It’s been a volatile few weeks on the stock market, driven by concerns over a potential trade war and signs of a slowdown in the US economy. At the time of writing, US stocks, according to the benchmark S&P 500 index, have fallen approximately 9% from their all-time high, achieved just three weeks ago.

For several years, investors have questioned why they should diversify beyond US equities, given their exceptional returns. But as we move through 2025, that conversation has shifted dramatically. Now, many are wondering if they have enough exposure to European markets after almost 20% outperformance through the first ten weeks of the year.

As Stuart Kirk recently put it in his daily blog for the Financial Times: “The emails saying I’m an idiot for not owning US equities have been replaced by emails saying I’m an idiot for not owning European ones.”

It’s a perfect illustration of how quickly market sentiment can shift.

Volatility: A Normal Part of Investing

Regular readers of this blog will have heard this message before: market volatility isn’t an anomaly—it’s part of the investment journey.

Looking at US equities, which make up around 60% of the global stock market (per the MSCI All-Cap World Index), history shows that downturns are more common than many realise. Since 1980, stocks have experienced intra-year declines of more than 10% in 25 out of 44 years—i.e. 57% of the time. In other words, pullbacks like the one we’ve recently seen should be expected more often than not.

Yet, despite these temporary declines, US equities have delivered an annualised return of approximately 12% over this period.

With hindsight, a return to volatility was overdue. With foresight, it’s simply part of the journey—one that doesn’t warrant a shift in strategy and can even present opportunity.

Source: JP Morgan’s A Guide to the Markets (US edition)

Please note, when investing, your capital is at risk. The value of your investment (and any income from them) can go down as well as up, and you may get back less than you invested, particularly when investing for a short timeframe (we normally recommend a horizon of at least 5 years). Neither simulated nor actual past performance are a reliable indicator of future performance.Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

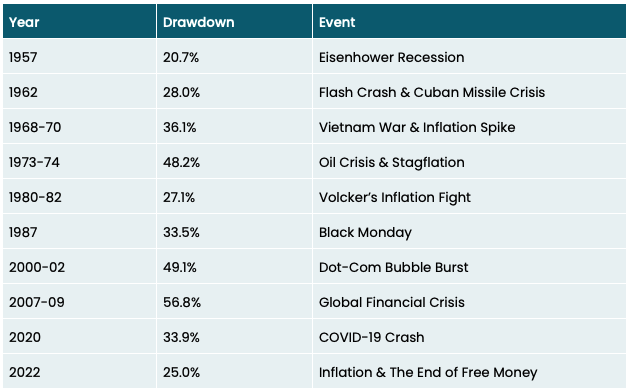

Is This the Start of a Bigger Sell Off?

The bigger question is whether this marks the beginning of a more dramatic market downturn.

While we have no way of knowing for certain, history offers some perspective. Since 1950, the S&P 500 has experienced ten major crashes—defined as declines of 20% or more from peak to trough. On average, that equates to one major sell-off roughly every five years.

Source: Visual Capitalist

This data is a powerful reminder that market downturns are not exceptions—they are part of the normal cycle. And yet, markets have always rebounded, rewarding those who stay the course.

Given the strength of the bull market in recent years, another major correction wouldn’t be surprising. But history also tells us that trying to time the market is a losing game—investors who attempt to predict downturns often miss out on the subsequent recovery.

Staying invested remains the best strategy.

Focusing on What We Can Control

The reality is that no one—not fund managers, economists, or the media—can predict with certainty when the next market downturn will come or which asset class will outperform in the short term. Instead, we focus on the things that are within our control:

- Spreading risk: A well-diversified portfolio ensures that no single asset class or region dominates your returns, providing a more stable investment journey.

- Rebalancing: This helps maintain your desired risk level while acting as a built-in "buy low, sell high" mechanism—trimming assets that have outperformed and reallocating to those that have lagged. We favour tolerance-based rebalancing, where adjustments are made only when asset weightings drift beyond a set threshold. This approach strikes the right balance between letting winners run and avoiding unnecessary trading costs.

- Keeping costs low: Investment costs compound over time just like investment returns. By using cost-efficient solutions, we ensure more of your money stays invested and working for you.

- Ensuring tax efficiency: Taxes can erode investment returns, so we structure portfolios to be as tax-efficient as possible—leveraging ISAs, pensions, and other allowances. By minimising tax drag, you get to keep more of the underlying investment returns.

- Keeping you in your seat when markets get choppy: History has shown that the biggest investment mistakes often come from emotional reactions to market volatility. By staying invested and resisting the urge to make knee-jerk decisions, patient investors have historically been rewarded with strong long-term returns. As Charlie Munger once said: “the big money is not in the buying or selling, but in the waiting."

Conclusion

Volatility is part of the journey. Market downturns often come quickly and sharply, but history has shown that investors who remain patient and stay invested through these corrections are ultimately rewarded with long-term, inflation-beating returns. The recent market fluctuations are not a reason to panic but rather a timely reminder of why we diversify, focus on what we can control, and take a disciplined approach to investing.

As always, if you’d like to discuss any of this—or the latest market volatility—in more detail, feel free to get in touch.

Kind regards,

George