Should You Sell When Markets Fall? Why Staying Invested Matters During Volatility

Stock Markets Tend to Grind Higher Over Time - But the Ride Is Never Smooth

There’s an old saying in financial markets: stocks take the escalator up and the lift shaft down.

It captures a long-term trend - markets tend to grind higher over time: slowly, steadily, sometimes almost boringly. But when they fall, they fall fast. Sharp, sudden, and often without warning. It’s an asymmetry that catches investors off guard, particularly when headlines turn ugly. And each time, it feels different - more serious, more structural, more concerning than what came before.

Right now, the headlines are particularly ugly. 2026 has already delivered a barrage of geopolitical and economic shocks: a US threat of invasion against Greenland; a renewed outbreak of war in the Middle East; rising concerns around a private credit meltdown (highlighted by Blue Owl halting redemptions); and a sharp reassessment of interest rate expectations, driven in part by higher oil prices. And it’s not even the end of the first quarter.

Please note, when investing, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invested, particularly if you invest for a short timeframe. Neither simulated nor actual past performance is a reliable indicator of future performance. Investments should be considered over the longer term and align with your overall attitude to risk and financial circumstances.*

Resilient, but Teetering

The immediate focus is, inevitably, on Iran. Air strikes and targeted attacks on energy infrastructure — on both sides — have effectively closed the Strait of Hormuz, the narrow waterway through which roughly a fifth of the world’s oil and natural gas typically flows.

The result has been a sharp surge in energy prices, with oil rising from around $70 per barrel to circa $120 in a matter of weeks.

For now, equity markets have held up relatively well. Most are ‘only’ around 5% below recent highs and, in many regions, remain broadly flat for the year following a strong start in January and February.

But that resilience feels fragile.

The consensus view among analysts and commentators is that the path of least resistance is lower. The longer the conflict persists, the greater the disruption to energy supply; the greater the pressure on inflation; and, in turn, the higher the likelihood of tighter monetary policy (i.e. higher interest rates, or at least fewer rate cuts than previously expected) to contain it.

That latter point is key because interest rates remain the single most important driver of equity valuations. Higher rates reduce the present value of future cash flows and increase borrowing costs - both of which act as a headwind for markets.

Of course, the situation could change overnight. A de-escalation is entirely possible - the US could pull back from further strikes, or a diplomatic agreement could be reached. In that scenario, oil prices would likely normalise, equity markets would recover, and we can all stop pretending to be experts on the Strait of Hormuz.

What to Do

In times like these, there’s an almost irresistible urge to act. Perhaps to sell everything and move to cash until things calm down. It feels like the responsible thing to do.

But the problem with that approach is simple: the market doesn’t ring a bell at the bottom.

That may sound flippant, but it reflects the notion that the stock market is a highly efficient, forward-looking mechanism — pricing in expectations and aggregating the views of millions of participants and trillions of dollars, every single day.

History shows that markets begin to recover long before the news feels comfortable. By the time headlines improve, the rebound is often already well underway. If you wait for things to “calm down” — for sentiment to shift, for conflict to resolve, for oil prices to normalise — you will almost certainly be buying back in at higher levels. Markets don’t wait for good news; they anticipate it.

The Cost of Trying to Time the Market

The cost of getting this timing wrong can be significant.

A large proportion of long-term market returns is driven by a small number of very strong days — and crucially, those days often occur when sentiment is at its worst. Periods of maximum pessimism and maximum opportunity tend to coincide.

