Five UK Tax Traps to Avoid in 2026 (And How to Plan Around Them)

Five UK Tax Traps - and How to Avoid Them

The UK tax system contains several hidden “tax traps” where earning more or holding additional wealth can actually leave you worse off due to steep marginal rates and lost allowances. Understanding these traps — and how to plan around them — is key to avoiding unnecessary tax and keeping more of what you earn.

“It’s a trap!” - the immortal words of Admiral Ackbar in Star Wars: Return of the Jedi.

While we’re not navigating the Death Star, the UK tax system has traps of its own. It’s a Byzantine patchwork of allowances, thresholds, tapers and cliff edges — stitched together over decades by successive governments. The result is a system where earning slightly more, or holding slightly too much, can leave you materially worse off.

In this week’s blog, we walk through five of the most punishing tax traps in the current system, explain how they work in practice, and — crucially — outline the planning strategies that can help you avoid them.

Please note, the Financial Conduct Authority does not regulate tax advice. Tax rules, reliefs and allowances may change, and their value depends on individual circumstances.

Trap 1: The 60% Tax Trap (and Why It’s Even Worse for Parents)

This is the most well-known trap on the list.

If you earn between £100,000 and £125,140, you lose £1 of your tax-free personal allowance for every £2 of income above £100,000. The result is an effective marginal tax rate of 60% — made up of 40% higher-rate tax, plus an additional 20% from the shrinking allowance.

Painful on its own. But for parents of young children, it gets significantly worse.

The Childcare Cliff Edge

The UK’s funded childcare entitlement — up to 30 hours per week for 38 weeks a year, available from when a child is 9 months old until they start school — is only accessible where each parent’s adjusted net income does not exceed £100,000. The same threshold applies for Tax-Free Childcare, under which the government adds £2 for every £8 paid into a childcare account (up to £2,000 per child per year).

However, these benefits don’t taper, they disappear entirely the moment either parent earns £100,001. It’s a cliff edge, not a slope.

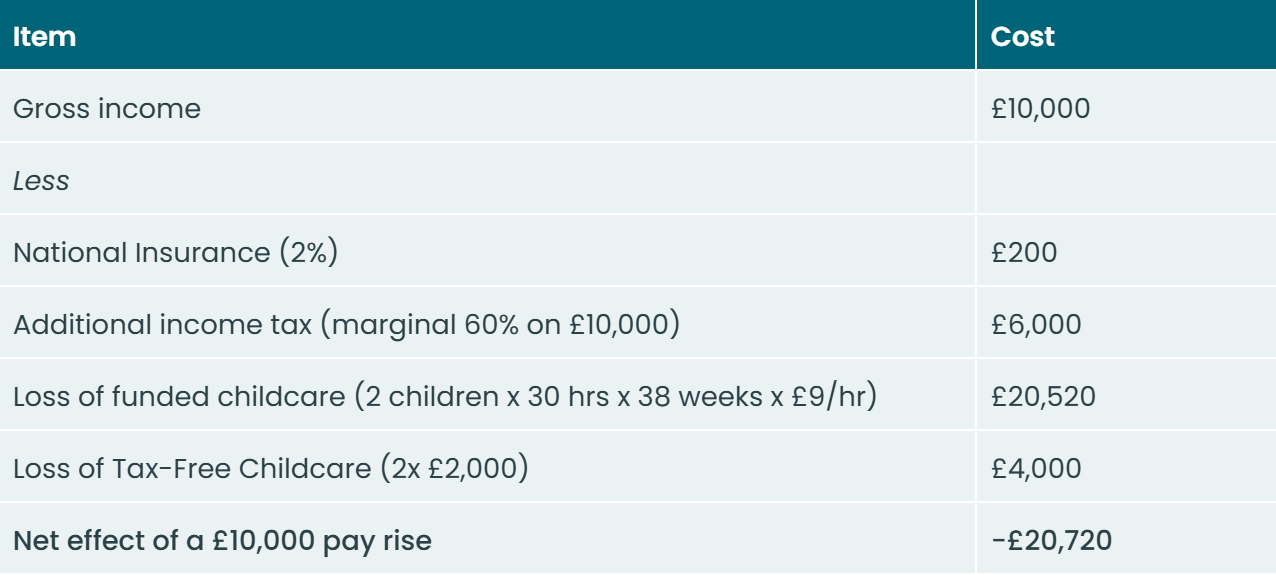

‘Worst-Case’ Example

Libby earns £100,000 and has twins aged two, attending nursery five days a week (8am–5pm) at £9 per hour. Her partner earns below £100,000. She receives a £10,000 pay rise, taking her income to £110,000.

