VCTs in 2026: Rule Changes, Tax Relief Cuts and What the Real Performance Numbers Show

TL;DR Version: Sometimes, for some people, maybe

In this week’s blog, we revisit Venture Capital Trusts (VCTs), which are back in the headlines ahead of several rule changes due to take effect in the 2026/27 tax year. Unsurprisingly, this has prompted a noticeable increase in enquiries.

Below, we recap the key rules (including the forthcoming changes), outline the main advantages and disadvantages of VCTs, and take a deeper dive into recent performance - an area that is often misunderstood or misreported.

However, before we go any further, it’s important to stress that:

VCTs are specialist investment vehicles.

They are typically only suitable for high-net-worth and experienced investors who understand the risks involved.

VCTs invest in smaller, early-stage companies, which tend to have higher failure rates and more volatile valuations than mainstream investments.

In addition, VCT shares can be relatively illiquid. While they are listed on the London Stock Exchange, secondary market demand is often limited, meaning it can be difficult (or costly) to sell your holding quickly.

To retain the upfront income tax relief, VCTs must also be held for a minimum of five years.

Finally, tax rules can change, and VCTs must continue to meet qualifying status requirements in order for investors to retain the associated tax benefits.

What Are VCTs?

Venture Capital Trusts (VCTs) are listed investment companies that operate in a similar way to traditional investment trusts. Investors buy shares in the trust itself, and the VCT then pools that capital to invest in a portfolio of underlying companies.

However, the key distinguishing feature is that VCTs are subject to strict investment criteria set by HMRC. These rules determine the type of companies a VCT can back and are designed to channel capital towards smaller, higher-risk UK businesses.

Qualifying Criteria

To qualify, companies must generally:

Be less than seven years old from their first commercial sale (extended to ten years for ‘knowledge-intensive’ companies - those operating in Research and Development)

Have fewer than 250 employees (or up to 500 for knowledge-intensive businesses)

Have gross assets of no more than £15 million before the VCT investment (and no more than £16 million immediately after)

Carry out a “qualifying trade” – which excludes certain sectors such as banking, insurance, farming, property development and energy generation

Be unquoted or listed on AIM (the Alternative Investment Market)

There are also limits on how much capital a VCT can invest. Currently, a company can receive up to £5 million per year from VCTs (and other state-backed schemes), subject to a lifetime limit of £12 million – or £20 million for knowledge-intensive businesses, which are typically research and development-led companies.

In simple terms, VCTs provide growth capital to small, early-stage, predominantly privately-owned UK companies.

Most VCTs typically invest in around 40-50 underlying companies, though this varies by manager.

Tax Benefits

In return for taking on the higher level of risk associated with smaller, early-stage companies, VCT investors benefit from a number of generous tax incentives:

Upfront income tax relief: Investors currently receive 30% income tax relief on investments of up to £200,000 per tax year (assuming you have sufficient tax liability to offset). However, this is due to reduce to 20% for investments made from the next tax year onwards - more on this shortly. To retain this relief, the shares must be held for at least five years. If they are sold earlier, the income tax relief will be clawed back.

Tax-free dividends: Somewhat counterintuitively, dividends are often the main source of return for VCT investors. As VCT managers exit underlying investments - typically via trade sales or public listings - cash is realised and distributed to shareholders. These dividends are paid entirely free of income tax. Many established VCTs target dividend yields in the region of 4–6% per annum. While not guaranteed, this income stream has historically proven more consistent than capital growth.

No capital gains tax (CGT): Any gain on the sale of VCT shares is free from capital gains tax.

Upcoming Rule Changes

In her recent Autumn Statement, Chancellor Rachel Reeves announced several important changes to the VCT regime.

The ‘Bad’:

The rate of upfront income tax relief is due to fall from 30% to 20% for investments made from the 2026/27 tax year onwards.

For investors considering a VCT allocation, this may create an incentive to act before the end of the current tax year in order to secure relief at the higher rate.

The ‘Good’:

Two less-publicised changes may prove equally, if not more, significant:

The lifetime funding limit per company will double from £12 million to £24 million (and from £20 million to £40 million for knowledge-intensive businesses).

VCTs will be permitted to invest in companies with up to £30 million in gross assets (pre-investment), up from the current £15 million limit.