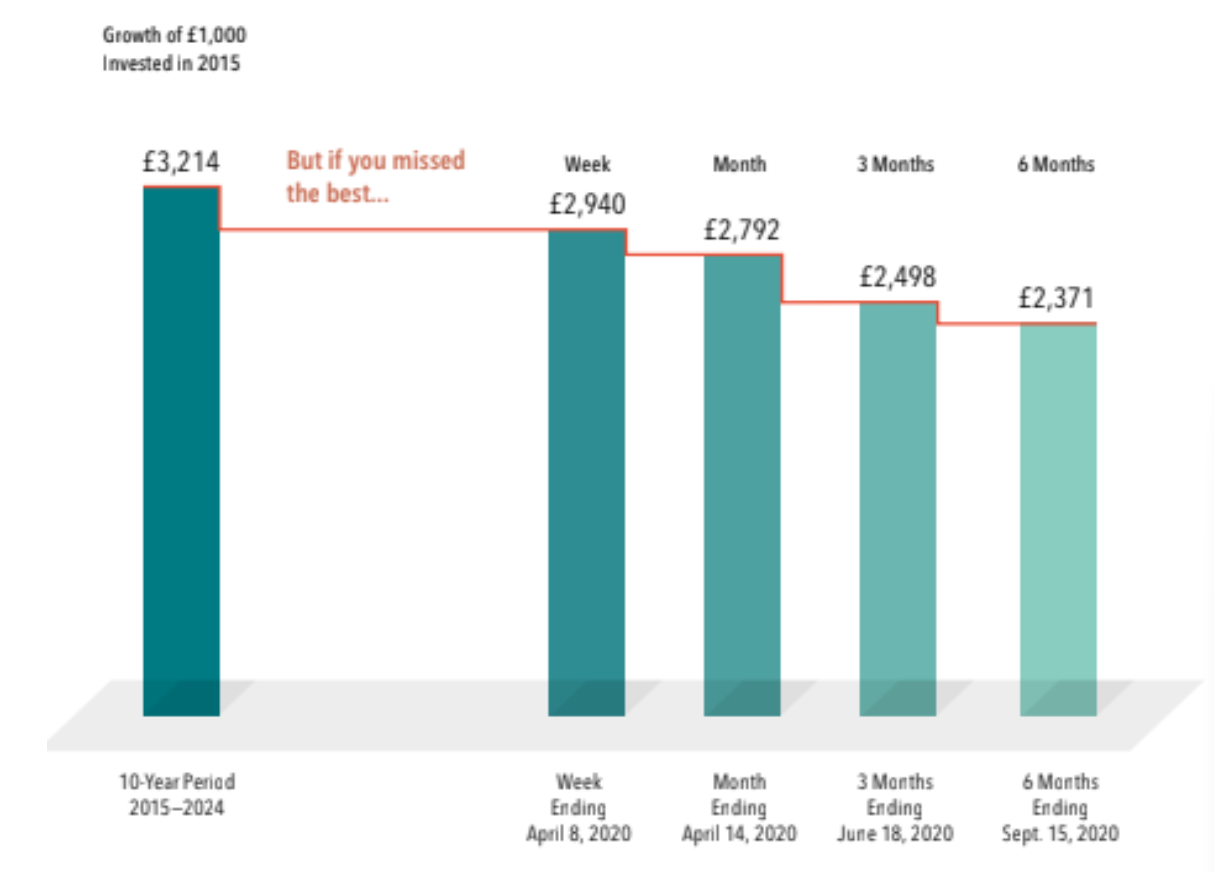

Research from Dimensional Fund Advisors illustrates this clearly. Based on the MSCI World Index (a proxy for global equities), a hypothetical £1,000 investment made in 2015 would have grown to £3,214 by the end of 2024 — a return of 221%, or circa 12.4% per annum.

Miss just the best week, and that falls to £2,940 (+194%).

Miss the best three months, and the outcome drops further to £2,498 (+150%).

There is no reliable way to predict when those best days will occur, nor to step out and back in at the right time. The only way to capture them is to remain invested.

Source: Dimensional Fund Advisors. Figures based on the MSCI World Index in GBP terms — a proxy for the global stock market.

