 might consider whether it makes sense to skip the next generation and leave pension benefits directly to grandchildren. If the grandchildren are non-earners or low earners, they will have their personal allowance or only incur basic-rate tax on subsequent withdrawals – a far better outcome than a higher-rate taxpayer child receiving the same benefit. It’s worth noting that where a pension is inherited by a minor, their parents or guardians can draw on the money for their benefit until the child turns 18, at which point the child will have unrestricted access.

7. Manufacturing Surplus Income for Gifting

This is a strategy we are particularly excited about. If you accelerate pension drawdown or purchase an annuity to create a regular income surplus – more income than you need to maintain your normal standard of living – those surplus amounts can potentially be given away during your lifetime under the Normal Expenditure out of Income exemption.

Gifts made under this exemption are immediately outside your estate for IHT. No seven-year waiting period.

The arithmetic can be very attractive. Draw pension income as a basic-rate taxpayer: you pay 20% income tax on the withdrawals, but by gifting the money straight out, this then sits (immediately) outside your estate, saving your beneficiaries 40% IHT and a second round of income tax. A net saving of 20% – and you get to see your family benefit from the gifts during your lifetime.

Better still, you could make the gift into a child’s or grandchild’s pension, where it would then qualify for income tax relief at the recipient’s marginal rate. This creates a supremely tax efficient loop: withdraw from your pension, gift the surplus, and the recipient gets tax relief on the contribution at the other end.

8. Or Use Surplus Income to Fund Life Insurance

Rather than gifting, you could use some or all of the surplus income to purchase a whole-of-life insurance policy written in trust.

The policy pays a tax-free lump sum on death which is then readily available to settle some or all of the IHT bill, without the delays of dealing with pension schemes and HMRC. We’ve written before about how the maths can stack up very nicely on this strategy and will be revisiting it in detail in a forthcoming blog.

9. Die Tidily

Under the new rules, your executors will need to inform and subsequently liaise with each pension scheme, instructing them to hold funds back for IHT, arranging for IHT to be paid, and coordinating the release of funds to beneficiaries. For someone with multiple pension schemes accumulated over a working life, this has the potential to become an administrative nightmare. Best to die tidily.

Consolidating multiple pensions into a single arrangement now – where appropriate – will make life considerably easier for your executors and beneficiaries when the time comes.

The Financial Conduct Authority does not regulate tax advice. Levels, bases, and reliefs from taxation may be subject to change, and their value depends on the individual circumstances of the investor.

The bottom line

The proposed new pension rules have received Royal Assent and therefore look set to go ahead as planned, making this one of the most significant changes to pension taxation in a generation.

For some families, this will mean a significant increase in the tax payable on death – potentially running to tens or even hundreds of thousands of pounds.

But this is not a cause for panic. It is a call to plan. The tax landscape has shifted, and the strategies that served people well for the past decade need revisiting. Pensions remain excellent vehicles for building wealth – just not for sheltering it from IHT in the way they once were.

As always, if you would like to discuss how these changes affect your own circumstances, please do get in touch. We are here to help you navigate what comes next.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.