Why Younger People Are Turning Away from Pensions - And Why the Maths Still Strongly Favour Saving Early

Younger savers are losing faith in pension saving

I’m finding it increasingly difficult to get younger clients excited about pension saving.

I see a worrying trend emerging, with an increasing number of Gen Zers and Millenials turning away from pensions, driven by a convergence of financial pressures and policy distrust.

The first and most common concern is around liquidity: “I don’t want to lock money away for so long.” This is reasonable. For a generation already financially stretched, battling high rents, student loan repayments, and a seemingly insurmountable climb onto the property ladder, the idea of locking capital away until their late 50s feels abstract and restrictive.

But more concerning is a second, fast-growing sentiment: “Why bother saving into a pension when the government will just tax it all away?”

Note, a pension is a long-term investment and funds are not normally accessible until 55 (rising to 57 from April 2028). When investing via a pension, your capital is at risk. The fund value may fluctuate and can go down.

The Erosion of Trust

This lack of trust in the long-term ‘rules of the game’ has become a significant psychological barrier. And while this scepticism can feel cynical, it’s not entirely without foundation.

The UK pension system has been in near-constant flux, reshaped by repeated policy changes and fuelled by a media cycle that thrives on worst-case scenarios. Annual allowances have been lifted and lowered. The Lifetime Allowance was first slashed, then abolished, only to be replaced with new limits that few people fully understand. From April 2027, pension pots are also set to fall within the scope of Inheritance Tax — creating the prospect of a “double death tax” for beneficiaries: IHT on the pot itself and income tax when they draw it (for deaths after age 75).

And layered on top of this is the annual ritual of doom-laden predictions that tax-free cash will be cut and tax relief harmonised across income bands - headlines that reappear each year ahead of the Autumn Statement, unsettling savers even though they never actually materialise (not yet anyway).

Understandably, this breeds confusion and distrust. Today’s pension system isn’t just complicated, it now feels politically vulnerable too.

The Unmatched Advantage

And yet, despite this constant policy noise, pensions remain the most tax-efficient long-term savings vehicle for the vast majority of UK taxpayers.

Even with all the complexity, they offer unmatched advantages, particularly for younger savers who have time on their side. The power of compounding over decades is still the single most potent force in wealth accumulation.

But time only helps if you put it to work. To illustrate the permanent cost of delaying or disengaging from pension saving, here are two worked examples.

Example 1: Three friends, three approaches

Consider three friends - Jack, Charlie, and Michael - all aged 40 and earning £100,000 a year. Each commits to saving £20,000 every year for 20 years.

Jack contributes to his pension.

Charlie, distrustful of future pension rules, contributes to his Stocks & Shares ISA.

Michael, ignoring advice, uses a taxable General Investment Account (GIA).

How each method works

Jack (Pension)

Contributes £20,000 net each year as a personal pension contribution.

Basic-rate relief is added automatically, grossing this up to £25,000.

As a higher-rate taxpayer, Jack receives a further £5,000 rebate via self-assessment, reducing his true out-of-pocket cost to £15,000.

Total net cost over 20 years: £300,000

Total gross contribution: £500,000

Investments grow free of income tax and capital gains tax.

In retirement, 25% can be withdrawn tax-free, with the remainder taxed at Jack’s marginal rate (assumed 20%).

Charlie (ISA)

Contributes £20,000 each year from post-tax income into a Stocks & Shares ISA.

Total cost and contribution over 20 years: £400,000

Growth is entirely tax-free, and funds can be withdrawn at any time without tax or restrictions.

Michael (GIA)

Contributes £20,000 each year to a taxable General Investment Account (GIA).

Total cost and contribution over 20 years: £400,000

Dividends, interest and realised capital gains (beyond allowances) are subject to tax.

Note: The core tax benefits of personal pension contributions remain unchanged under the new legislation (announced in the Autumn Statement 2025). Only certain salary-sacrifice contributions will lose NIC advantages from 2029.

Access note: Pension funds can normally be accessed only from the Minimum Pension Age - currently 55, rising to 57 in 2028.

Results (assuming 6% annual growth over 20 years)

Performance note: These figures are for illustrative purposes only and do not reflect actual investment returns, which can fluctuate and are not guaranteed.

Taxation note: Pension withdrawals assume 25% tax-free, with the remainder taxed at the basic rate only. For the GIA, we assume (conservatively) that all investment growth takes the form of capital gains taxed at 18%. In reality, some returns will come from dividends or interest, and some gains will be covered by allowances. As such, Michael’s actual tax liability would likely sit somewhere between the GIA and ISA outcomes.