Here’s what she loses:

In other words, a £10,000 pay rise has actually left Libby over £20,000 worse off. Her effective marginal tax rate exceeds 200%.

The Solution: Pension Contributions

The most effective planning tool here is a pension contribution.

If Libby contributes £10,000 (gross) into her pension, her adjusted net income falls back to £100,000. This achieves several things at once:

Restores her full personal allowance (creating effective 60% tax relief)

Reinstates funded childcare (saving over £20,000)

Restores Tax-Free Childcare (saving £4,000)

In total, the pension contribution delivers effective tax relief in excess of 200%. If available, salary sacrifice improves this further by reducing National Insurance as well.

A pension is a long-term investment and funds are not normally accessible until 55 (rising to 57 from April 2028). When investing via a pension, your capital is at risk. The fund value may fluctuate and can go down. Your pension income could also be affected by the interest rates at the time you take your benefits.

Trap 2: The Child Benefit Tax Trap

A similar — though less extreme — trap exists further down the income scale.

The High Income Child Benefit Charge applies where one partner’s income exceeds £60,000. Child Benefit is clawed back at a rate of 1% for every £200 of income above this level, disappearing entirely by £80,000.

For a family with two children, that’s around £2,300 a year at stake; for three children, over £3,200.

Crucially, this is assessed on individual income — meaning a single earner at £80,000 loses everything, while a couple earning £59,999 each keep the full benefit.

The Solution: Pension Contributions (Again)

Once again, pension contributions can reduce adjusted net income below £60,000 and eliminate the charge entirely.

However, in reality, families facing high childcare costs may struggle to fund additional contributions at these income levels.

One underused solution here is third-party contributions. A parent or grandparent can contribute to your pension, helping reduce your tax liability while also supporting longer-term family wealth planning. In fact, this can double as an inheritance tax strategy - something we’ll explore in more detail in an upcoming blog.

Trap 3: Double Death Tax — Sell, Gift, Die

This one flies under the radar — but it can be brutal in practice.

It typically affects those with assets carrying large capital gains, most commonly buy-to-let property.

Here’s the sequence:

You sell an asset and pay Capital Gains Tax (CGT).

You then gift the proceeds to your children.

…But die within seven years.

The gift becomes a failed Potentially Exempt Transfer (PET), meaning the full value is pulled back into your estate and taxed at up to 40% for inheritance tax (IHT).

And here’s the sting: there’s no credit for the CGT already paid.

The same wealth is effectively taxed twice — once on the asset sale, and again on death.

Why Not Just Hold the Asset?

Under current rules, capital gains are wiped on death. Your beneficiaries inherit the asset at market value — with no CGT to pay. This “base cost uplift” is one of the most generous features of the UK tax system - holding on to a gain-laden asset until death, will effectively wipe out the potential CGT charge.

Of course, that doesn’t help solve an ‘IHT problem’. But one underused solution here is whole-of-life insurance, written in trust.

Instead of triggering CGT by selling, you retain the asset and use rental income to fund a policy designed to cover the future IHT liability.

Because the policy is held in trust:

The payout sits outside your estate

Funds are available immediately (no probate delays)

Assets don’t need to be sold in a hurry

Done properly, the numbers can stack up well — with total premiums often significantly lower than the eventual tax saved. Again, we’ll be revisiting this in an upcoming blog.

Trap 4: Double Death Tax — The New Pension Rules

From 6 April 2027, unused pension funds will be included in your estate for IHT purposes.

Combine that with the existing rules — where beneficiaries pay income tax on withdrawals if you die after age 75 — and you have the potential for double taxation:

40% IHT on death

Then income tax at the beneficiary’s marginal rate

At higher rates, this can erode close to two-thirds of the pension.

We covered this in detail in a recent blog (The ‘Double Death Tax’: How Pensions Will Be Taxed from 2027), including practical planning strategies.

The key takeaway is that pensions remain highly effective for building wealth — but no longer for sheltering it from IHT. Build a pension. Spend a pension.