The reduction in tax relief has been widely reported. However, these two changes have received far less attention in the mainstream press, yet we believe they could be meaningful.

Why This Matters

1. Greater ability to back the winners

VCTs rarely deploy capital into a company in a single investment. Instead, they typically invest modestly at first and then provide follow-on funding to businesses that perform well.

By doubling the lifetime investment limits, VCT managers should, in theory, be able to allocate more capital to their strongest performers. If “winners” can be identified early, this greater flexibility could enhance overall portfolio returns.

2. Access to more mature businesses

Increasing the gross asset threshold from £15 million to £30 million allows VCTs to invest in slightly more established companies. In theory, this could reduce failure rates and smooth overall returns, as slightly larger businesses may already have more robust revenues and operational infrastructure.

Of course, the ‘proof will be in the pudding’. The new rules do not take effect until next year, so we have no empirical evidence yet. While the reduction in income tax relief is clearly a negative on entry, the structural changes to investment limits may improve portfolio quality over time.

The Recycling Strategy

Another key element of VCT investing is what’s commonly referred to as the ‘recycling strategy’.

This warrants a blog in its own right, but in brief:

After five years - once you are beyond the income tax relief clawback period - you are free to sell your VCT shares. Most VCT managers operate a share buyback facility, typically purchasing shares at a 5–10% discount to the prevailing Net Asset Value (NAV).

The proceeds can then be reinvested into a new VCT issue, allowing you to claim a fresh round of income tax relief on effectively the same original capital.

Over time, this repeated cycle of reinvestment and tax relief can meaningfully enhance overall returns, particularly for higher-rate taxpayers who are able to fully utilise the relief each time.

Of course, this strategy depends on the continued availability of VCT offers, stable buyback policies, and unchanged tax rules, none of which are guaranteed. But when executed carefully, recycling can be a powerful component of long-term VCT investing.

