Gilts Explained: A Tax-Efficient Alternative to Cash for Higher-Rate Taxpayers

The Case for UK Government Bonds Today

Low-coupon UK gilts can offer higher and additional rate taxpayers a largely tax-free return of around 4%, thanks to their exemption from capital gains tax. In today’s market, that can make them more attractive than cash savings once tax is taken into account.

It’s been a choppy few weeks for financial markets. Most of the attention has been on equities, but bond markets have seen their fair share of volatility too.

Rising tensions in the Middle East have pushed oil prices higher, lifting inflation expectations and, in turn, nudging interest rate expectations upwards.

The knock-on effect is that UK gilt yields have moved back up to around 4%. For higher and additional rate taxpayers holding cash outside an ISA or pension, that could present an opportunity.

What is a Gilt?

A gilt is a bond issued by the UK Government.

In simple terms, when the government needs to borrow money, it issues these ‘IOUs’ to investors. By buying a gilt, you’re effectively lending money to the government in return for two things:

a fixed repayment at a future date, and

a small amount of interest paid twice a year (known as the coupon).

Gilts trade on the London Stock Exchange, much like shares, so their prices move over time. These movements are largely driven by changes in interest rates — when rates rise, existing bond prices typically fall, and vice versa.

Crucially, when a gilt matures, the government repays £100 per unit — its “par” value.

Here’s where things get interesting. UK gilts are exempt from capital gains tax. This means that if you buy a gilt below £100 and hold it to maturity, the uplift back to £100 (often referred to as the “pull to par”) is completely tax-free. This is a quirk of UK tax rules and is unique to gilts.

The coupon payments are still subject to income tax at your marginal rate. However, by selecting gilts with low coupons and buying them at a discount to par, most of your return can come from that tax-free capital uplift rather than taxable income.

For higher and additional rate taxpayers, this can be particularly attractive. It means keeping more of your return, rather than losing a significant portion to income tax as you would with a standard savings account via a bank of building society.

Note, when investing, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invested. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. The Financial Conduct Authority does not regulate tax advice. Levels, bases, and reliefs from taxation may be subject to change, and their value depends on the individual circumstances of the investor.

A worked example

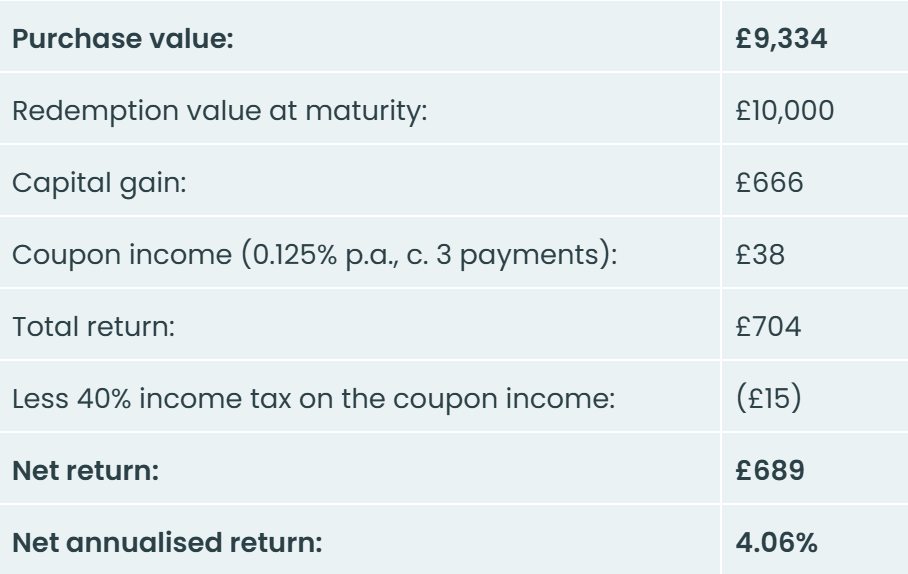

Let's take the 0.125% Treasury Gilt maturing on 31 January 2028 (known as TN28).

At the time of writing, this gilt is trading at around £93.34 per £100 of nominal value.

Consider a £9,334 investment by a higher-rate taxpayer:

Of that £689 return, £666 comes from the capital gain (the ‘pull to par’) — which is entirely free from capital gains tax. The £38 of coupon income is taxable, but at such a low level, it’s largely negligible.

In other words, almost the entire return is effectively tax-free.

How Does this Compare to Cash?

At the time of writing, the best easy access savings rates are around 4.75% (source: Moneyfacts). On the face of it, that looks more attractive.

However, the interest is fully taxable.

For a higher-rate taxpayer (assuming their £500 Personal Savings Allowance is already used), that reduces the net return to 2.85%. For an additional-rate taxpayer, it falls further to 2.61%.

In fact, to match a near-4% tax-free gilt return, a savings account would need to offer:

In other words, a higher-rate taxpayer would need a savings account paying around 6.7% gross just to stand still after tax. An additional-rate taxpayer would need 7.3%. Neither of those rates are available anywhere reputable right now.

This is often referred to as the “gross equivalent yield” — the headline rate required to match a given after-tax return.

The risks

As with any investment, it’s important to consider the potential risks and drawbacks of investing in gilts.

Price volatility

Gilts are not the same as cash in a bank account. Their prices fluctuate daily on the secondary market. If you need to sell before maturity, you may receive less than you originally invested.

If inflation expectations rise further, gilt prices could fall in the short term before recovering. While the “pull to par” is effectively assured at maturity, the path there can be volatile. It is therefore important to be comfortable holding the investment until the redemption date and not relying on the funds for short-term needs.

Interest rate risk

Changes in interest rates are the primary driver of gilt prices. Rising rates typically lead to falling prices in the short term.

Again, this is less relevant if you hold the gilt to maturity, but it becomes important if there is a possibility of needing to sell early.

Reinvestment risk

Coupon payments are received twice a year and may need to be reinvested at prevailing market rates, which could be lower.

For low-coupon gilts, this risk is relatively minor given the small size of the income payments, but it is still worth acknowledging.

Government default risk

There is also the theoretical risk that the UK government fails to meet its obligations. In practice, this is widely considered extremely unlikely - the UK has never defaulted on its domestically issued debt and, as a sovereign issuer of its own currency, has significant flexibility in meeting sterling-denominated liabilities.

That said, no investment is entirely risk-free, and it is important to recognise this — even if it remains firmly in the “remote” category.

Who Might This Suit?

Gilts may be particularly suitable for:

Higher and additional rate taxpayers holding cash outside ISAs (i.e. where ISA allowances have already been fully utilised) or pensions

Investors with a defined time horizon (e.g. 1–3 years) who want a low-risk return aligned to a specific future need

Those seeking an alternative to cash without taking on equity market risk

In Summary

The opportunity with gilts is simple but often overlooked. For higher earners, where tax can significantly erode cash returns, low-coupon gilts offer a way to achieve a competitive return with most of it effectively tax-free.

With yields around 4%, and equivalent savings rates closer to 6.7–7.3% on a gross basis, the case is compelling for the right investor.

As always, suitability depends on your broader financial position — including your tax status, time horizon and liquidity needs. If you’d like to explore whether gilts could play a role in your plan, feel free to get in touch.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.