What Is Coast FIRE? How to Reach Financial Independence Without Retiring Early

A more realistic (and increasingly popular) route to financial freedom

In a previous blog we explored the FIRE movement – Financial Independence, Retire Early. Popularised by the 1992 book Your Money or Your Life, the premise is simple: live frugally, save aggressively in your twenties and thirties, and retire altogether by your early forties.

It’s an appealing idea on paper, but in reality, it’s a tough sell. Few people want to live on such a tight budget during arguably their best years. It also frames retirement as something to escape from, which isn’t always the case. For many, work provides a sense of purpose, structure and fulfilment.

That’s where a more balanced approach comes in. Increasingly, we’re seeing interest shift towards a variation of the concept: Coast FIRE.

What is Coast FIRE?

Coast FIRE is a softer, more practical version of the original FIRE concept.

It’s about reaching the point where your investments and pensions are sufficient to fund your retirement, even if you stop contributing — in other words, you’ve hit your ‘magic number’. From there, you only need to earn enough to cover your day-to-day spending, giving you the option to step back into a lower-pressure role and effectively ‘coast’.

It therefore typically plays out in two phases:

Career 1 — You work hard, earn well, and save consistently across pensions, ISAs and other investments. These are your peak earning years, where you focus on building a solid financial base.

Career 2 — Once that base is large enough to grow on its own, the pressure to save falls away. You simply need to earn enough to cover your day-to-day spending. In other words, you can afford to take a step back and ‘coast’.

It’s about having the freedom to move into work that’s potentially more enjoyable, more flexible, or less stressful — even if it comes with a lower salary.

Why this resonates

This might sound theoretical, but it’s something we’re seeing more and more in practice.

We regularly speak to clients who feel caught between two worlds. They’ve built successful careers, earned well and saved diligently — but they’re tired. The job has taken its toll. Many feel they’ve outgrown the office politics, are frustrated by increasing layers of red tape, or simply find the work less engaging than it once was.

In some cases, it’s a change in environment — a new boss, a recent takeover, or the constant pressure to hit increasingly unrealistic targets. That may have been motivating earlier in their careers, but for many, it has a natural shelf life.

At the same time, they’re not ready to stop working altogether. As we often hear: “I don’t want to stop working — I wouldn’t know what to do with myself.” They still value the routine, structure and sense of purpose that work provides — they just want it on different terms.

The traditional model of “work flat out, then stop at 65” is becoming increasingly outdated. What we’re seeing instead is a more gradual transition: work hard, step back into something more fulfilling, and then ease into full retirement over time (perhaps later than originally anticipated).

Coast FIRE simply provides a framework for that transition.

The Key Question: What’s My Number?

For anyone considering Coast FIRE, the key question is a simple one:

At what point can I stop saving, and instead move into a role that simply covers my day-to-day spending?

In other words, what’s the number you need to reach before you can afford to ‘coast’?

The answer will depend on a few key factors — how much you’ve already built up, what your current and future spending looks like, when you plan to fully retire, and the level of investment growth you can reasonably expect between now and then.

This Is Where Cashflow Modelling Comes In

Cashflow modelling is one of the most valuable tools we use in financial planning. It combines your current financial position — your assets, liabilities, income, spending, pensions and investments — with a set of assumptions around income progression, spending and investment returns, to project this forward over time.

The output is a clear, visual plan that shows whether you’re on track, and how your position might evolve under different scenarios.

In the context of Coast FIRE, it’s particularly powerful. Rather than relying on rough estimates, we can model the point at which your existing investments and pensions are sufficient to fund your retirement on their own.

Worked Example

As ever, this is best illustrated with an example.

Jack and Juliet are both 45, with a combined household income of £250,000 a year. They’ve been disciplined with their finances and have built up the following:

Pensions worth £400,000, with annual contributions of £25,000

Stocks & Shares ISAs worth £200,000, with annual contributions of £40,000

Premium Bonds of £50,000 (their emergency fund)

Cash savings of £10,000

They also own their home outright, valued at £750,000.

Their spending needs are estimated at £5,500 per month.

