Using Investment Bonds to Fund School Fees: Tax-Efficient Planning with Offshore Bonds

How to Effectively Fund Private School Fees Using Tax-Deferred Withdrawals

In Part 1 of this series, we looked at how investment bonds work, how they are taxed, and how they can be used as a retirement planning tool. If you haven’t read that yet, it’s well worth doing so before continuing, as we covered the fundamentals in some detail .

In this second instalment, we turn to what is arguably one of the most compelling use cases for investment bonds: school fee planning.

For families who have received a substantial windfall – whether from a business sale, inheritance, bonus, or another source – the question of how best to deploy those funds to cover several years of private school fees is a common one. The challenge is not simply investing the money wisely, but doing so in a way that is tax-efficient along the way.

Investment bonds, and offshore bonds in particular, offer a genuinely powerful solution here. The combination of gross roll-up (no tax drag on growth), the 5% tax-deferred withdrawal allowance (enabling you to fund fees without triggering an immediate tax charge), and the ability to assign segments to children once they reach adulthood (shifting the point of taxation to a lower or nil-rate taxpayer) makes bonds uniquely well suited to this purpose.

First, a brief recap of the key rules before working through a detailed example.

How Investment Bonds are Taxed

We covered this in detail in Part 1, but here is a summary of the key points relevant to school fee planning.

Onshore vs Offshore Bonds

Onshore bonds are issued by UK-based life insurance companies. The fund within the bond pays corporation tax on its investment returns, currently at 20%. When you later come to cash in (or ‘surrender’) the bond, any chargeable gain is treated as savings income, but you receive a non-refundable basic rate tax credit of 20%. This means that a basic rate taxpayer would have no further tax to pay, while a higher or additional rate taxpayer would pay the difference – effectively 20% or 25% on the gain.

Offshore bonds are issued by providers based in jurisdictions such as the Isle of Man or Ireland, where the fund is subject to little or no local tax. This means the bond benefits from what is known as gross roll-up – the full value of your investment returns compounds without any tax drag whatsoever. Upon surrender, the gain is still taxed as savings income in the UK, but there is no basic rate tax credit. The crucial advantage, however, is that the investment has had the benefit of growing without tax along the way.

Taxation as Savings Income

When a chargeable event arises – for example, when you partially or fully surrender the bond – the resulting gain is treated as savings income, not capital gains. This is an important distinction, because savings income benefits from a number of valuable allowances:

Personal Allowance: £12,570 of income is tax-free for most individuals.

Starting Rate Band for Savings: Up to £5,000 of savings income can be taxed at 0%, provided your non-savings income is below £17,570.

Personal Savings Allowance: £1,000 for basic rate taxpayers (£500 for higher rate).

Taken together, an individual with no other income could receive up to £18,570 of savings income completely tax-free. This becomes particularly relevant when we consider assigning bond segments to adult children, as we’ll demonstrate later.

The 5% Tax-Deferred Withdrawal Allowance

This is where investment bonds become especially attractive as a school fee planning tool.

Each year, you may withdraw up to 5% of the original amount invested without triggering an immediate income tax charge. If you do not make a withdrawal in a given year, the unused allowance carries forward to subsequent years, accumulating over the life of the bond.

A key distinction point here is that these withdrawals are not tax-free. They are tax-deferred. You are simply deferring any tax liability until a future chargeable event, such as surrender. With proper planning, however, this deferred tax charge can often be minimised considerably, or even eliminated.

After 20 years, the cumulative 5% allowances will equal 100% of the original investment, meaning you could, in theory, withdraw the entire initial premium on a tax-deferred basis over that period.

Assignment of Segments

Investment bonds are typically divided into a large number of sub-policies, known as segments – often 1,000. Individual segments can be assigned (transferred) to another person at any time, without triggering a chargeable event.

The effect of assignment is to shift the point of taxation onto the recipient. When that individual subsequently surrenders the assigned segments, the gain is assessed against their income and their tax position – not the original investor’s.

