How Business Relief Schemes Work: IHT Benefits, Real Risks, and the Opportunity Cost Most Advisers Don't Mention

(image created by AI; article written by me)

How BR Schemes Work, What the Risks Are, and Our Preferred Approach

Business Relief offers a rare combination in inheritance tax planning: a two-year qualifying period, no requirement to give up access to your capital, and 100% IHT exemption up to £2.5 million. In this week’s blog we explain how it works, what's changed since April 2026, and where the risks — including opportunity cost — are most often overlooked.

Business Relief (BR) is, on paper, one of the most compelling tools available for mitigating inheritance tax (IHT). Invest in qualifying businesses, hold the shares for two years, and those shares can pass to your beneficiaries free of IHT. No seven-year wait. No need to give up access to your capital. No complex trust structures. No costly life insurance premiums.

On the face of it, that sounds almost too good to be true — and, inevitably, there are caveats. BR schemes carry real risks and are not suitable for every investor.

Important Risk Warning: Business Relief schemes are specialist investment vehicles designed for high net worth and sophisticated investors only. They carry significant risks — including illiquidity, legislative change, concentration of underlying investments, and higher costs than mainstream funds — and should only be considered as part of a personalised financial plan following professional advice. As with all investments, the value of your investment can fall as well as rise, and you may get back less than you put in.

The Mechanics

The basic principle of BR is straightforward: you invest in a qualifying business. After holding the investment for at least two years, and provided it is still held at the point of death, the value of those shares qualifies for 100% relief from IHT (up to £2.5 million per person, with 50% relief applying above that threshold). The shares pass to your beneficiaries free from inheritance tax.

Crucially, the investment remains in your name throughout and, with most schemes, can be accessed if your circumstances change.

Compare that with the main alternatives:

Gifting requires you to survive seven years and means giving up both access and control.

Trusts carry the same seven-year survival requirement and, whilst they can address the control issue, access is typically lost — except through specialist structures that bring added complexity and cost.

Whole of life insurance provides cover from day one but can be expensive, and ultimately funds the IHT bill rather than eliminating it.

So far, so good.

What’s Changed: The New Rules from April 2026

A quick note on the new BR rules, introduced at the beginning of the tax year:

AIM Shares: Effectively Redundant for IHT Planning

Until April 2026, AIM-listed shares meeting certain criteria could attract 100% Business Relief. From 6 April 2026, that relief was cut to 50% — creating an effective 20% IHT charge on death. Given the inherent volatility of AIM stocks, we think this makes AIM redundant as an IHT planning tool. The risk simply doesn't justify the residual tax exposure for most investors.

The £2.5 Million Cap

The government also introduced a cap on the amount of Business Relief (BR) and Agricultural Property Relief (APR) that can qualify for full Inheritance Tax (IHT) relief. Under the revised rules, the first £2.5 million per individual will continue to benefit from 100% relief, while qualifying assets above this threshold will receive relief at 50%, resulting in an effective IHT rate of 20% on the excess. The cap was initially proposed at £1 million but was increased to £2.5 million in December 2025 following significant opposition from business owners, farmers and industry groups.

How BR Schemes Actually Work

When recommending BR investments, we use specialist schemes run by dedicated managers — such as TIME Investments, Octopus, TriplePoint, Foresight, and Puma.

When you invest, you are buying shares in a private limited company managed by that specialist. For most people, that's the first hurdle — putting a significant sum into a company you've never heard of, structured as a Ltd rather than a PLC, feels inherently risky. But the Ltd structure is a regulatory requirement: to qualify for 100% BR, the investment must be in an unquoted trading company.

In practice, the limited company operates much like a managed fund, pooling capital across a range of BR-qualifying activities. These typically focus on two distinct areas:

Renewable energy infrastructure (wind, solar, hydro, biomass) or

Secured lending to SMEs and public-sector bodies, targeting high-quality borrowers to reduce default risk

So whilst you technically hold shares in a single company, the underlying portfolio is diversified across a wide range of real-economy activities.

