Why Whole-of-Life Insurance Still Matters for Inheritance Tax Planning

‘It’s insurance Jim, but not as we know it’

Whole-of-life insurance can play an important role in inheritance tax planning by providing a guaranteed, tax-free lump sum to help beneficiaries settle an eventual IHT liability. While it doesn’t reduce the tax itself, it can be a highly effective solution for illiquid, property-heavy, or gain-laden estates where other planning strategies may be limited or inefficient.

As an Inheritance Tax (IHT) planning tool, insurance is a ‘tough sell’.

When discussing with clients, I can immediately feel the energy leaving the room. And that’s completely understandable. With alternative options, such as gifting, trust planning, and Business Relief investments, there’s a feeling of ‘beating the system’ by mitigating a potential IHT charge. Whereas with insurance, you’re merely providing for it. It feels like waving the white flag.

However, despite its unpopularity, ‘whole-of-life’ insurance cover has a legitimate place in the estate planning toolkit. For certain clients — particularly those with illiquid estates, heavily gain-laden property portfolios, or estates where the IHT charge is simply unavoidable whole-of-life insurance can represent one of the most practical and predictable solutions available.

What’s more, the economics are often more attractive than many people initially assume. In the right circumstances, the trade-off between the monthly premium and the eventual tax-free payout can be remarkably compelling, particularly when viewed against the scale of the potential inheritance tax liability.

What is Whole of Life Insurance?

Most people’s experience of life insurance is term insurance. You take out a policy for a fixed period — say 25 years to match your mortgage for example — and if you die during that term, it pays out. If you don’t die, the policy expires worthless. You’re paying for protection against a risk that might not materialise.

Whole-of-life insurance is fundamentally different. There is no fixed term. The policy runs for your entire life, and it will always pay out (assuming you keep up with paying the premiums). The question is not if it pays out, but when.

That distinction matters enormously. Because death is certain, the policy is guaranteed to deliver a return. It should therefore be thought of less as “insurance” in the traditional sense, and more as a transfer of value: you pay premiums during your lifetime, and in return your beneficiaries receive a tax-free lump sum on your death.

Note, life assurance plans typically have no cash in value at any time and cover will cease at the end of term. If premiums stop, then cover will lapse.The Financial Conduct Authority does not regulate Estate and Inheritance Tax Planning. Inheritance Tax thresholds depend on your individual circumstances and may change in the future.

How It Works in Practice

The key to using whole-of-life insurance for IHT planning is that the policy must be written in trust. This is a critical step that is sometimes overlooked, and getting it wrong defeats the entire purpose.

When a policy is written in trust:

The policy proceeds sit outside your estate for IHT purposes, i.e. the payout is not subject to inheritance tax.

The funds are available to your beneficiaries immediately on death. There is no need to wait for probate, no need to apply for a grant of representation, and no delay in accessing the money.

Your beneficiaries receive a tax-free lump sum that can be used to settle the IHT bill, preventing the need to sell assets under pressure.

The Case For and Against

The Advantages

Simplicity. Whole-of-life cover is straightforward to set up and straightforward to understand. You pay premiums. Your beneficiaries receive a lump sum. There’s no complex trust structure to manage (beyond the policy trust itself), no ongoing compliance burden, and no need to revisit the arrangement every year (assuming you opt for a ‘guaranteed’ policy - our preference - where the sum assured and cost, aka. ‘Premium’, remain the same throughout).

Day-one cover. Unlike gifting (which requires a seven-year survival period to be fully effective), whole-of-life cover works from the moment the policy is in force. If you die the day after taking out the policy, it pays out in full.

Regulatory resilience. Other IHT planning strategies are more vulnerable to legislative change. Business Relief has already been scaled back, with qualifying thresholds and rules tightened in recent Budgets. Pension IHT treatment is being overhauled from April 2027. Whole-of-life insurance, by contrast, has been largely untouched by successive governments. It’s a simpler target for regulators to leave alone.

Certainty. You know exactly what your beneficiaries will receive. There is no market risk, no sequencing risk, and no risk of legislative change eroding the benefit.