This is particularly powerful where the recipient is an adult child with little or no other income, for example whilst at university. We’ll see exactly how this works in the example below.

Worked Example: Pre-Funding School Fees

Background

Jack and Kate are both additional rate taxpayers. They have recently received a substantial lump sum as a result of a business asset sale. They have two sons, John and James, who are currently at state primary school.

John is due to start private secondary school in 4 years, and James in 6 years. The estimated cost is £25,000 per child per academic year, and both will attend from Year 7 through to the end of Sixth Form – seven years of secondary education each.

Jack and Kate intend to set aside £600,000 of their recent capital injection, to effectively pre-fund these school fees.

Setting Up the Bond

They choose to invest the £600,000 into an offshore investment bond, split into 1,000 segments for optimal future tax planning. The underlying investment is a diversified multi-asset portfolio with approximately 70% equities and 30% bonds. The precise asset allocation would, of course, depend on their individual circumstances and risk profile.

For this example, we assume the bond generates an average annual return of 5% net of charges.

Please note, when investing, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invested. Neither simulated nor actual past performance is a reliable indicator of future performance.

Years 1-3: The Accumulation Phase

During the first three years, no school fees are required. The bond is free to grow without any withdrawals.

Because this is an offshore bond, the investment rolls up on a gross basis – no income tax, no capital gains tax, no corporation tax within the fund. The full value of the returns compounds without any tax drag.

Assuming a 5% net annual return, the bond grows from £600,000 to approximately £695,000 by the end of Year 3.

Crucially, Jack and Kate have not yet used any of their 5% tax-deferred withdrawal allowance. This means the unused allowance has been rolling forward: 3 years × £30,000 = £90,000 in accumulated tax-deferred allowance, available to draw upon in future years.

Year 4: John Starts School

John now enters Year 7 at his new school. The annual fee is £25,000.

Jack and Kate’s cumulative 5% allowance at this point is £120,000 (4 years × £30,000). They have made no prior withdrawals, so they have substantial headroom.

They withdraw £25,000 from the bond to cover John’s first year of fees. There is no immediate tax charge on this withdrawal – it falls well within the cumulative allowance.

Year 5: Continued Fee Funding

Another £25,000 is withdrawn for John’s second year of fees. Cumulative withdrawals to date: £50,000, against a cumulative allowance of £150,000.

Years 6–10: Both Children at School

James now joins John at private school. The annual cost doubles to £50,000 per year.

Jack and Kate increase their withdrawals accordingly, drawing £50,000 each year from Years 6 through 10. This continues to fall within the cumulative 5% allowance, which grows by £30,000 each year.

Years 11–12: James Completes School

John finishes Sixth Form at the end of Year 10, leaving only James at school for Years 11 and 12. The withdrawals reduce back to £25,000 per year.

By the end of Year 12, both children have completed their schooling. Total withdrawals over the 12-year period: £350,000, all made within the cumulative 5% tax-deferred allowance.