Capital Preservation, Not Capital Growth

BR schemes are not designed to generate outsized returns. The target is typically capital preservation with modest net returns of 3–5% per year — roughly in line with inflation. That's intentional — the real value lies in the IHT saving.

Access and Liquidity

Unlike gifting or trusts, BR shares remain in your name and can be sold if needed — most providers commit to returning funds within two to four weeks. The expectation is that you won't need to access the capital, but the option provides a useful safety net against unforeseen costs such as care needs in later life.

The Risks

BR schemes carry certain risks that must be understood before investing.

Concentration: Despite diversification within each scheme, exposure is fundamentally limited to two sectors — secured lending and renewable energy. A systemic shock to either could have a significant impact.

Legislative risk: Last year's AIM changes demonstrated how quickly the rules can shift. There is no guarantee that BR won't be tightened further in future Budgets.

Liquidity risk: Most providers commit to meeting redemption requests within two to four weeks under normal conditions. But if a rule change triggered a sudden wave of redemptions, providers might struggle, particularly those focussing on renewable energy projects where the underlying assets are illiquid by nature.

Costs: Most schemes carry an initial set-up fee of 1–2% and a similar annual management charge. Compared with no initial charge and under 0.5% per year for a mainstream diversified public equity portfolio, that gap compounds meaningfully over time.

RNRB taper: Often overlooked, BR assets are still counted within the estate for the purposes of the £2 million Residence Nil-Rate Band taper. A large BR holding could therefore trigger the loss of the RNRB, even though the BR assets themselves attract full IHT relief.

The Biggest Risk: Opportunity Cost

However, we would argue that the biggest risk, and the one most frequently glossed over by the BR providers, is the potential opportunity cost of low returns.

As noted earlier, BR schemes typically target returns of 3–5% per year net of fees — reasonable, given the objective is capital preservation and the 40% IHT saving after two years. But if more traditional public equity and bond portfolios are delivering 6%, 8%, or even 10% per year (as they have been in recent years — though it’s important to caveat here that past performance is no guide to future returns), there is a risk that the BR portfolio could be ‘overtaken’, even after adjusting for the IHT saving.