The Drawbacks

You’re providing, not mitigating. This is the big one. Whole-of-life cover doesn’t reduce your IHT liability by a single penny. It simply provides a pot of money to pay it. For many people, that feels like an admission of defeat — like paying the taxman in advance rather than finding a way around the charge. Psychologically, it’s a hard sell. And I understand that reaction completely.

Premiums feel expensive. Monthly premiums for whole-of-life policies are materially higher than term insurance because the insurer knows the policy will eventually pay out. However, the cost should be considered in the context of the guaranteed payout and the potential inheritance tax liability being insured against. Term insurance is cheaper because it only pays out if death occurs during the policy term, whereas a whole-of-life policy is intended to provide certainty that funds will be available whenever they are ultimately needed.

Opportunity cost. Every pound spent on premiums is a pound that could have been invested. This is a legitimate concern, and one we explore in detail below.

Review periods. Whole-of-life policies can typically be arranged on either a guaranteed basis (where premiums and cover remain fixed throughout) or a reviewable basis (where premiums start lower but are periodically reviewed — and usually increased — often every ten years). We generally favour guaranteed policies, as reviewable plans introduce budgeting uncertainty and can become prohibitively expensive later in life, precisely when the cover is likely to be needed most.

Do the Maths Stack Up?

This is the question that rightly comes up often, and the answer is more nuanced than most people think.

The Naïve Breakeven

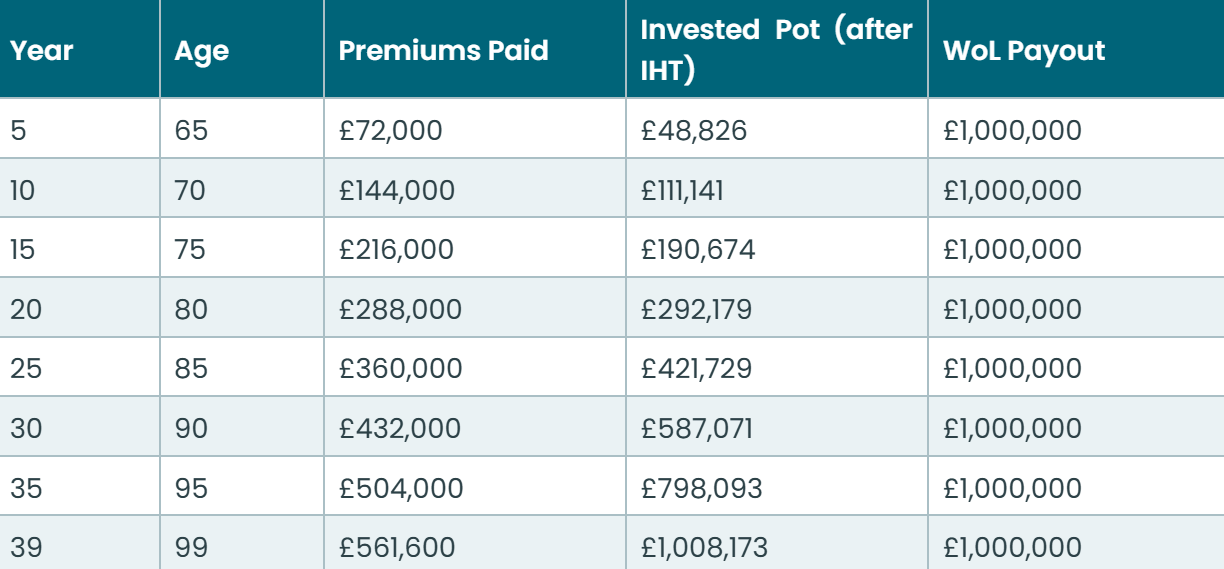

Take a 60-year-old male, in good health, who takes out £1,000,000 of whole-of-life cover, on a guaranteed basis, at a cost of £1,200 per month or £14,400 per year [source: AssureWeb].

The simple breakeven — total premiums paid equalling the sum assured — occurs after approximately 69 years, at age 129, well beyond any reasonable life expectancy. By this measure, the policy looks like excellent value.

