Is It Better to Pay Off Debt or Invest Your Money?

When does paying down debt make more sense than investing?

It’s one of the questions we hear most often:

“I’ve got some spare cash each month - should I be throwing it at my debts, or putting it to work elsewhere?”

It’s a great question, and the honest answer is: it depends.

This week, we’re exploring the key factors that determine whether accelerating debt repayment or investing your surplus is likely to leave you better off.

The Golden Rule: Debt as a Risk-Free Return

The interest rate on your debt is effectively a guaranteed, risk-free, tax-free rate of return. Every pound you use to repay debt ‘earns’ you the interest you would otherwise have been charged. There’s no volatility, no market risk, and no tax to pay on that saving.

So the central question becomes: can you realistically earn more by investing that pound than by repaying the debt?

Comparing the Alternatives

The return you need to beat depends on where the money is invested. Because tax treatment varies by investment product or “wrapper”, the same investment return can translate into very different after-tax outcomes.

Take a debt charging 5% interest. To come out ahead financially, any investment alternative must generate more than 5% after tax. The hurdle rate therefore depends on the type of account used:

Pensions

Pension contributions benefit from upfront income tax relief. For a basic-rate taxpayer, a £100 contribution only costs £80 out of pocket - effectively a 25% uplift. For higher-rate taxpayers, the boost rises to around 66% once additional tax relief is reclaimed.

This upfront advantage dramatically reduces the gross investment return required to beat the interest on debt. For that reason, pensions often present the strongest case for investing rather than repaying borrowing.

However, pensions come with an important constraint: accessibility. Pension savings cannot normally be accessed until the Minimum Pension Age - currently 55, rising to 57 from 2028. The trade-off is therefore clear: greater tax efficiency, but less flexibility.

ISAs

ISAs are simpler. Investment growth and withdrawals are completely tax-free, making them the most direct comparison with debt interest.

If your debt costs 5%, your ISA investments simply need to earn 5% to ‘break even’.

General Investment Accounts (GIAs)

Investments held outside tax wrappers are subject to dividend tax and capital gains tax. The exact tax drag depends on your personal tax position, but as a rough rule of thumb, reducing gross returns by around 20% provides a reasonable after-tax estimate.

In practical terms, this means that to match a 5% borrowing cost, a GIA investment would need to generate roughly 6.25% before tax to make you ‘better off’.

When investing, your capital is at risk. The value of your investment (and any income from them) can go down as well as up, and you may get back less than you invested. Neither simulated nor actual past performance is a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

High-Interest Debt: The No-Brainer

Not all debt is created equal.

Credit cards typically charge 20–40% APR.

Short-term personal loans often sit in the 7–15% range.

Bridging finance and other specialist lending can cost 12–18% or more.

At these rates, it is extremely difficult for any sensible investment strategy to reliably and consistently outperform the cost of the debt without taking on excessive risk.

For that reason, the decision is usually straightforward: repaying high-interest debt should take priority over investing. The guaranteed return from clearing the debt will almost always outweigh the uncertain return from markets.

Mortgages: The Middle Ground

Mortgages currently sit in more nuanced territory. With rates on new fixed deals in the 3.5 - 4.0% range, they’re neither so high that overpayment is a no-brainer, nor so low that they can be ignored altogether.

What the Spreadsheet Says

On a purely mathematical basis, the numbers tend to favour investing.