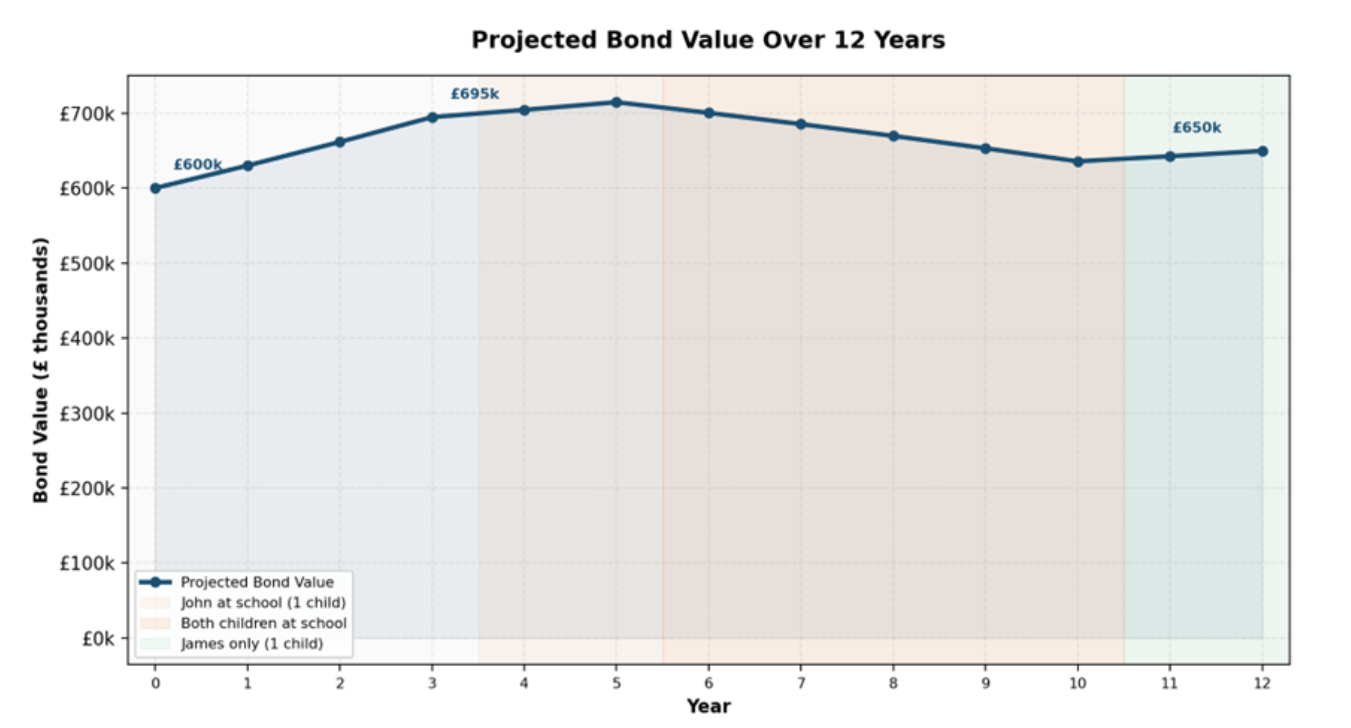

Projected Bond Value Over 12 Years

The chart below shows the projected bond value over the 12 years, based on the above strategy.

As you can see, the bond’s value remains relatively stable throughout the period despite the withdrawals, owing to ongoing investment growth. The bond peaks at around £715,000 in Year 5 before the larger withdrawals begin, and ends Year 12 at approximately £650,000 – still above the original £600,000 investment.