Trap 5: The 60% IHT Rate — When Estates Creep Over £2 Million

Most people know IHT is charged at 40%.

Fewer realise that, in certain circumstances, the effective rate rises to 60%.

This happens because of the so-called Residence Nil-Rate Band (RNRB) — the additional £175,000 allowance available when passing a home to direct descendants.

However, once an estate exceeds £2 million, the RNRB is withdrawn at a rate of £1 for every £2 above the threshold.

The effect is that, within the taper range (£2m–£2.35m for an individual and £2m–£2.7m for a couple), every additional £2 of estate value results in £1 of allowance being withdrawn — and that £1 is then taxed at the standard 40% IHT rate. Combined with the underlying 40% charge on the estate itself, this creates an effective 60% tax rate within the taper band.

From April 2027, the new pension rules outlined in point 4 will bring unused pension funds into the estate for IHT purposes, meaning many more families are likely to be caught by this effective 60% IHT band.

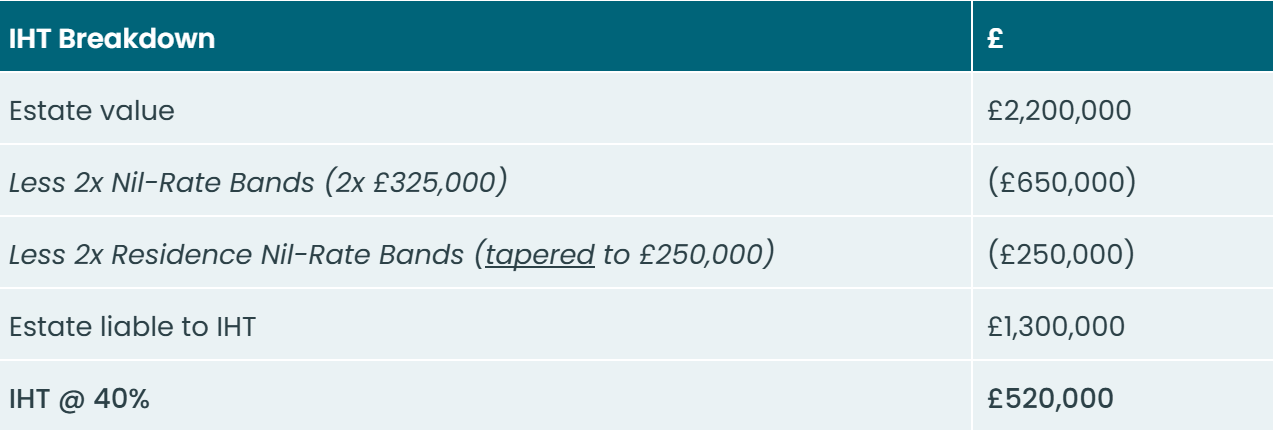

Worked Example

John and Helen have a combined estate of £2.2 million, including a £600,000 family home that they intend to leave to their children.

Their IHT position is as follows:

As you can see, because their estate exceeds the £2m threshold, part of their Residence Nil-Rate Band (RNRB) is tapered away — reduced by £1 for every £2 above £2m — bringing it down from the full £350,000 (£175,000 each) to £250,000.

Now suppose John and Helen reduce their estate by £200,000, whether through gifting or simply spending it. This restores their full RNRB, increasing the total exempt amount from £900,000 to £1 million.

As a result, the portion of the estate subject to IHT falls from £1.3 million to £1 million, reducing the tax bill to £400,000. The net effect is a £120,000 IHT saving from a £200,000 reduction in the estate.

The Planning Opportunity: Get Below £2 Million

This is one of the few areas of tax planning where the benefit is immediate.

Unlike gifting rules, there’s no seven-year clock. If your estate is below £2 million at death, you get the full RNRB — simple as that.

For families hovering around this level, relatively modest planning — gifting, spending, or restructuring — can deliver disproportionately large tax savings.

The Bottom Line

The UK tax system has evolved into a complex maze of thresholds, tapers and cliff edges where:

A modest pay rise can leave you worse off

Selling and gifting assets can trigger double taxation

Holding slightly too much wealth can push tax rates from 40% to 60%

But these traps aren’t unavoidable. With the right planning — pension contributions, gifting strategies, insurance, and estate structuring — they can often be sidestepped entirely.

If you’d like to discuss any planning opportunities further, please let us know.

Happy Thursday!

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.