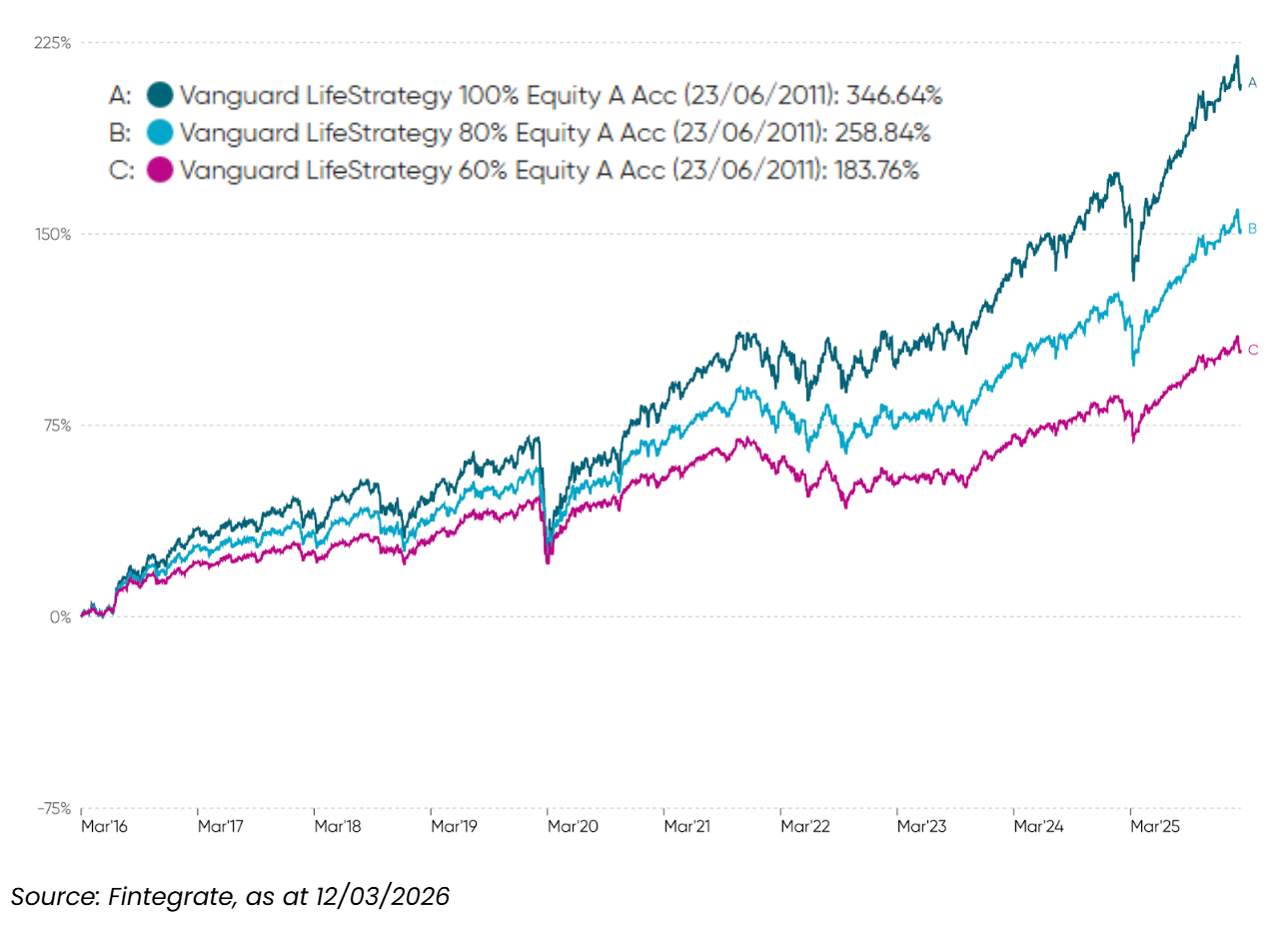

Using the Vanguard LifeStrategy funds as a reasonable proxy, long-term market returns have been compelling. Over the past 15 years:

The 100% equity version (“speculative” risk) has compounded at roughly 10% per year.

The 80/20 equity–bond portfolio (“adventurous”) has returned around 8.8% per year,

The 60/40 portfolio (“balanced”) has delivered approximately 7.2% per year.

The chart below illustrates this.

Of course, the usual caveat applies: past performance is not a guarantee of future returns. Markets can and do experience periods of volatility and underperformance.

That said, when compared with typical mortgage rates, the long-term arithmetic often favours investing - particularly when using tax-efficient wrappers such as ISAs (where returns are tax-free) and pensions, where upfront tax relief effectively boosts the return on invested capital.

What the Spreadsheet Doesn’t Tell You

But there’s more to this decision than maths. Good financial planning isn’t just about optimising post-tax returns - it’s about helping clients sleep comfortably at night.

Paying down a mortgage reduces your essential monthly outgoings. Each overpayment chips away at your committed spending and builds flexibility into your budget.

There is also a powerful psychological element. Many people have a deep-rooted desire to be debt-free, and there is genuine value in honouring that instinct. Financial decisions that feel comfortable are often easier to stick with over the long term.