Interpretation

Jack, the pension saver, finishes with the highest level of wealth, despite paying £100,000 less out of pocket than either of his friends (thanks to his £5,000 per-year tax rebate). His pot grows from £300,000 of net contributions to £918,266 pre-tax, delivering an effective 160% return, or +£481k in nominal terms. This return could have been higher still had he recycled his annual £5,000 rebate back into the pension (or some other investment vehicle), a common strategy among our clients.

Charlie’s ISA performs well, turning £400,000 into £734,613 — but the effective return (84%) is roughly half that of Jack’s pension.

Michael fares worst. By keeping his money in a straightforward trading account (a GIA), the drag from capital gains tax sees him end up over £200,000 worse off than Jack.

This example illustrates why pension saving continues to ‘reign supreme’ for tax efficiency and long-term wealth creation. The core drivers of this outperformance — upfront tax relief and tax-free compounding — have survived every major pension reform to date. And while withdrawals are subject to Income Tax, the combination of front-loaded relief and, in this case, 20 years of untaxed growth more than outweighs the tax paid on exit.

Example 2: The benefit of starting early

The reluctance among younger people to engage with pensions is especially damaging, because the mathematics of starting early are transformative.

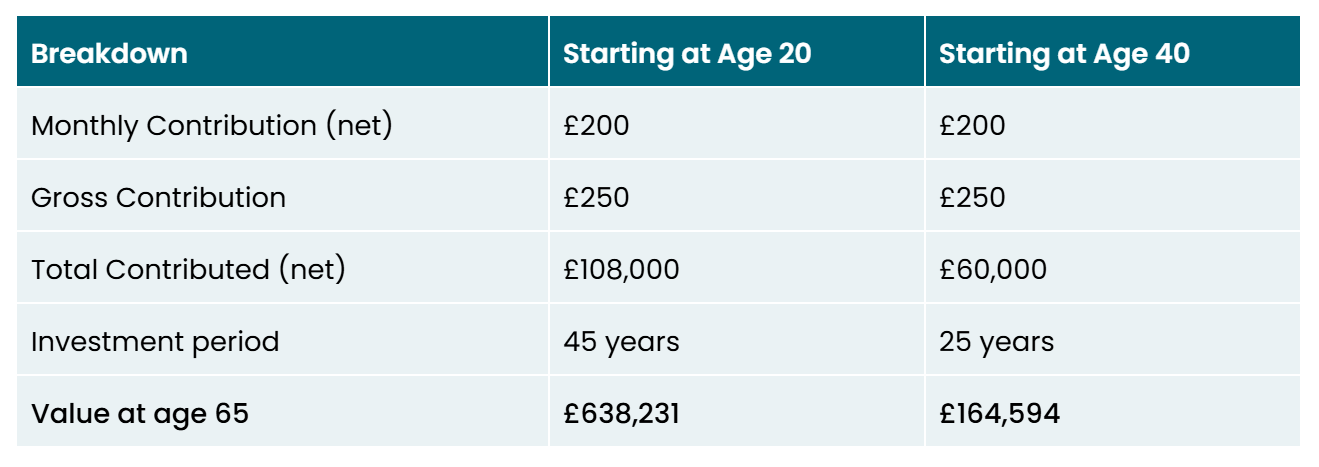

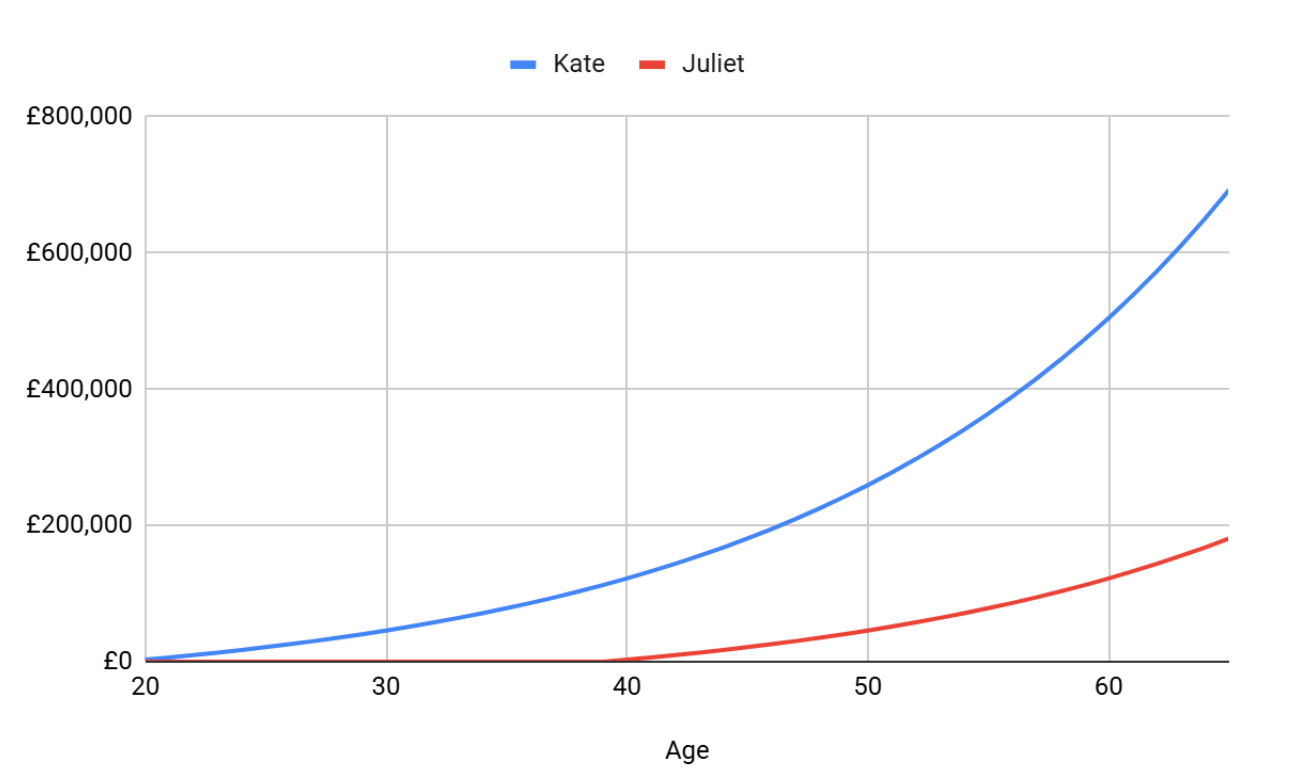

Take two colleagues, Kate and Juliet, each saving £250 a month gross (£200 net after basic-rate tax relief):

Kate starts at age 20 and saves until 65.

Juliet starts at age 40 and saves until 65.

Assuming 6% annual growth:

Kate contributes £48,000 more, yet retires with over £470,000 more than Juliet. This is also shown in the chart below.

That difference is almost entirely due to compounding:

The first £1 saved at 20 works for 45 years.

Save that same £1 at 40 and it works for just 25.

Small annual contributions, compounded over decades, become powerful. Delay compresses the investment horizon and permanently reduces the final outcome — no matter how much you contribute later.

Conclusion