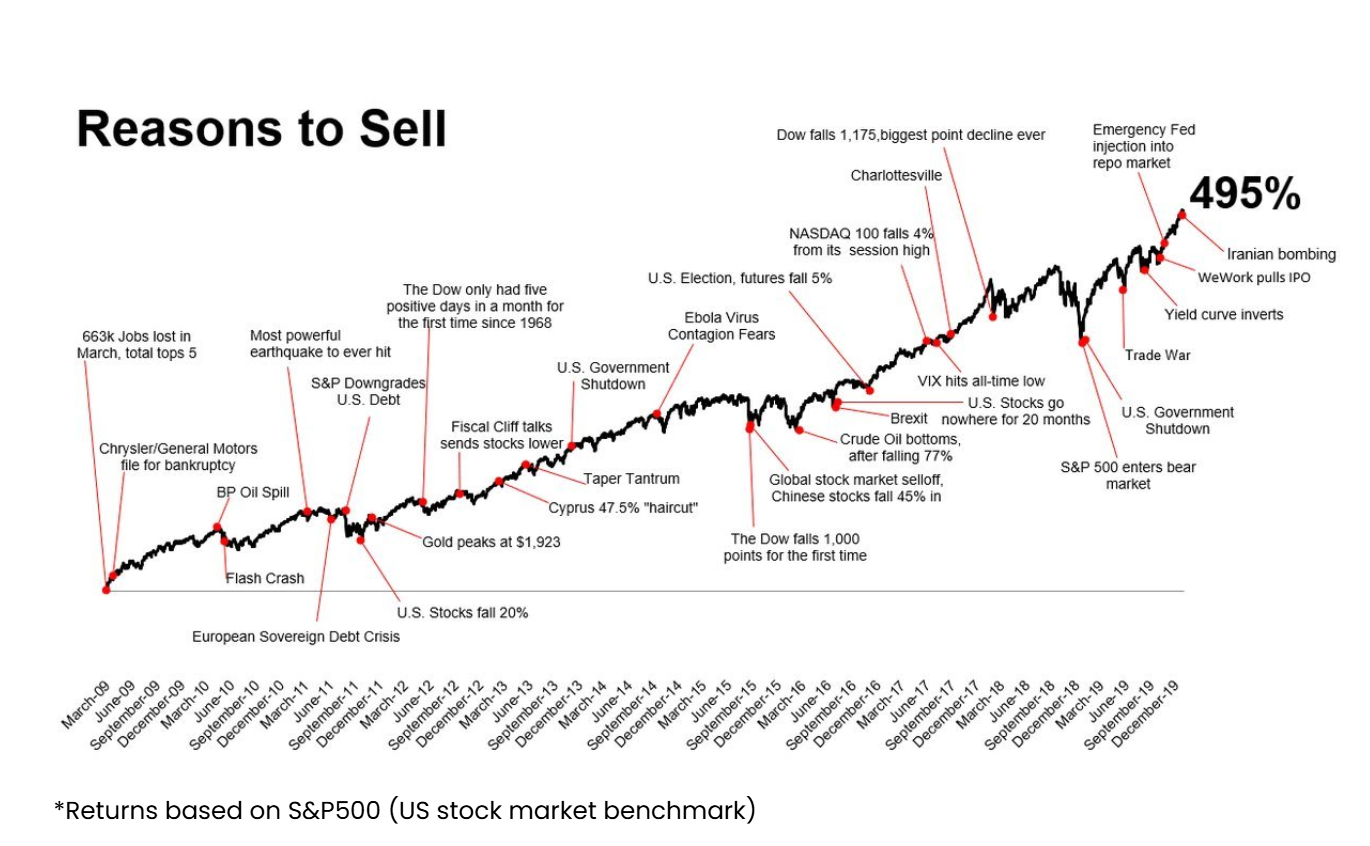

Climbing the Wall of Worry

To emphasise this point further, one of the most powerful visuals in investing is a long-term chart of the stock market overlaid with crises — wars, recessions, oil shocks and financial panics. It’s often referred to as the “wall of worry” — because markets have climbed it, time and again.

Each episode feels unique in the moment. Each comes with compelling reasons why “this time is different.” And yet, over time, the pattern is remarkably consistent: short, sharp drawdowns, followed by recovery, and ultimately, new highs.