Then there’s the question of whether the future will look like the past. Those long-term equity returns of 6–10% per year were achieved over decades that, broadly speaking, benefited from relatively favourable economic conditions. Looking ahead, there are credible reasons to question whether the next 10–20 years will be quite as generous: persistent geopolitical tensions, stubbornly elevated inflation, rising government debt and interest burdens, and historically high equity valuations that arguably leave less room for future gains.

Of course, the counterargument is technological progress - particularly artificial intelligence and the extraordinary productivity gains it could unlock. If AI delivers even a fraction of what is currently being promised, many of today’s economic headwinds could fade considerably.

The honest answer is that nobody knows. And that uncertainty itself is a powerful argument for avoiding extremes - rather than putting all your eggs in one basket.

A Balanced Approach

The reality is that mortgage repayment feels good. And feeling good about your financial plan matters, because a plan you stick to is worth infinitely more than a theoretically optimal one you abandon when markets wobble.

Our preferred approach, therefore, is to integrate mortgage overpayment into a broader investment strategy, rather than treating it as an either/or decision. We typically consider mortgage overpayment to be a risk-free allocation. In a traditional portfolio, bonds and other low-risk assets serve as a counterweight to equities. Mortgage overpayment can fulfil precisely that role - and at current mortgage rates, it arguably offers a more attractive risk-adjusted return than many bond funds.

By directing part of your investable surplus towards gradual mortgage overpayment, you create a reliable, guaranteed return in your overall plan – effectively replacing a bond allocation. This then frees up the remainder of your portfolio to potentially take on more risk in equity-based investments, where the potential for higher long-term returns is greater.

Student Loans: A Special Case

Student debt has become one of the most hotly debated financial issues in the UK right now. The Times has been running a high-profile campaign highlighting what it calls “crippling” graduate debt, and Martin Lewis - founder of The Money Saving Expert - has been vocal in his criticism of the government’s recent threshold freeze.

With average graduate debt now standing at roughly £53,000 and rising, it’s understandable that many feel anxious. But student loans operate very differently from conventional debt, and that distinction matters enormously when deciding whether to accelerate repayment.

How Repayment Actually Works

The crucial point with student debt is that the amount you repay each month is tied to your income, not the size of the debt.

You repay 9% of everything you earn above a threshold. If your income dips below that threshold, you pay nothing. This makes student loan repayment function more like an additional income tax than a conventional debt.

Meanwhile, interest continues to accrue on the outstanding balance.

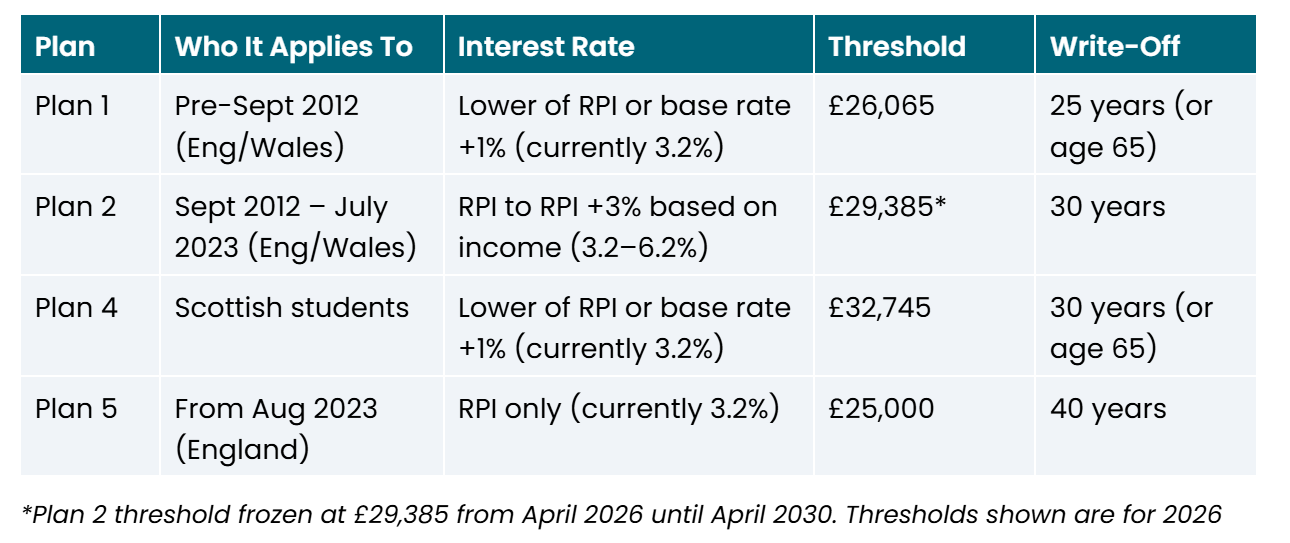

The rates and terms vary by loan type:

