How Much Is the State Pension Really Worth? (And Why It’s More Valuable Than You Think)

Your Most Valuable Pension Isn’t the One You Think

The State Pension is one of the most valuable yet frequently overlooked components of retirement planning. In effect, it represents a government-backed, inflation-linked income stream, payable for life.

To illustrate its significance, the full new State Pension has recently increased to £241.30 per week, equivalent to approximately £12,550 per year. For a couple both entitled to the full amount, this equates to a combined annual income of around £25,100, or approximately £2,090 per month. And in most cases, this is received tax-free, sitting just below the Personal Allowance.

This provides a secure, inflation-protected foundation of income in retirement, with no exposure to investment risk, no requirement for ongoing management, and no risk of depletion over time.

Do You Qualify for the Full Amount?

The amount of State Pension you receive depends on your National Insurance (NI) contribution record. Under the new State Pension system (which applies if you reached State Pension age on or after 6 April 2016), you need:

A minimum of 10 qualifying years to receive anything at all

35 qualifying years to receive the full amount

A qualifying year is one in which you either paid sufficient National Insurance contributions through employment or self-employment, or you received NI credits — for example, through claiming Child Benefit for a child under 12, receiving certain benefits, or being a registered carer.

If you have between 10 and 35 qualifying years, you'll receive a proportionally reduced amount. For example, someone with 30 qualifying years would receive 30/35ths of the full rate — approximately £207 per week, or around £10,750 per year.

Checking your entitlement is straightforward. You can view your State Pension forecast online at gov.uk/check-state-pension using your Government Gateway ID. It will tell you your estimated weekly amount, how many qualifying years you have, and any gaps in your record.

We'd strongly recommend doing this.

How the State Pension Grows: The Triple Lock

One of the most powerful features of the State Pension is the way it increases each year. Under a mechanism known as the triple lock, the State Pension rises every April by the highest of three measures:

Consumer Price Index (CPI) inflation — the September figure from the previous year