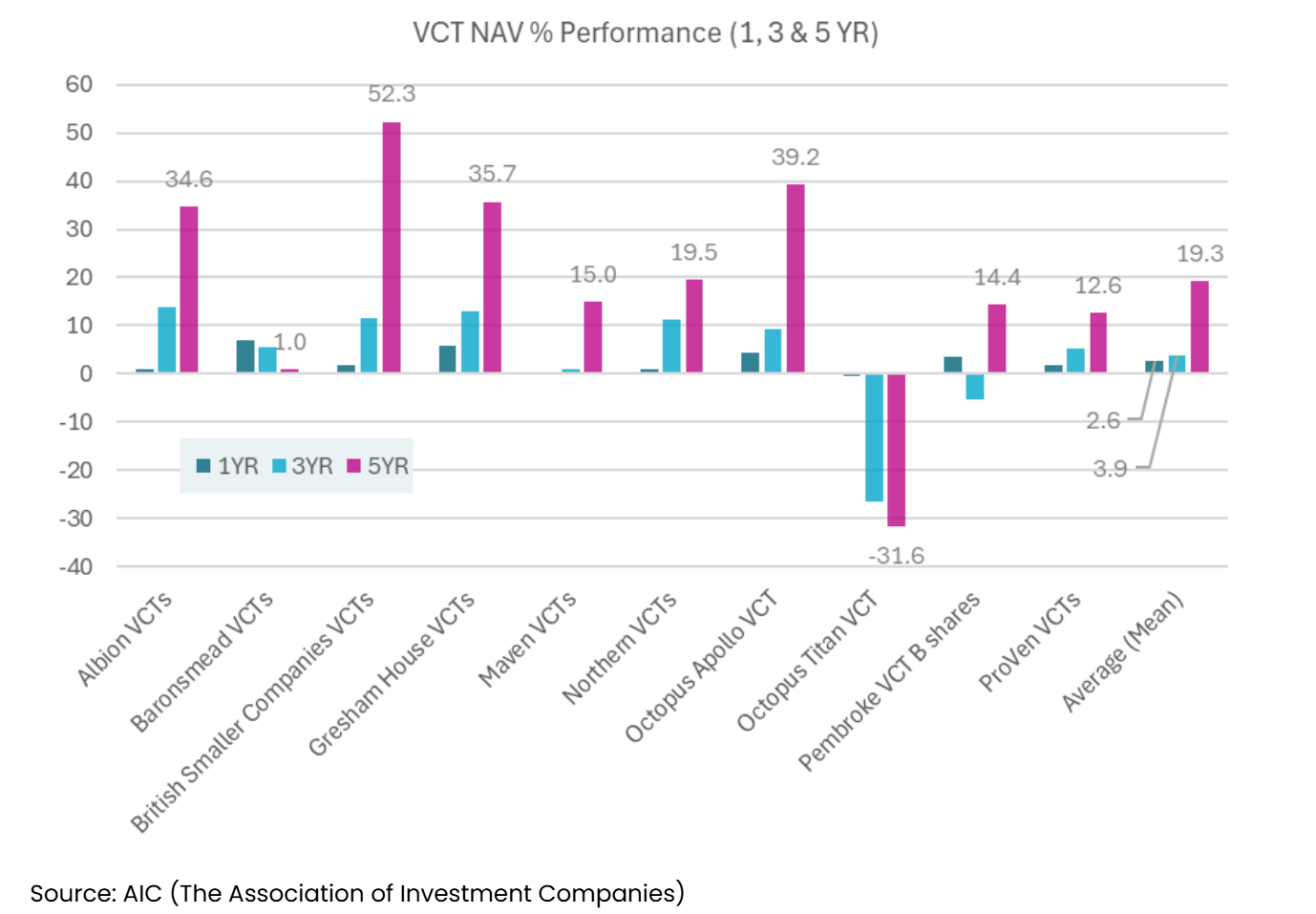

What Do the Actual Numbers Tell Us?

The chart below shows the 1, 3 and 5-year cumulative NAV returns of the ten largest VCT managers by assets under management.

Where managers operate multiple VCTs (for example, Northern, British Smaller Companies, Albion and others), we have used the average return across their underlying trusts. In practice, investors often split allocations evenly across a manager’s range, so this provides a fair reflection of typical exposure.

The final column shows the average return across the wider VCT universe.

Importantly, these figures reflect NAV returns only, in other words, how the underlying value of the VCT portfolios has evolved. They do not include upfront income tax relief, which clearly enhances overall investor returns.

Key Findings:

1. Five-year returns have been respectable, but lag public equities

Over the past five years, VCTs have delivered average cumulative NAV returns of around +19%.

That compares with roughly +70–80% from global equity index funds over the same period (for example, Vanguard FTSE Developed World or HSBC FTSE All-World - data to 11/02/2026).

On a gross, pre-tax-relief basis, VCTs have materially underperformed listed equities.

2. Tax relief changes the equation.

If we assume 30% upfront income tax relief and hold all else equal, the effective five-year return rises to around +70%.

At that point, performance appears broadly comparable to public equities, albeit with a much higher risk profile and greater dispersion of outcomes.

3. Returns vary enormously by manager.

Performance dispersion is wide.

The strongest manager in the sample (British Smaller Companies) delivered +52% gross over five years - equivalent to +117% once tax relief is factored in.

The weakest (Octopus Titan) produced -32% gross (around -3% net after relief).

Manager selection clearly matters.

4. Recent years have been difficult.

One and three-year returns have been subdued, averaging +2.6% and +3.9% respectively.

Therefore, much of the five-year return was delivered in the 2020–2022 period, when liquidity was abundant and valuations were strong. Since then, higher interest rates, tighter funding conditions and reduced exit activity have weighed on the sector.

That said, VCTs operate on long cycles. Periods of weaker performance are often followed by stronger vintages — though, as ever, past performance is no guide to future returns.

Conclusion

Five-year returns, once factoring in income tax relief, are broadly comparable to public equities.

However, those returns are skewed toward earlier years, vary significantly between managers, and come with higher volatility and illiquidity.

For that reason, we view VCTs as a satellite allocation, not a core holding. Pensions and ISAs should usually be maximised first, as they offer similar long-term return potential with far less complexity and risk.

That said, once these allowances are used, VCTs may suit experienced investors with long time horizons, particularly those able to benefit from the recycling strategy.

The upcoming rule changes may modestly improve underlying portfolio quality, potentially offsetting the lower tax relief from 2026/27.

As the TL;DR suggests: sometimes, for some people, maybe.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

George Taylor, CFA

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.