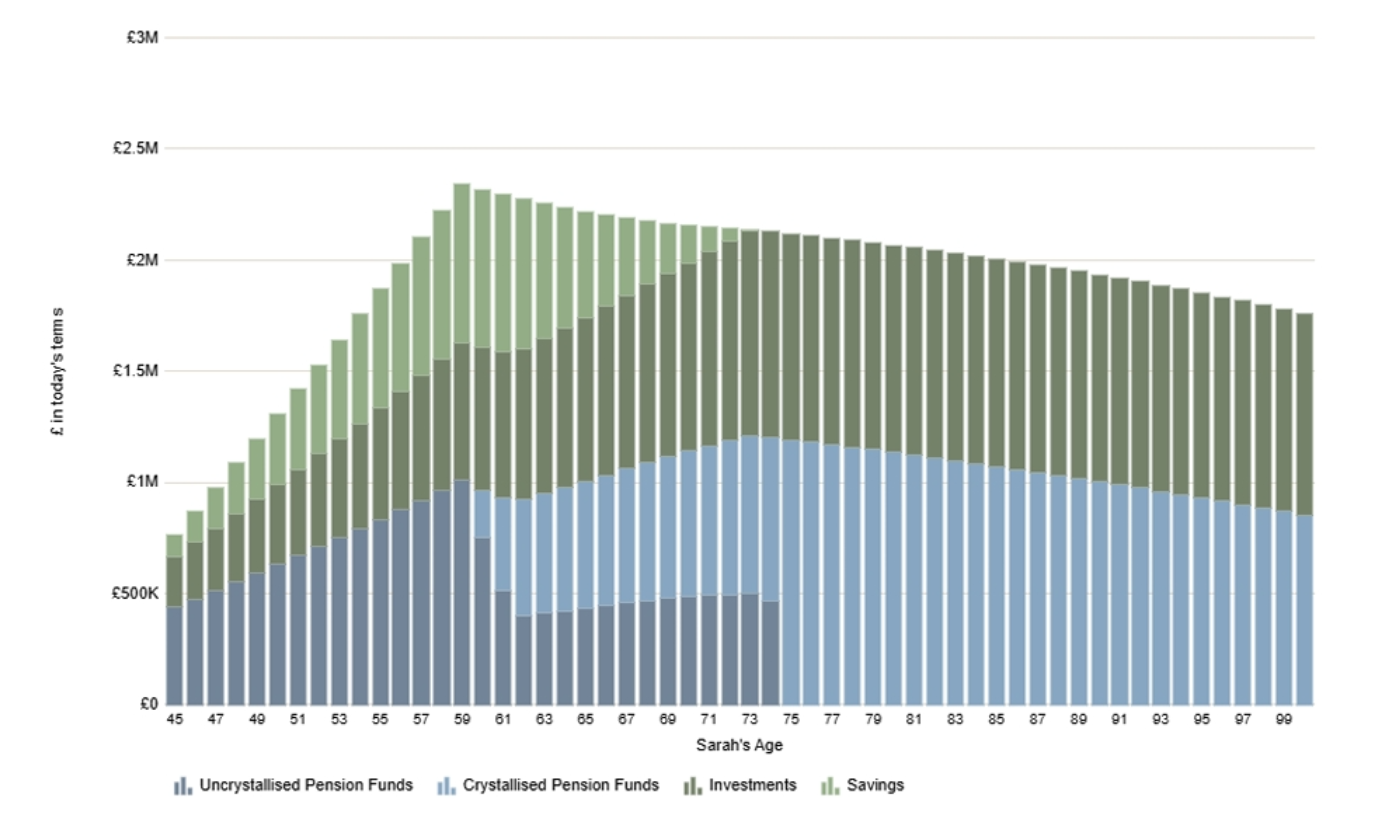

Until recently, the plan was to continue in their current roles, before retiring fully at age 60.

Under this ‘status quo’ (i.e. do nothing) scenario, the chart below shows their projected liquid capital over time. This is the key metric we focus on — it includes all accessible assets (cash, investments and pensions from minimum pension age) and provides a clear view of whether they are on track to meet their spending needs.

In their case, the answer is a clear yes. In fact, the projections suggest a significant surplus. This means they have options — including bringing forward the date of full retirement to age 56 should they wish to do so (i.e. 11 more years).

However, during our most recent meeting, Jack and Juliet noted that a range of factors had prompted a rethink. This includes a shift in culture at Jack’s firm, alongside a change in Juliet’s priorities for the future.

Neither wants to stop working entirely. In fact, they would be open to working beyond 60 — perhaps to age 68, in line with State Pension age — but only if it’s in roles that are more flexible, more enjoyable, and ultimately less demanding.

Enter Coast FIRE.