The ‘Middle Earner’ Trap

The particular frustration – and the one driving much of the public anger – hits graduates earning roughly £30,000 to £60,000. At these salary levels, the monthly repayment (9% above the threshold) is often less than the interest accruing on the loan.

The result is that you may be paying hundreds of pounds a month and your balance is still going up - clearly a dispiriting position to be in, particularly at a time in life when you might be trying to save for a house deposit too.

To make matters worse, this sits on top of income tax and National Insurance, creating what amounts to a very high effective marginal tax rate for graduates. A Plan 2 graduate earning £60,000 faces an effective marginal rate of 51% - 40% income tax + 2% NI + 9% student loan).

What the Numbers Show

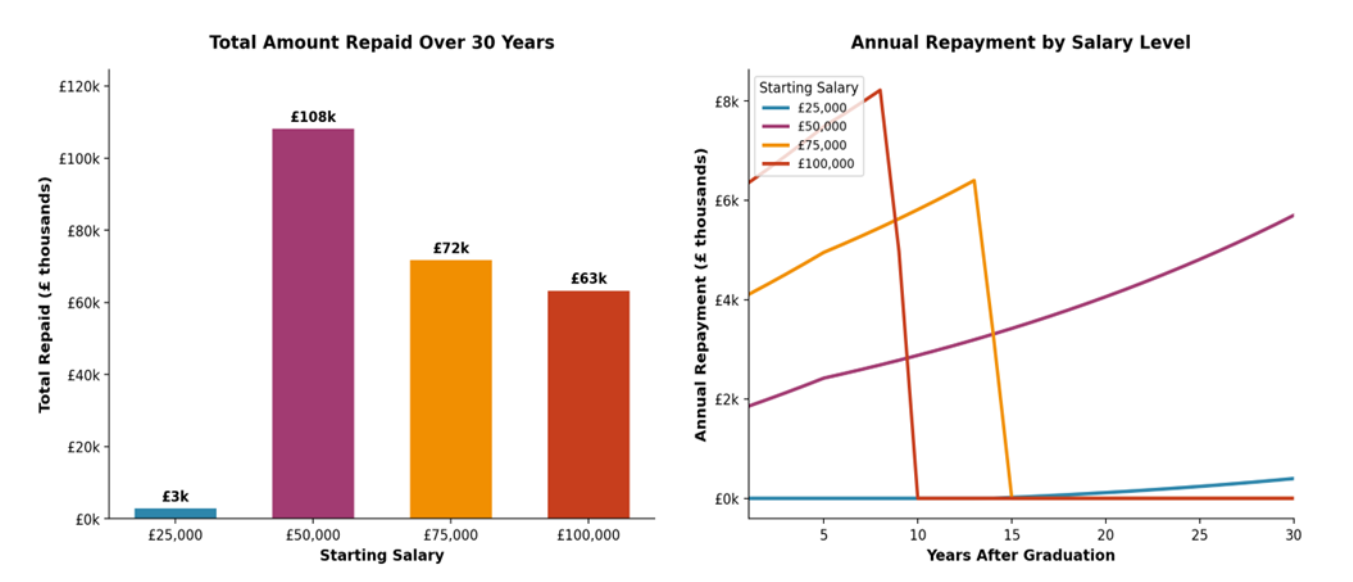

The chart below illustrates total repayments over 30 years for a typical Plan 2 graduate with £50,000 of starting debt, at four different salary levels - £25,000, £50,000, £75,000 and £100,000 a year. The results are striking:

Key takeaways from this analysis:

The £25,000 earner pays almost nothing back (roughly £3,000 over the full 30 years) before the debt is written off. For this group, early repayment makes no sense whatsoever.

The £50,000 earner pays the most in total – over £108,000 across 30 years – yet still doesn’t quite clear the balance. They’re firmly in the ‘middle trap’: earning enough to make substantial payments, but not enough to outpace the interest.