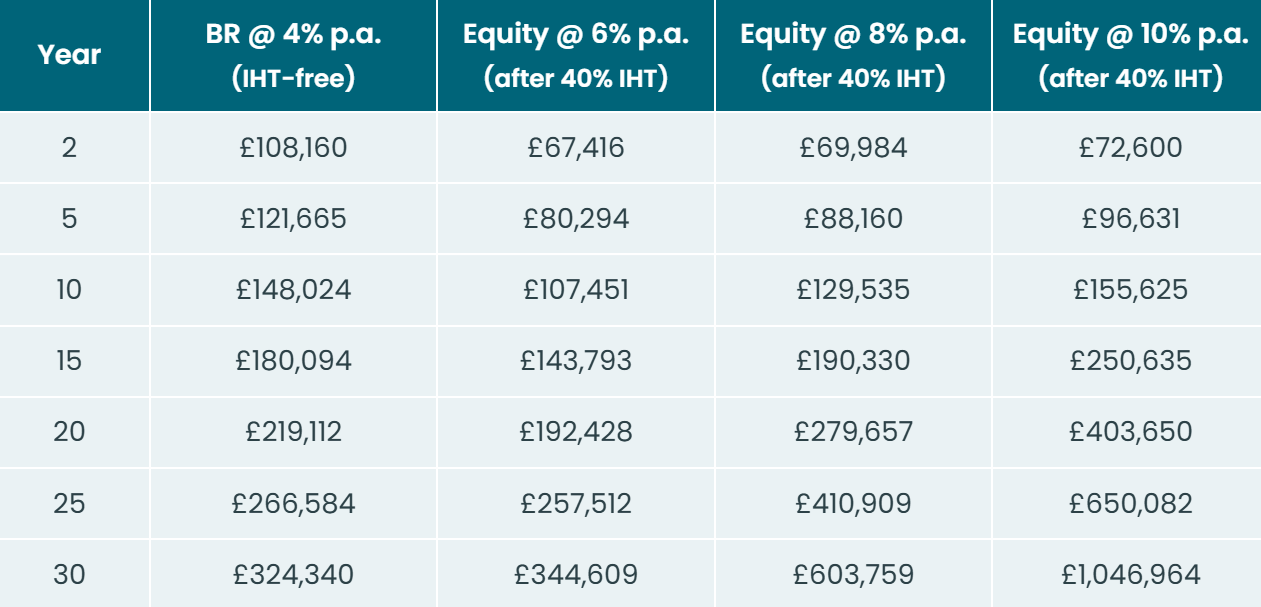

The table below illustrates the breakeven point — the year at which a more traditional equity/bond portfolio, after 40% IHT on death, overtakes a BR portfolio net of IHT — for £100,000 invested, assuming BR returns of 4% per year. We model three scenarios for portfolio returns: 6%, 8%, and 10% per year.

These figures are for illustrative purposes only and do not reflect actual investment returns, which can fluctuate and are not guaranteed.

At a 6% annual return (net of costs), the breakeven point is around 27 years. In other words, if you survive beyond that point, you would have been better off investing in a traditional portfolio and simply accepting the eventual IHT liability.

Increase the assumed return to 8% a year and the breakeven period falls to around 14 years. At 10% a year, it drops to just 10 years.

This highlights an uncomfortable reality. From a purely financial perspective, the ideal BR investment is one where you survive the two-year qualifying period, but not for so long that the lower returns ultimately outweigh the inheritance tax saving.

In other words, timing is crucial. If you begin a BR strategy in your mid-60s and have a life expectancy of 20 years or more, there is a reasonable chance that the forgone growth from a traditional equity/bond portfolio will offset much, if not all, of the eventual IHT benefit. Conversely, for someone later in life, or with a shorter life expectancy, the inheritance tax saving becomes more compelling relative to the opportunity cost.

This doesn't mean BR is a bad idea. Rather, it highlights the importance of sizing and timing the allocation appropriately.

Our Approach: Gradual Allocation

Given the risks outlined above, we don't tend to recommend large, single-tranche BR investments. Instead, our preferred approach is what we'd describe as toe-dipping: starting with a modest allocation and building it up gradually over time.

There are several reasons for this.

Familiarity: BR schemes work differently from a mainstream investment portfolio. Building up gradually gives investors time to understand how the structure operates, how reporting works, and how valuations behave in practice, without committing a substantial proportion of their wealth from day one.

Risk management: By investing in stages, you reduce the risk of allocating a large sum immediately before an adverse change in market conditions, legislation or provider circumstances. If rules evolve or a particular scheme underperforms, the impact on the overall portfolio remains contained.

Proportionality: We generally view BR as a useful complement to a broader investment strategy rather than a replacement for it. As a rule of thumb, we rarely recommend allocating more than 10–20% of liquid assets to BR solutions.

Summary

Business Relief remains one of the most attractive inheritance tax planning tools available, given the accelerated two-year IHT exemption and ongoing access to capital.

That said, as with any IHT planning solution, BR should not be viewed as a silver bullet. These schemes are designed primarily to provide inheritance tax relief rather than maximise investment returns. The underlying assets are typically concentrated in areas such as private lending and renewable energy infrastructure, creating a different risk profile from a globally diversified equity/bond portfolio. Charges also tend to be higher, liquidity can be more limited during periods of market stress, and future governments retain the ability to amend the rules (at fairly short notice).

For these reasons, we generally see BR as one component of a wider estate planning strategy alongside gifting, trusts and, in some cases, whole-of-life insurance.

Our preference is to build exposure gradually, keep allocations proportionate, and review them regularly as part of the wider financial plan. That approach allows investors to capture the inheritance tax benefits without becoming overly reliant on a single strategy.

As ever, if you’d like to explore whether BR is a good fit for you, we’d be delighted to discuss this.

Happy Thursday.

P.S. It’s coming home.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.