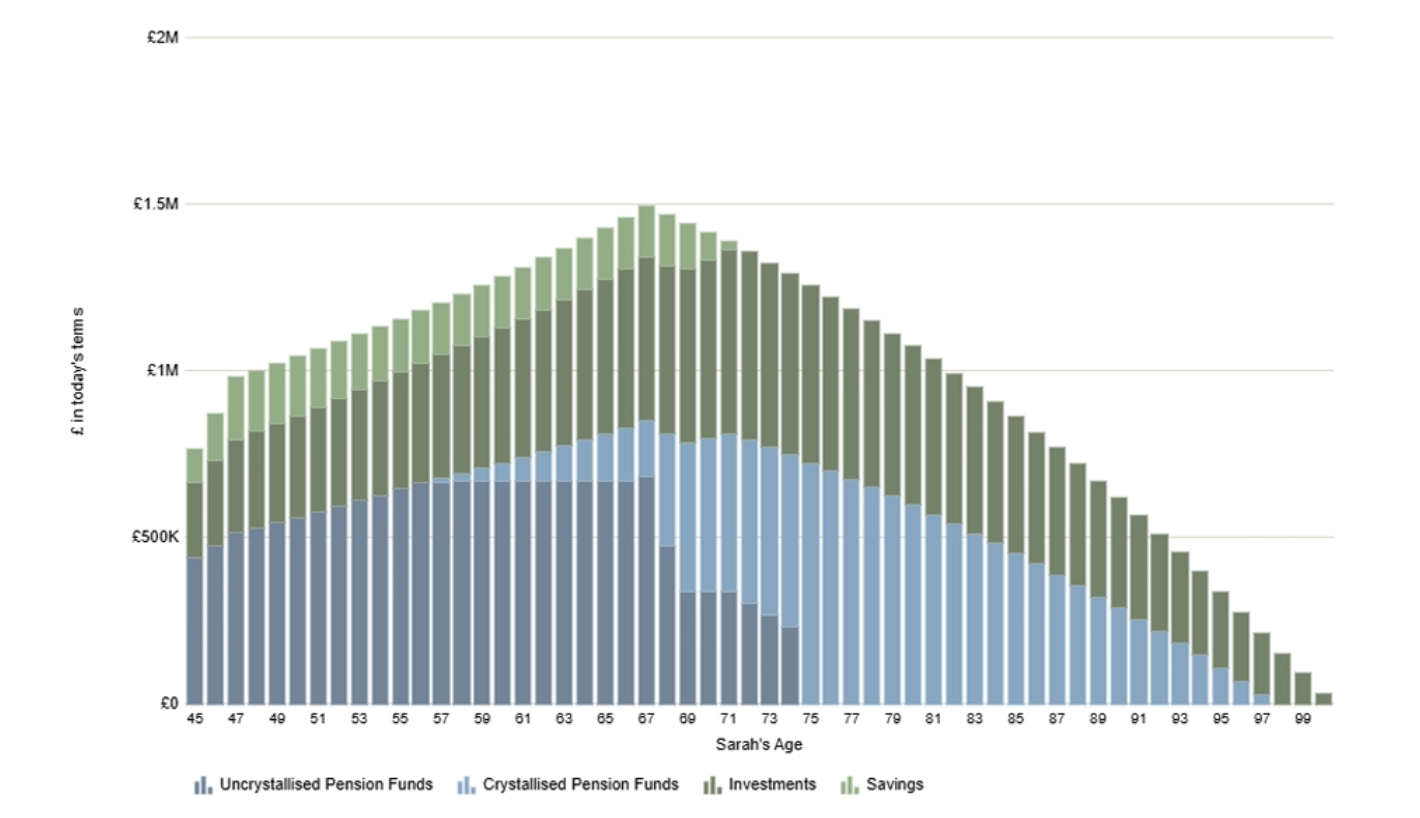

We model a scenario where they earn just enough to cover their spending needs (c. £5,500 per month). That equates to a gross income of around £40,000 each — a c. 68% reduction from their current household earnings — but crucially, with no further need to save.

The next question is: when can they afford to make this transition?

We return to the cashflow modelling and identify the point at which they can step into these second careers without depleting their liquid capital over their lifetime (we typically model to age 100 to reflect longevity risk).

In Jack and Juliet’s case, the answer is 48.

That is, just three more years in their current roles would be enough. At that point, they will have built sufficient assets in their pensions and investments to fund their retirement — with no need for further contributions. From there, they simply need to cover their day-to-day spending until retirement.

Here’s how their projected liquid capital looks under this revised scenario:

Comparing the two scenarios — ‘status quo’ vs Coast FIRE — the latter sees Jack and Juliet moving into work they genuinely enjoy, with greater flexibility and without the pressure to keep building wealth through ongoing saving. Crucially, they can make that transition in just three years’ time, rather than potentially having to remain in their current roles for another 11. Their existing investments do the heavy lifting in the background.

Summary

Coast FIRE offers a more balanced route to financial independence. Rather than stopping work altogether, it focuses on building enough wealth so your investments can fund retirement in the background — allowing you to step back from high-pressure roles sooner.

For many, this means moving into more enjoyable, flexible work without the need to keep saving aggressively. Your accumulated pensions and investments do the heavy lifting, while your income covers day-to-day spending.

The key is understanding your ‘number’ — when your assets are sufficient to support your long-term goals. Cashflow modelling helps identify this point and shows when that transition becomes viable.

Ultimately, Coast FIRE isn’t about escaping work, but gaining the flexibility to work on your own terms and transition gradually into retirement.

If this resonates, the next step is to understand your own ‘number’ — and whether you might be closer than you think.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.