The £75,000 earner clears the debt in roughly 14 years, paying around £72,000 in total.

The £100,000 earner clears it fastest – within about 9 years – and pays significantly less overall (around £63,000) than the £50,000 and £75,000 a year earners.

The counter-intuitive result is clear: the £50,000 earner pays more in total than both the £75,000 and the £100,000 earners. This is the fundamental oddity of the system.

If you’d like to explore this for your own situation, we’ve built a student loan calculator, available via our website. By entering your loan type, current earnings and outstanding balance, the tool provides an estimate of your total repayments over the lifetime of the loan.

You can try it here: https://blincoe.uk/student-loan-calculator

Should You Repay Early? The Three Categories

Whether accelerated repayment makes sense depends not just on what you earn now, but on your projected lifetime earnings.

We think the decision broadly falls into three camps:

Lower earners (£25,000–£35,000 and likely to stay in that range): Leave the debt alone. Your repayments will be modest, and there’s a strong chance the balance will be written off before it’s cleared. Early repayment would simply be money you didn’t need to spend.

Higher earners (£70,000+ and rising): Your mandatory repayments will comfortably exceed the interest, and the debt will come down relatively quickly on its own. There’s less urgency to overpay.

Middle earners (£35,000–£65,000): This is the difficult zone. You’re making meaningful repayments, but they may not be outpacing the interest. For this group, accelerating repayment can make sense, but it must be weighed against other priorities – particularly if you’re saving for a home.

The Case for ‘Wait and See’

For recent graduates especially, our general advice is to not rush the decision. In the first few years after university, your career trajectory is still taking shape. The difference between settling into a £30,000 role and climbing quickly to £60,000+ changes the calculus entirely.

Give it time. Let your earnings trajectory become clearer, and then make a considered decision about whether voluntary repayment is genuinely worthwhile for your circumstances.

Student Debt and Getting on the Property Ladder

There’s a common misconception that student debt damages your ability to get a mortgage. This is not the case - student loans do not appear on your credit file, and lenders do not treat them as conventional debt for the purposes of creditworthiness.

That said, the monthly repayment does reduce your net income, which can affect affordability assessments. But the debt itself won’t prevent you from being approved.

For many young people, buying a home is the top financial priority. If that’s you, directing surplus cash towards building a deposit almost certainly makes more sense than accelerating student loan repayment. The deposit gets you on the ladder; the student loan will take care of itself one way or another.

Conclusion

If there’s one takeaway from all of this, it’s that not all debt should be treated the same.

High-interest borrowing - such as credit cards or expensive personal loans - is usually the clearest case for repayment first. The interest rates are simply too high for most investment strategies to compete with on a consistent, risk-adjusted basis.

Mortgages, by contrast, tend to sit in a more balanced middle ground. The mathematics often favour investing over the long term, particularly when using tax-efficient wrappers like ISAs and pensions. But the numbers alone don’t capture the full picture. Reducing your mortgage can improve financial resilience, lower your essential spending and provide peace of mind - benefits that are difficult to quantify in a spreadsheet.

Student loans are different again. Because repayments are income-linked and balances are eventually written off, they behave less like traditional debt and more like a graduate tax. For many borrowers, especially those early in their careers, accelerating repayment may not be the most effective use of surplus cash.

In practice, the right approach will depend on a range of factors: the interest rate on the debt, your tax position, your investment timeframe, your attitude to risk and your broader financial goals. For many households, a blended approach - gradually reducing debt while continuing to invest - can strike a sensible balance between mathematical optimisation and financial peace of mind.

As always, the ideas discussed here are general guidance rather than personal advice. Your own circumstances, priorities and tolerance for risk will ultimately determine what makes the most sense for you. If you’re unsure how these principles apply to your situation, it may be worth discussing them with a financial professional who can look at the full picture.

Happy Thursday!

P.S. I’m running the London Marathon in April and raising money for Sue Ryder, a charity that provides compassionate end-of-life care and vital bereavement support for families. They help people through some of the most difficult moments in life, offering expert medical care, emotional support and practical guidance when it’s needed most. If you’d like to support this fantastic cause, I’d be hugely grateful – here’s the link to my JustGiving page: JustGiving Page.

Kind regards,

George

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.