Average earnings growth — measured over May to July of the previous year

A floor of 2.5% — ensuring a meaningful increase even in benign economic times

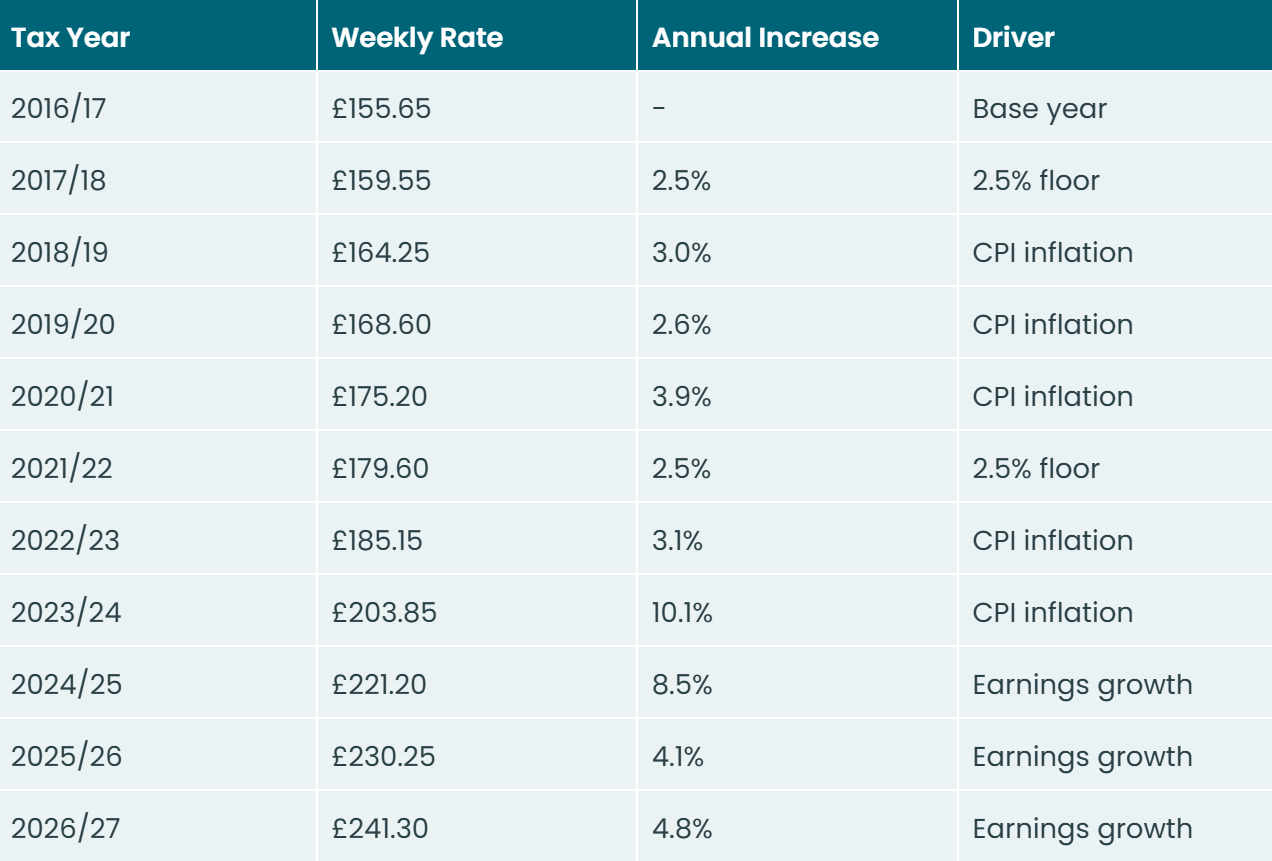

This mechanism has been in place since 2011 (with a one-year suspension in 2022/23 when the earnings element was removed due to pandemic-era distortions). The effect has been remarkable - since the new State Pension launched in April 2016 at £155.65 per week, it has risen to £241.30 — an increase of 55% in just ten years.

Over the same period, CPI inflation totalled roughly 35%. In other words, pensioners haven't just kept pace with the rising cost of living — they've meaningfully pulled ahead.

Here's how the annual increase has been determined each year since the new State Pension began:

The key feature of the triple lock is its asymmetry — it always picks the winner. In periods of low growth, you're protected by the 2.5% floor. When inflation spikes, you're protected against the cost of living. When wages are growing healthily, you share in the prosperity, a remarkably generous ratchet.

What's the State Pension Actually Worth in Cash Terms?

To truly appreciate the value of the State Pension, it helps to think about what it would cost to replicate it privately.

The State Pension provides a single-life, non-inheritable, inflation-linked income for life. The closest private market equivalent is an RPI-linked annuity with no guarantee period, purchased at State Pension age.

Based on current annuity rates (April 2026, source: AMS), an RPI-linked single-life annuity for a healthy, non-smoking 67-year-old pays approximately 5.5% of the purchase price as a starting income. We can then work backwards:

£12,550 ÷ 0.055 = approximately £228,000.

In other words, to replicate the income provided by a full new State Pension, you would need a pension pot of roughly £228,000 at today's annuity rates.

For a couple, that's a combined notional value of £456,000 (!!).

Note, we're using an RPI-linked annuity as the proxy rather than a CPI-linked one, even though the triple lock references CPI. This is deliberate - RPI has historically run higher than CPI, so it provides a reasonable proxy for the additional uplift provided by the earnings growth and 2.5% floor elements of the triple lock.

The key point is that if you had to buy this income privately, you'd need a very substantial pension pot to do so. The State Pension is, for the vast majority of retirees, their single most valuable retirement asset.

Providing an Income Floor in Retirement

Even for those with substantial pensions and investments, the State Pension provides a robust foundation for retirement income.

For a couple with full entitlement, this equates to c. £2,090 per month — effectively gross and net, as it currently falls just within the Personal Allowance (£12,570 per person per year).

This guaranteed, inflation-linked income is likely to cover most essential expenditure — groceries, utilities, council tax, insurance and transport.

This, in turn, reframes the role of other assets. ISAs, pensions and investment portfolios are no longer required to fund basic living costs, but instead support discretionary spending — holidays, leisure and lifestyle choices.

What About the Future of the State Pension?

This is where it gets politically thorny.