Policy uncertainty is frustrating, but the mathematics of pension saving remain overwhelmingly in your favour:

Upfront tax relief

Tax-free investment growth

A 25% tax-free lump sum at retirement

Meaningful employer contributions for many

And decades of tax-free compounding

Taken together, these advantages make pensions the most tax-efficient and effective long-term wealth-building tool available.

The real danger isn’t a future policy change — it’s not saving enough for retirement. The era of guaranteed defined benefit pensions has ended. Responsibility now rests with individuals.

If you’re in your 20s or 30s and avoiding pension saving because “the rules might change”, the examples above show the cost of delay far outweighs the impact of almost any plausible future reform. Governments may tinker, but the fundamental tax advantages of pensions have survived every major overhaul to date.

Alas, don’t let hypothetical risks stop you benefiting from very real advantages today.

Happy Thursday!

Kind regards,

George

George Taylor, CFA

Referrals Welcome

Our business grows mainly through personal recommendations. If you know someone—whether a friend, family member or colleague—who might benefit from financial planning, we’d be grateful if you could share my details with them. Alternatively, you can pass their details on to me, and I’ll be happy to reach out.

Regulatory Information

Blincoe Financial Planning Limited is an appointed representative of Sense Network Ltd, which is authorised and regulated by the Financial Conduct Authority. Registered in England & Wales (No. 14569306). Registered Office: Star Lodge, Montpellier Drive, Cheltenham, GL50 1TY.

Important Disclaimer

This blog is for general information only and is intended for retail clients. It does not constitute financial or tax advice, nor is it an offer to buy or sell any specific investment. Since I don’t know your personal financial situation, you should not rely on this content as tailored advice. While we aim to provide accurate and up-to-date information, we cannot guarantee that all details remain correct over time. We are not responsible for any losses resulting from actions taken based on this blog’s content.