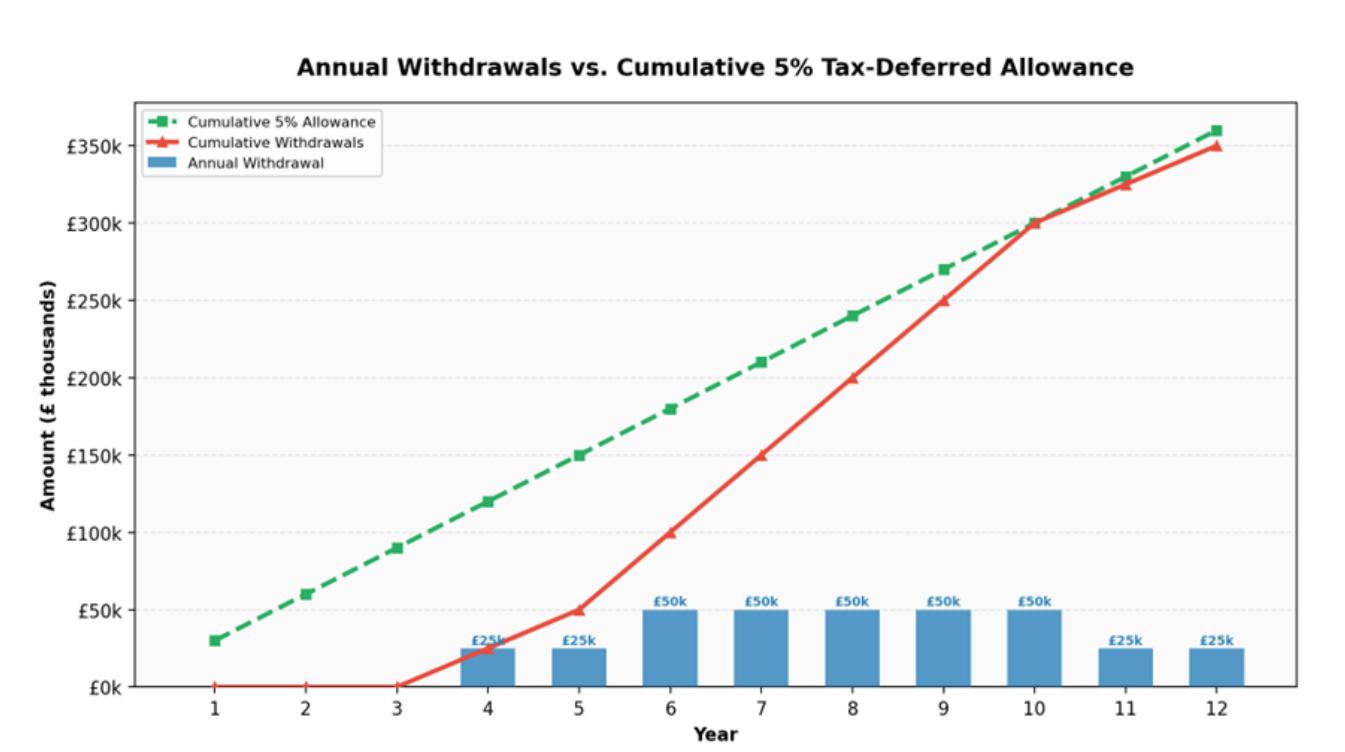

Withdrawals vs. the 5% Cumulative Allowance

This second chart compares the maximum available withdrawal allowance, Jack and Kate’s annual withdrawals to fund school fees and cumulative withdrawals.

As you can see, on the assumptions stated, they’re able to keep just within the available bond withdrawal allowance at all times. In doing so, Jack and Kate avoid triggering any immediate tax liability throughout the entire fee-paying period.

In practice of course, if fees were to rise above £25,000 per child, Jack and Kate may need to supplement the bond withdrawals from other sources. However, all else being equal, the 5% allowance covers the assumed fee schedule.

Exit Strategy: Assignment to Adult Children (or Fund Your Own Retirement)

By the end of Year 12, both John and James have finished school and are now over 18. This opens up another powerful tax planning strategy.

The Position at Year 12

On the assumptions stated:

Bond value: approximately £650,000

Initial investment: £600,000

Total withdrawals taken: £350,000

Effective chargeable gain: approximately £400,000 (bond value + total withdrawals to date – initial investment)

Assuming Jack and Kate are still additional rate taxpayers, if they were to surrender the bond themselves, the gain of circa £400,000 would be taxed at up to 45%, resulting in a very significant tax bill. To mitigate this, they might instead assign underlying segments to John and James.

How Assignment Works

Recall that the bond is split into 1,000 segments. Jack and Kate can assign any number of these segments to any individual they choose – including their adult children – without triggering a chargeable event at the point of transfer. The tax liability shifts to the recipient.

When the recipient subsequently surrenders the assigned segments, the gain is assessed against their personal income and tax position – not the original investor's.

Example: Assigning Segments to John

Let's say John is now at university, with no other earnings. Jack and Kate consider assigning sufficient segments to realise a chargeable gain of approximately £100,000.