But that calculation is misleading, because it ignores a crucial factor: opportunity cost.

The Real Breakeven

What if those £1,200 per month premiums were invested instead? Assuming a net return of 5% per year (after charges), the invested pot would compound over time.

Note these figures are for illustrative purposes only and do not reflect actual investment returns, which can fluctuate and are not guaranteed.

But critically, unlike a whole-of-life policy written in trust, the investment portfolio would usually form part of your estate on death and could therefore be subject to inheritance tax at 40% (depending on the size of the wider estate and available allowances). In practical terms, this means your beneficiaries may ultimately receive as little as 60% of the portfolio’s value after tax.

The whole-of-life policy, by contrast, pays out £1,000,000 tax-free (because it’s held in trust).

The question then becomes: at what point does the after-tax value of the invested premiums overtake the £1,000,000 tax-free payout?

On the assumptions stated, the opportunity cost breakeven is approximately age 99 — around 39 years of premiums. That’s thirty years sooner than the naïve calculation suggests, but still well beyond average life expectancy. For a 60-year-old male, the ONS estimates an average further life expectancy of around 22 years (to age 82). At that point, the invested alternative would have delivered only around £340,000 after IHT, compared with a £1,000,000 tax-free payout from the policy.

Of course, the real breakeven will depend greatly on the tax position of those funds, and the average investment returns. But on the evidence presented, the maths of WoL cover still stack up favourably.

Where We Think Whole-of-Life Cover Fits Best

For what it’s worth, we generally share our clients’ instinctive resistance to whole-of-life cover. With early planning, there should be scope to reduce an IHT charge through gifting, trust strategies, and Business Relief investment — all supported by thorough cashflow modelling to make sure you can comfortably fund your own lifestyle with a healthy war chest for unexpected costs.

But whole-of-life cover comes into its own in a specific set of circumstances. The clearest use case is an estate that is skewed towards illiquid assets — most commonly, property.

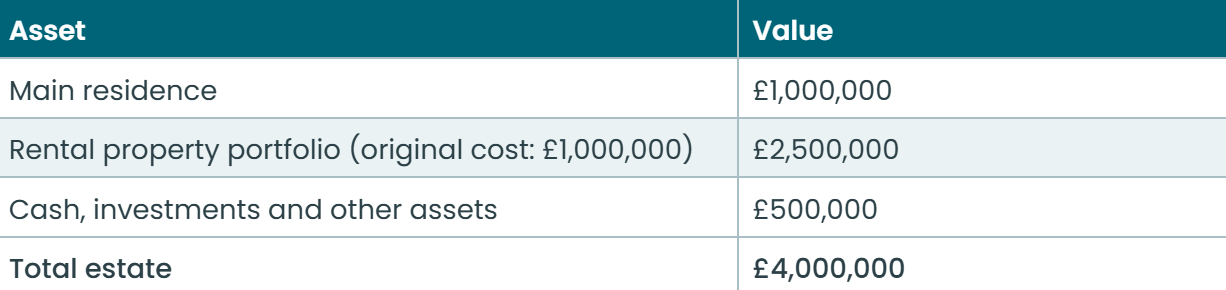

Worked Example: The Property-Heavy Estate

Michael and Jane are married with two adult children. Their estate is valued at £4 million, comprising:

The IHT Position

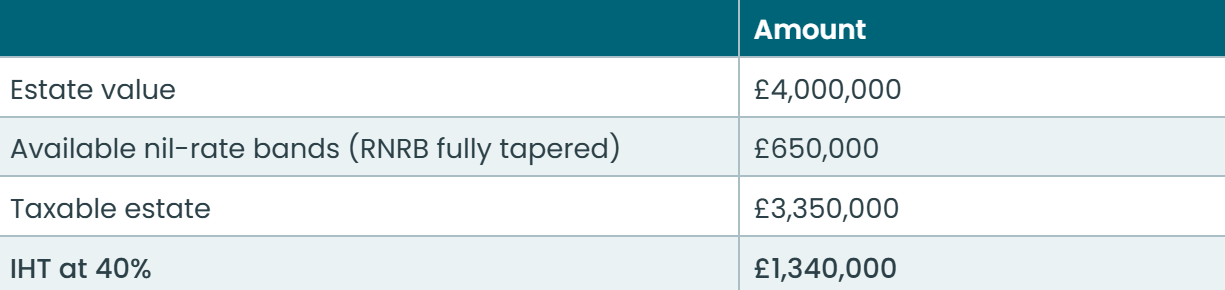

At £4 million, the estate is well above the £2 million taper threshold. The Residence Nil-Rate Band (RNRB) is fully tapered away (as we discussed in last week’s blog). Their available nil-rate bands are limited to the standard £650,000 (2 × £325,000).

Per the above, they fact a potential £1.34 million IHT bill. And a key issue is that most of their property is locked up in bricks and mortar.

Why Selling Isn’t Straightforward

The obvious option might be to sell some rental properties, use the proceeds to make lifetime gifts, and reduce the estate. But in this example, the rental portfolio carries an unrealised gain of £1.5 million (current value £2.5 million less original cost £1 million). Selling would trigger Capital Gains Tax at 24%, costing approximately £360,000.

Under current rules, if Michael and Jane hold the properties until death, that £1.5 million gain is wiped out entirely. Their children inherit the properties at current market value with no CGT to pay. This “base cost uplift on death” is one of the most valuable features of the UK tax system — and selling in order to gift effectively throws it away.

Even worse, as we explored in an recent blog - Five UK Tax Traps to Avoid in 2026 (And How to Plan Around Them) - if they sell, gift the proceeds, and then die within seven years, the gift becomes a failed PET and the cash is brought back into the estate for IHT — with no credit for the CGT already paid. The same wealth could be taxed twice!!

Where Whole-of-Life Cover Comes In

Rather than selling (and triggering CGT), Michael and Jane can use the rental income from their portfolio to fund a whole-of-life policy written in trust.

Their gross rental yield is approximately 5%, generating around £125,000 per year. Assuming they’re in good health, a policy covering the full £1.34 million IHT liability might cost in the region of £1,600 per month (£19,200 per year) on a guaranteed basis (same premium and cover throughout) — roughly 15% of their gross rental income. That’s a meaningful cost, but manageable within the context of their wider income.

The result:

The rental properties are held until death, preserving the CGT base cost uplift and avoiding a £360,000 CGT charge

On death, the policy pays £1.34 million tax-free directly to the beneficiaries — no probate delay, no pressure to sell, available to settle against the IHT bill

In this scenario - an estate consisting mostly of gain-laden illiquid assets - whole-of-life insurance offers a particularly effective solution.

Reframing the Conversation

Part of the resistance to whole-of-life insurance stems from how it is perceived. Whilst technically a form of “insurance”, the label places it in the same mental category as car or home insurance — something you pay for hoping never to claim on it.

But whole-of-life cover is fundamentally different. It is designed to pay out; the only variable is when.

In our view, a more helpful way to think about it is as pre-funding a future inheritance tax liability. Rather than leaving beneficiaries to settle an IHT bill from the estate itself, the policy creates a dedicated, tax-free pool of liquidity to meet that liability when it arises.

It also supports the principle of “dying tidily” — ensuring funds are immediately available to pay any inheritance tax due, without forcing the sale of assets or creating unnecessary financial pressure for the family at an already difficult time.

The Bottom Line

Whole-of-life insurance is unlikely to be the most exciting estate planning tool. It does not eliminate inheritance tax or rely on complex planning. But for estates that are illiquid, gain-laden, or simply too large to mitigate fully, it offers something many alternatives cannot: simplicity and certainty.

Our approach is to use it alongside other strategies, not instead of them. Reduce the liability where possible through gifting, trusts, and efficient structuring. Then model any residual exposure through cashflow planning. Where an IHT charge is genuinely unavoidable, pre-funding it at a fraction of the eventual liability may be preferable to leaving your family to settle the bill later via sales of illiquid assets.

Happy Thursday!

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.