Corrections Are Normal

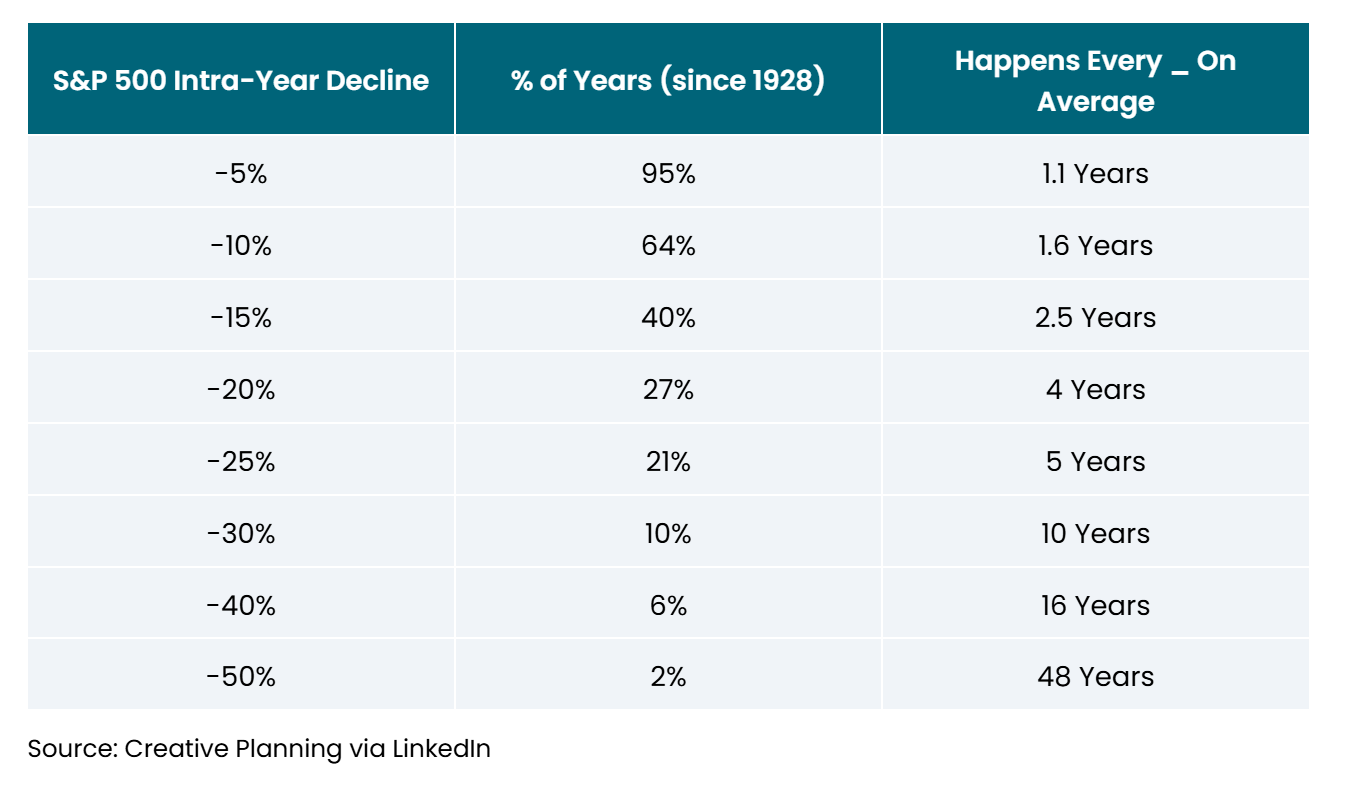

It’s also important to recognise that short-term market corrections are entirely normal.

The table below shows the frequency of intra-year declines in the S&P 500, between 1928 and end-2025:

Several things stand out:

A 5% pullback (in line with the current move) happens almost every year

A 10% correction occurs in the majority of years

Roughly one in four years sees a 20% decline — a bear market

More severe drawdowns, while less frequent, are a normal part of long-term investing. Most long-term investors, particularly those with a 20–30 year time horizon, should expect to experience multiple corrections of this nature — and likely at least one significant drawdown in the region of 30–40% or more.

However, it’s equally important to ‘zoom out’.

Despite wars, recessions, oil shocks and financial crises, markets have consistently recovered and gone on to reach new highs — driven by innovation, productivity, and the fundamental incentive of capitalism: the pursuit of profit.

Over the same period as the drawdowns outlined above, the US stock market has delivered an average annual return of circa 10%.

Stick to Core Investment Principles

Our advice hasn’t changed — and regular readers will recognise these themes from previous blogs. The principles that work in euphoric markets are the same ones that carry you through turbulent periods like this:

1. Diversify.

Don’t put all your eggs in one basket. A well-diversified portfolio — spread across regions, sectors, and asset classes, including bonds and cash — is your best defence against any single event, including an oil shock in the Middle East.

2. Focus on the long term.

It’s time in the market, not timing the market. Missing even a handful of the best recovery days can have a devastating impact on long-term returns. Crucially, those best days tend to occur during periods of peak fear and volatility — exactly when the temptation to sell is strongest.

3. Let rebalancing do the work.

Rebalancing is the unsung hero. As markets move, your portfolio naturally drifts away from its target allocation. Rebalancing restores that balance by trimming assets that have held up well and adding to those that have fallen. In effect, it enforces a disciplined “buy low, sell high” approach — quietly and systematically, without the need for emotional decision-making.

Final Thoughts

The situation in the Middle East is clearly extremely worrying. The humanitarian cost is significant. And the economic consequences — particularly around oil prices, inflation, and global trade — are real and shouldn’t be dismissed.

But from an investment perspective, this is not new territory. Markets have navigated oil shocks, wars, and geopolitical crises many times before. The pattern is remarkably consistent: sharp sell-offs followed by recovery, often faster than anyone expects.

The situation may well get worse before it gets better. But for long-term investors with a diversified portfolio and a sound financial plan, the best course of action remains the same: stay the course.

As Warren Buffett once put it: “The stock market is a device for transferring money from the impatient to the patient.”

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.