At this point, each segment is worth approximately £650, and the gain per segment is approximately £400. To realise a £100,000 gain, they would need to assign and subsequently surrender roughly 250 segments, generating gross proceeds of approximately £162,500.

John's Tax Position

Assuming John has no other income, the £100,000 chargeable gain would be assessed as savings income.

However, John also benefits from so-called top-slicing relief. In simple terms, top-slicing works by dividing the total gain by the number of complete years the bond has been held (in this case, 12 years), producing an 'annual equivalent' of approximately £8,333.

When combined with John’s other taxable income (nil in this instance), this sits well below the higher rate income tax threshold (£50,270), which means the entire gain is effectively taxed at no more than the basic rate.

The result:

The first £18,570 of the gain is tax-free, falling within John's combined Personal Allowance (£12,570), Starting Rate Band for Savings (£5,000), and Personal Savings Allowance (£1,000).

The remaining £81,430 is taxed at 20% (basic rate), giving rise to a tax liability of approximately £16,286.

This implies an effective tax rate of around 16.3% on a £100,000 gain.

Net proceeds to John: approximately £146,000.

This process could be repeated over several years, splitting assignments between John and James, to achieve a highly tax-efficient exit from the bond. In this example, the resultant funds would be sufficient not only to cover any further education costs – such as university fees, without the need for student debt (a hot topic at present, and one we'll be revisiting soon) – but also to provide a substantial house deposit for each child.

A Note on Parental Settlements

It is worth noting that assigning bond segments to minor children (under 18) would typically fall under the parental settlement rules, meaning any resulting income or gain would be taxed on the parent. The assignment strategy described above works specifically because the children are over 18 at the point of assignment and surrender. Professional advice should always be taken in this area.

Alternatively: Retaining the Bond for Retirement

It may be that Jack and Kate prefer to retain some or all of the remaining bond themselves, rather than assigning everything to the children.

This is perfectly viable – and it brings us back to the retirement planning use case we covered in Part 1 of this series.

For example, if Jack and Kate were to retire in their late fifties or early sixties, there may be a window of several years before their State Pensions and any defined benefit pensions come into payment. During this period, their taxable income could be significantly lower – potentially placing them in the basic rate band, or even below the Personal Allowance.

At that point, they could begin surrendering bond segments in their own names, taking advantage of the same savings income allowances and lower tax rates that we described for John above. With careful planning, they could extract the remaining bond profits at a fraction of the tax cost that would apply during their working years.

In short, whether the exit route is via assignment to children, personal surrender in retirement, or a combination of both, the flexibility of the bond structure allows the family to choose the most tax-efficient path depending on their circumstances at the time.

The Big Picture

Let's consider what Jack and Kate have achieved in aggregate.

They received a substantial windfall and invested £600,000 in an offshore investment bond. Over 12 years, they:

Funded the full cost of private secondary education for two children – £350,000 in total – using tax-deferred withdrawals with no immediate tax liability along the way.

Preserved and grew the underlying capital, ending the fee-paying period with approximately £650,000 remaining in the bond – more than the original investment.

Planned a tax-efficient exit, whether by assigning segments to their adult children (effective tax rate of approximately 16%) or by surrendering segments themselves post-retirement when their income – and therefore their tax rate – is likely to be significantly lower.

Provided substantial additional funds – potentially in the region of £300,000 or more – for each child to put towards further education costs, without needing student loans, and towards house deposits.

I appreciate that the above figures are substantial, but the underlying principle is the same regardless of scale: investment bonds offer a structured, tax-efficient way to pre-fund school fees and then manage the exit from the bond in the most favourable way possible.

Please note, tax rules are subject to change and their application depends on individual circumstances. The tax treatment described in this blog is based on current legislation and HMRC practice, which may change in the future. This blog does not constitute tax advice. You should consult a qualified tax adviser or financial planner before making any decisions based on this content.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.