We've been vocal in the past about our view that the triple lock in its current form is unaffordable over the long run. The OBR estimates that pension spending could rise by around £80 billion per year in today's money by the 2070s, with more than half of that increase attributable to the triple lock mechanism. The IFS has described the policy as creating significant uncertainty for both pensioners and policymakers.

We'd advocate for a simpler approach:

A straightforward inflation (CPI) link — protecting the real value of the pension without the compounding ratchet effect

A 0% floor — so there's never a nominal reduction in income, even in the unlikely event of deflation

A gradual increase in the State Pension age towards 70 — reflecting improving health trends and encouraging more people to remain economically active for longer

This would keep the State Pension sustainable for future generations while still protecting current retirees against the erosion of purchasing power. However, such an overhaul would require long-term, cross-party thinking of the kind that is, regrettably, not synonymous with the sole political objective of winning elections every four or five years.

This is precisely why we believe pension policy — both private and state — should be removed from the hands of the major political parties and placed into an independent body, much like the Bank of England's Monetary Policy Committee. Pension decisions should be made on actuarial and economic evidence, not electoral timetables. But we accept this may be wishful thinking.

Regardless, the current regime looks set to continue for the foreseeable future.

The State Pension Age Is Changing

While the triple lock remains in place, one thing that is changing is the age at which you can claim the State Pension.

As of 6 April 2026, the State Pension age has begun its phased increase from 66 to 67. This transition, legislated under the Pensions Act 2014, will be completed by March 2028. The change is gradual — each month of birth after April 1960 adds approximately one additional month to your State Pension age, rather than a sudden jump.

In practical terms:

Born before 6 April 1960: your State Pension age is 66 (already reached)

Born between 6 April 1960 and 5 March 1961: your pension age is between 66 and 67, depending on your exact date of birth

Born on or after 6 March 1961: your State Pension age is 67

A further increase to 68 is currently legislated for between 2044 and 2046, though the Government has committed to reviewing this timetable within the next Parliament.

You can check your personal State Pension age using the calculator on gov.uk/state-pension-age.

Topping Up Your State Pension: The Best Deal in Town?

If you don't have 35 qualifying years, there may be an opportunity to buy additional years by making voluntary Class 3 National Insurance contributions. And the maths stacks up nicely here.

In terms of cost, voluntary Class 3 NI contributions for the 2026/27 tax year are £18.40 per week, or £956.80 for a full year. If you're paying for earlier gap years within the last six tax years, you may pay the rate that applied in that year (e.g., £17.75/week or £923 for 2025/26).

In terms of benefit, each additional qualifying year adds 1/35th of the full State Pension to your entitlement. At the current full rate of £241.30 per week, that's an extra £6.89 per week, or approximately £358 per year — paid every year for the rest of your life, and increasing annually under the triple lock.

You can generally fill gaps in your NI record covering the last six tax years. As of April 2026, that means you can top up gaps from 2020/21 onwards.

A worked example:

Let's say Sarah is approaching State Pension age with 30 qualifying years. She has five years she could top up:

Current entitlement: 30/35 x £241.30 = £206.83/week (£10,755/year)

Full entitlement: £241.30/week (£12,548/year)

Additional income from 5 years: £34.47/week (£1,792/year)

Cost to top-up 5 years: 5x £956.80 = £4,784

Breakeven: £4,784 cost ÷ £1,792 additional income = 2.7 years

After just two years and eight months of receiving the State Pension, Sarah will have recouped her entire outlay. Every penny after that is pure profit — and it's inflation-protected, guaranteed income for life. If Sarah lives to average life expectancy (around 87 for a woman currently aged 66), she'd receive the additional income for roughly 21 years. That's approximately £37,600 of additional income from a £4,784 investment.

Even accounting for the time value of money, this is an exceptional return.

Important: Before making any voluntary contributions, always check your State Pension forecast first to confirm that additional years will actually increase your entitlement. In some cases — particularly if you were contracted out of the additional State Pension before April 2016 — the calculation is more complex and additional years may not add as much as you expect.

Summary

The State Pension is not as glamorous as stock picking or alternative investments. But for the overwhelming majority of retirees, it is the single most important asset they have — a Government-backed, inflation-protected income for life worth the equivalent of a c. £228,000 pension pot per person.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.